by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

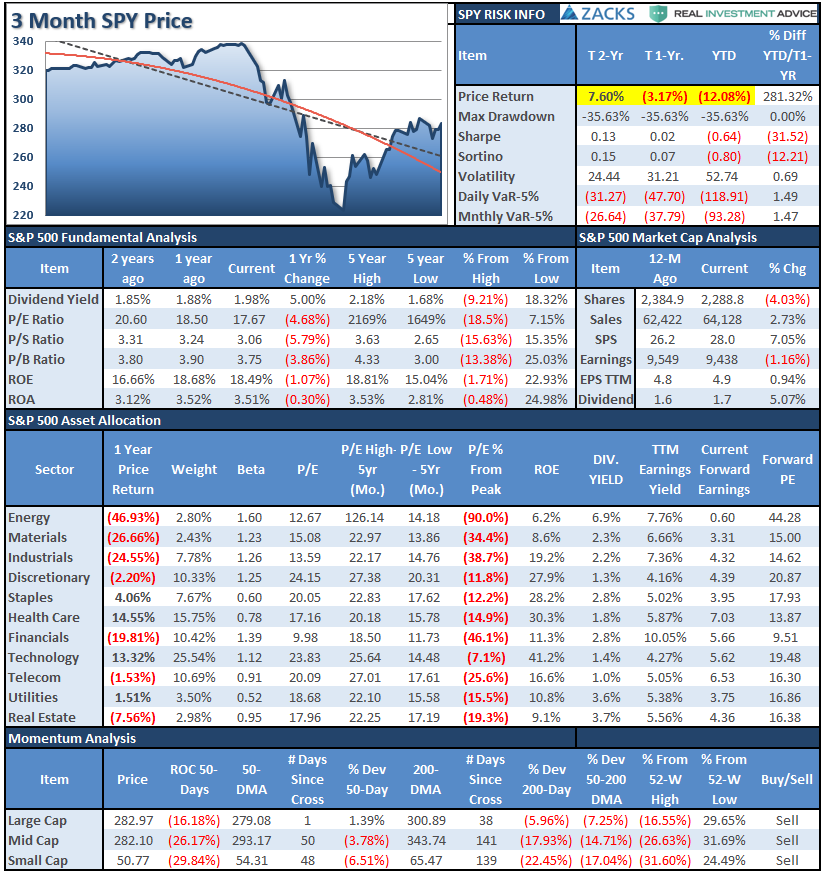

S&P 500 Tear Sheet

Performance Analysis

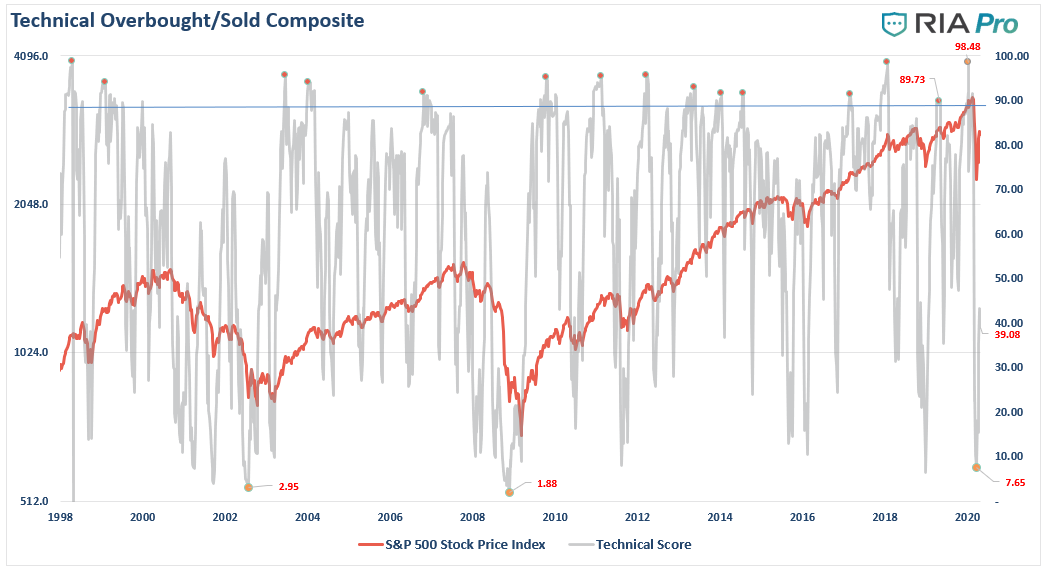

NOTE: I have rarely seen EVERY SECTOR overbought this much all at the same time. The market WILL CORRECT from these levels.

Technical Composite

Note: The technical gauge bounced from the lowest level since both the “Dot.com” and “Financial Crisis.” However, note the gauge bottoms BEFORE the market bottoms. In 2002, the market retested lows. In 2008, there was an additional 22% decline in early 2009.

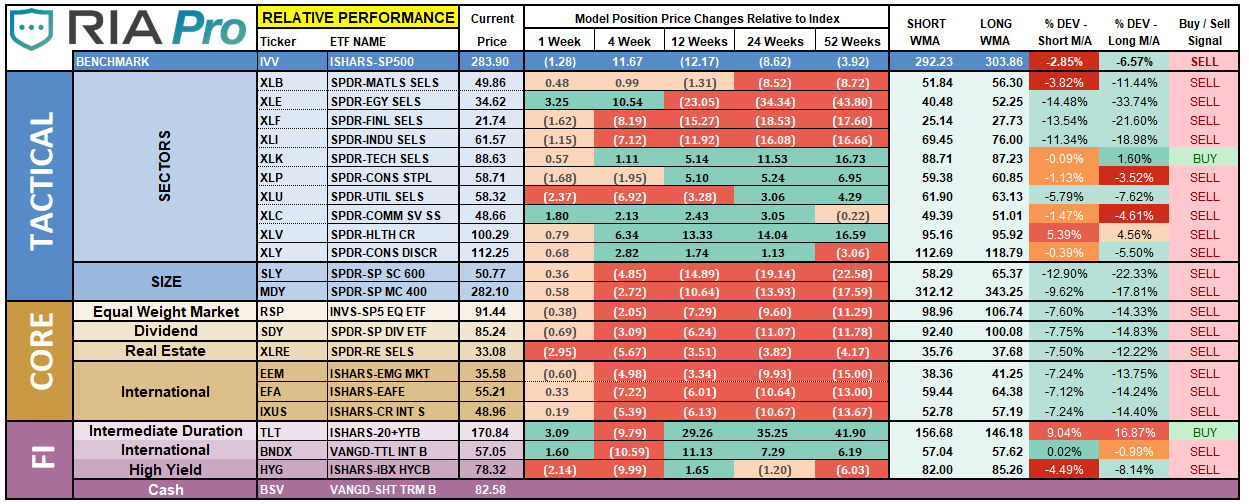

ETF Model Relative Performance Analysis

Sector & Market Analysis:

Be sure and catch our updates on Major Markets (Monday) and Major Sectors (Tuesday) with updated buy/stop/sell levels

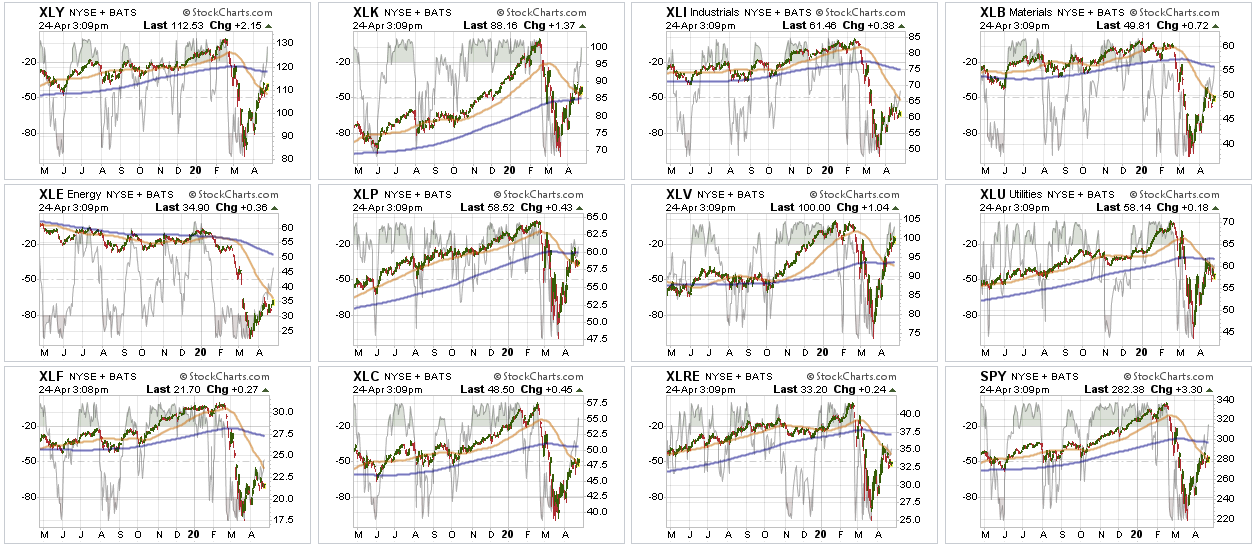

Sector-by-Sector

Improving – Discretionary (XLY), and Materials (XLB)

As noted last week, there is no rush to get into either Discretionary or Materials stocks until AFTER we get through earnings season. The economic shutdown is going to devastate the discretionary sector, focus on Staples for the time being. Early indications for earnings in the sector are terrible. These sectors are still lagging our primary holdings.

Current Positions: No Positions

Outperforming – Technology (XLK), Communications (XLC), Staples (XLP), Healthcare (XLV), Utilities (XLU), and Real Estate (XLRE)

A month ago, we shifted exposures in portfolios and added to our Technology and Communications sectors, bringing them up to weight. We remain long sectors that are currently outperforming the S&P 500 on a relative basis and have less “virus” exposure and added Utilities and Staples positions.

Everything is getting very overbought and extended in these sectors; we need a corrective pullback to add more to our holdings.

Current Positions: XLK, XLC, XLP, XLV, XLU

Weakening – None

No sectors in this quadrant.

Current Position: None

Lagging – Industrials (XLI), Financials (XLF), and Energy (XLE)

Financials continue to underperform the market. You can NOT have a lasting bull market rally without financials participating. As we have said previously, this sector, in particular, is THE most sensitive to Fed actions (XLF) and the shutdown of the economy (XLI).

We did start nibbling on exposure in the Energy sector this past week by adding some minimal positions which have been outperforming relative to the price of oil. It is WAY too early to be overly aggressive in the sector.

Current Position: 1/3rd Position XLE

Market By Market

Small-Cap (SLY) and Mid Cap (MDY) – We sold all small-cap and mid-cap exposure earlier this year over concerns of the impact of the coronavirus. We remain out of these sectors for now, and there is no rush to add them anytime soon. Be patient, small, and mid-caps are lagging badly. You can not have a “bull market” without “small and mid-cap” stocks participating. Such is currently the case and suggests the current rally remains a “bear market” rally.

Current Position: None

Emerging, International (EEM) & Total International Markets (EFA)

Same as Small-cap and Mid-cap. Given the spread of the virus and the impact on the global supply chain.

Current Position: None

S&P 500 Index (Core Holding) – Given the overall uncertainty of the broad market, we previously closed out our long-term core holdings. We will re-add a core once we see a bottom in the market has formed.

Current Position: None

Gold (GLD) – We previously added additional exposure to both our GDX and IAU positions and are comfortable with our exposure currently. With the Fed going crazy with liquidity, this will be good for gold long-term, so we continue to add to our holdings on corrections.

We also added a position in the Dollar last week (UUP) as the U.S. dollar shortage continues to rage and is larger than the Fed can offset.

Current Position: 1/2 weight GDX, 2/3rd weight IAU, 1/2 weight UUP

Bonds (TLT) –

Bonds have rallied as the Fed has become THE “buyer” of bonds on both a “first” and “last” resort. Simply, “bonds will not be allowed to default,” as the Fed will guarantee payments to creditors. As we have been increasing our “equity” exposure in portfolios over the last few weeks, we added a position in TLT on Friday to increase our “risk” hedge in portfolios currently.

Current Positions: SHY, IEF, BIL, TLT

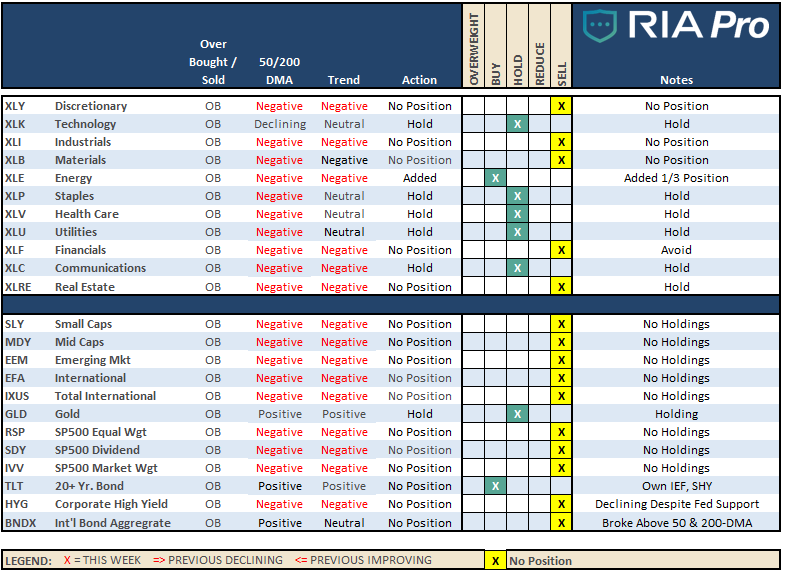

Sector / Market Recommendations

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. Such is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio / Client Update

We continue to look for opportunities where we can add exposure while still controlling overall risk. I encourage you to read last week’s missive in full if you are “getting all bullish” on the market, and think you want more exposure to equity risk.

This past week, the market struggled at the 50% retracement level but is holding the 50-dma (which is bullish short-term.) As discussed last week, there is indeed some short-term upside, but as we head into the summer months, the relative risk/reward ratio is not in our favor.

Furthermore, earnings and economic data have been horrific. While the markets do not seem to care at the moment, in hopes that there will be a rapid “V-shaped” recovery in the market, this data will eventually matter. It is not a question of “if” just a matter of “when.”

While investors are scrambling to chase markets currently, they are buying stocks with absolutely no visibility into earnings or outlooks. This type of investing tends to turn out badly. It is also important to note that participation is incredibly weak, and volume remains very low. These aren’t signs of recovering bull market.

We did add some exposure.

On Thursday, we added some small energy exposures to portfolios. (XOM, CVX in the Equity Model and XLE in the ETF model.) As we noted at the time:

“We added positions in Exxon (XOM), Chevron (CVX), and the SPDR Energy ETF (XLE) to our portfolios. We believed the companies offered significant value before the crisis and offer even more today despite the sell-off in oil.

Based on our discounted cash flow model for XOM and CVX, we think that both stocks are about 25% undervalued. The model assumes very conservative earnings projections for the next three years and a low earnings growth rate after that.

In addition to trading at a good discount, we think their strong balance sheets put these companies in a prime position to purchase sharply discounted energy assets in the months ahead. These stocks and the sector will be volatile for a while, but we intend to add to these positions in the future and potentially hold them for a long time.”

On Friday, we added a position of TLT (20-year Treasury Bond ETF) to portfolios.

“As we continue to add some equity exposure in areas that we like or are undervalued, we are hedging that risk accordingly.

Previously, we reduced our bond portfolio to align with our reduced equity exposure, however, over the last few of weeks, we have been adding positions in CLX, MRK, CAG, XLE, XOM, and CVX, along with increasing exposures in our Staples (XLP), Healthcare (XLV) and Communications (XLC).

Today, we are increasing our bond exposure a “smidge” to compensate for the risk of increased equity exposure by adding a 5% weight of TLT (iShares 20-Year Treasury Bond) to portfolios. Such will increase our “duration,” so if the market declines, the pickup in yield will hedge equity risk to some degree.”

Our process is still to participate in markets while preserving capital through risk management strategies.

We will continue to trade opportunistically, but as noted last week, ultimately we WILL MISS the bottom. We are going to wait to see “the bottom” has been put in; then, we will aggressively add exposure. At such a point, risk and reward will be clearly in our favor.

We continue to remain very defensive and are in an excellent position with plenty of cash, reduced bond holdings, and minimal equity exposure in companies we want to own for the next 10-years. Just remain patient with us as we await the right opportunity to build holdings with both stable values, and higher yields.

Please don’t hesitate to contact us if you have any questions or concerns.

Lance Roberts

CIO