Written by Lance Roberts, Clarity Financial

Market Rallies Into The “Resistance Zone”

This week’s post is somewhat condensed as the bulk of our current positioning is based upon the information contained in the two reports referenced herein. The goal of this week’s letter is simply to outline the market ranges which fall within the context of our current Macroview.

Please share this article – Go to very top of page, right hand side, for social media buttons.

With that said, let’s get to work.

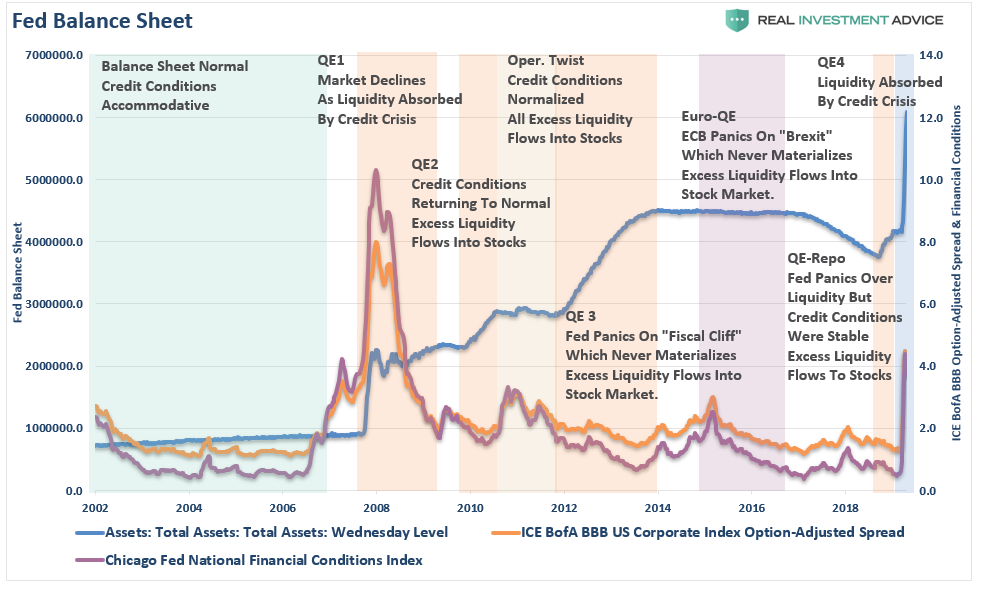

In this week’s #MacroView, I reviewed the history of monetary programs and the training of investors to respond to the “ringing of the bell.”

“As each round of ‘Quantitative Easing’ was the ‘neutral stimulus,’ which was followed by the ‘potent stimulus’ of higher stock prices, Not surprisingly, after a decade of ‘ringing the bell,’ investors have been conditioned to respond accordingly.

It is worth a trip back through history to evaluate the relationship between the Fed’s monetary interventions, and the impact on asset prices.”

While the report details the history of repeated rounds of monetary stimulus to offset potential “credit events” that never occurred, the most relevant period to review is 2008, which is most akin to the situation we are currently experiencing. A credit-event coupled with a major economic recession.

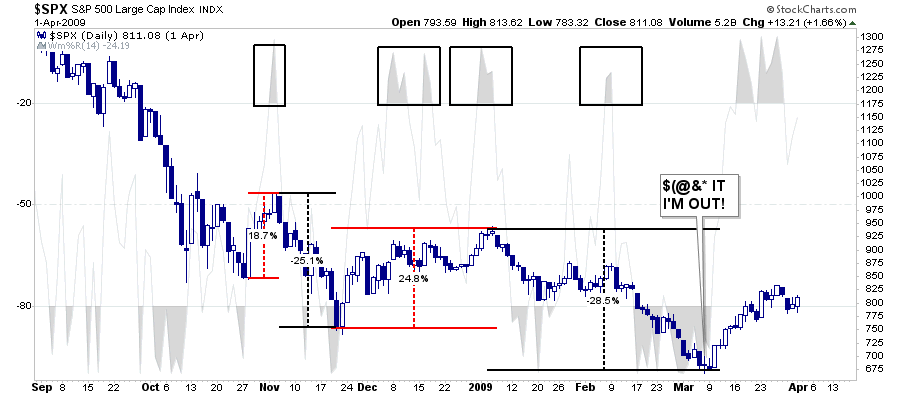

“2008: March – Bear Stearns fails, mortgage defaults start to rise, credit conditions worsen, and yield spreads rise. September – Lehman fails and freezes credit markets. Asset prices decline sharply, triggering margin calls, and the Fed floods the system with liquidity. As discussed last week:”

The reality of the economic devastation begins to set in as unemployment skyrockets, consumption and investment contract, and earnings fall nearly 100% from their previous peak, as the market declines 26% into late November. It was then the Federal Reserve launched the first round of Quantitative Easing.

Stocks staged an impressive rally of almost 25% from the lows. Yes, the bull market was back! Except that it wasn’t. Over the next few months, the Fed’s liquidity was absorbed by the “gaping economic wound,” and the market fell another 28.5% to its ultimate low.”

There are currently LOT’S of excuses to rationalize and justify the rally:

- The markets are looking past 2020 earnings.

- The market is looking at the eventual recovery.

- The market is rallying because of the Fed.

Rationalizing fundamentally unsupported advances typically have a “payback” consequence when you least expect it. This is particularly the case when you view the recent rally from a lens of:

- Never before seen levels of jobless claims

- Depression level unemployment rates

- An earnings and profit collapse

- The largest single GDP decline in history

- A loss of 1/3 of small businesses, which comprise nearly 45% of GDP.

- A loss of the biggest driver of asset prices over the last decade – stock buybacks.

As I discussed with our RIAPro Subscribers (30-day Risk Free Trial) on Friday:

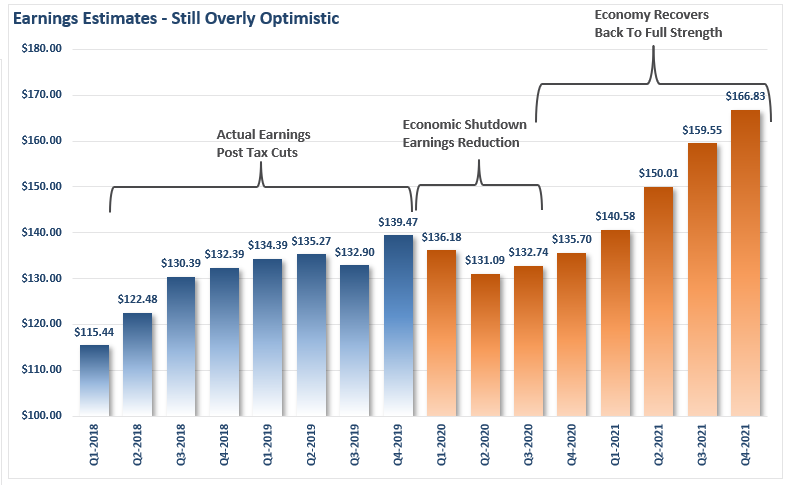

The chart below shows the most current estimates as of April 2020. As you can see, earnings are expected to decline from Q4-2019 levels of $139.47 to $136.18 and $131.09, respectively in Q1 and Q2 of 2020. That is a decline of -2.3% in Q1 and a total decline of -6% in Q2.”

“So, with the entire U.S. economy effectively shut down, 15-20% unemployment, and -20% GDP, earnings are only expected to take a 6% hit?

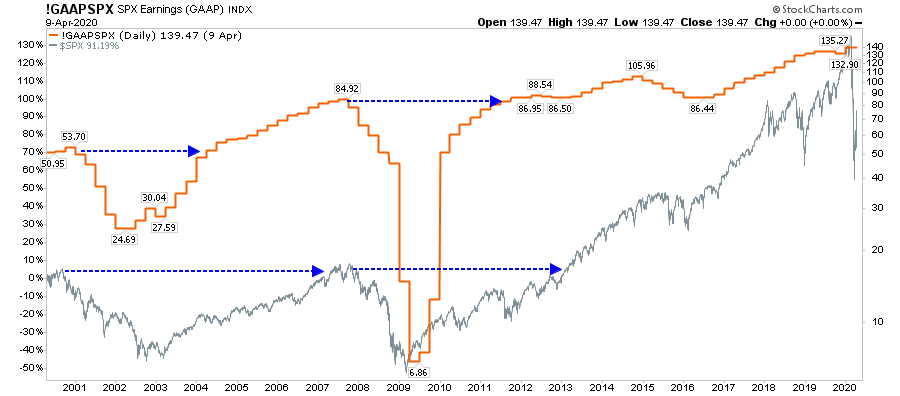

- In 2008, without an economic shutdown, S&P 500 earnings fell from $84.92 to $6.86. That is a decline of 92% from the peak, and earnings did not fully recover until 3-years later in Q3-2011.

- Or in 2000, during the “dot.com crash,” earnings fell from $53.70 to $24.69, or a decline of 54%. Earnings did not fully recover until 4-years later in Q2-2004.”

Do you really believe that stocks have priced in a real earnings collapse?

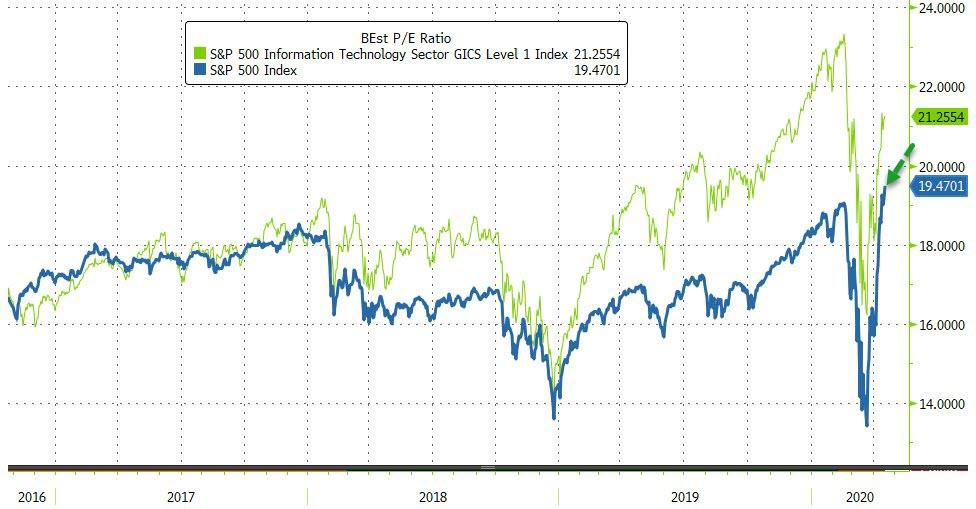

If you honestly think they have, then why is the market trading at 19x forward operating earnings, which is higher than both 2002, and the February 2020 peak?

As I stated in last week’s missive:

“While 2008 was bad, the impact from the ‘economic shutdown’ due to the virus will be substantially worse for several reasons:

- In 2008, the economy was already slowing down, unemployment was already on the rise, and businesses were adjusting for the related impact to earnings. Also, despite the ‘crisis’ caused in the mortgage market, businesses and consumer activity remained ‘open.’ Outside of the real estate and finance industries, many other sectors were only marginally affected.

- In 2020, the shuttering of the economy caught many businesses ‘flat-footed’ and ill-prepared for an involuntary ‘shuttering’ of business.

- In 2020, the surge in unemployment, combined with a shuttering of business, will have a substantially deeper impact on gross consumption in the economy than in 2008.

- As opposed to 2008, there are many businesses which will never reopen, many more will be very slow to recover, with the rest slow to rehire until demand returns.

The markets are currently rallying on a flush of liquidity, and a massive short-covering rally, which is likely reaching its “exhaustion” stage. Over the next few months, stocks will begin to price in the severity of the economic damage, a substantial decline in earnings, and the realization that hopes for a ‘V-Shaped’ recovery are not likely.”

Whatever rally is left currently in the market is still very likely a “gift” to sell into.

.