by Lance Roberts, Clarity Financial

Major Technical Failures Confirm Bear Market Risk

In last week’s discussion, we stated the “bear market” was not yet complete. This was despite the “market rally,” which convinced the media the “bull market was back.”

Please share this article – Go to very top of page, right hand side, for social media buttons.

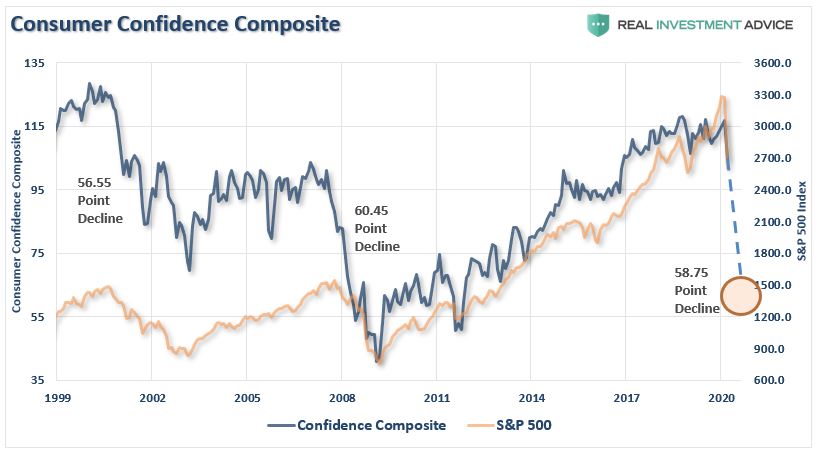

While it was indeed a sharp “reflex rally,” and expected, “bear markets” are not resolved in a single month. Most importantly, as we discussed in our employment report on Thursday, “bear markets” do not end with “consumer confidence” still very elevated.

“Notice that during each of the previous two bear market cycles, confidence dropped by an average of 58 points.”

This past week, we saw early indications of the unemployment that is coming to America as jobless claims surged to 10 million, and unemployment in April will surge to 15-20%.

Confidence, and ultimately consumption, Which comprises 70% of GDP, will plummet as job losses mount. It is incredibly difficult to remain optimistic when you are unemployed.

No Light At The End Of The Tunnel – Yet.

The markets have been clinging on to “hope” that as soon as the virus passes, there will be a sharp “V”-shaped recovery in the economy and markets. While we strongly believe this will not be the case, we do acknowledge there will likely be a short-term market surge as the economy does initially come back “online.” (That surge could be very strong and will once again have the media crowing the “bear market” is over.)

However, for now, we are not there yet. As we noted last week’s Macroview, there are two issues currently weighing on the economy and markets, short-term.

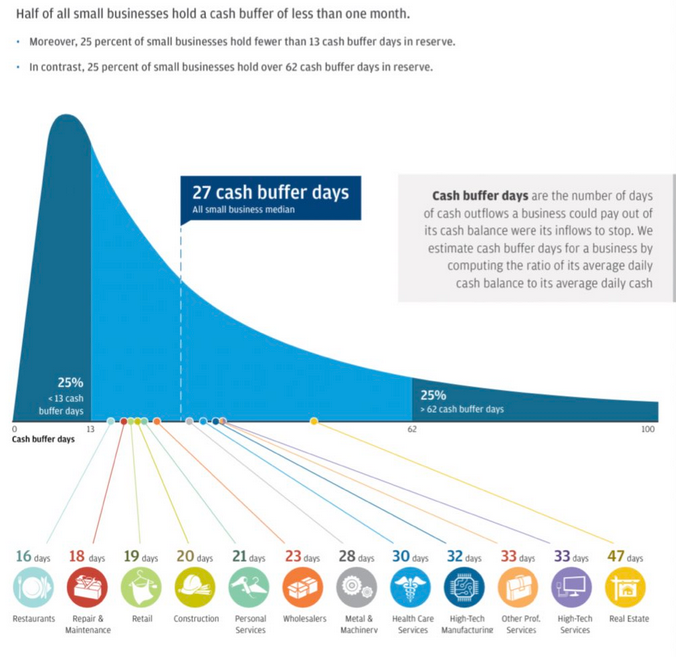

“Most importantly, as shown below, the majority of businesses will run out of money long before SBA loans, or financial assistance can be provided. This will lead to higher, and a longer-duration of unemployment.”

Furthermore, the bill only provides for two and a half times a company’s average monthly payroll expense over the past 12 months. However, the bill fails to take into consideration that not all small businesses are labor and payroll intensive. Those businesses will fail to receive enough support to stay in business for very long. Furthermore, the bill doesn’t provide for inventory, other operating costs, and spoilage.

Small businesses, up to 500-employees, make up 70% of employment in the U.S. While the government is busy bailing out self-dealing publicly traded corporations, there will be a massive wave of defaults in the small- to mid-size business sector.

Secondly, we are not near the end of the virus as of yet. As noted last week:

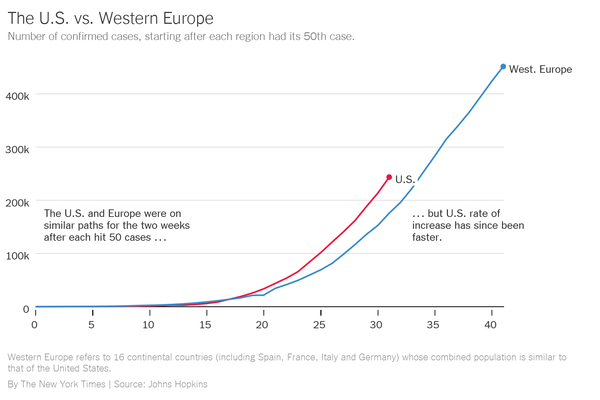

“While there is much hope that the current ‘economic shutdown’ will end quickly, we are still very early in the infection cycle relative to other countries. Importantly, we are substantially larger than most, and on a GDP basis, the damage will be worse.”

This was confirmed again this week by the New York Times’ columnist David Leonhardt:

“Five ways we know that the American response to the coronavirus isn’t yet working.

- There is still no sign of the curve flattening.

- The caseload is growing more rapidly here than in Europe.

- The shortage of medical supplies continues.

- There is still a testing shortage.

- Nationwide, the policy response remains inconsistent.

What the cycle tells us is that jobless claims, unemployment, and economic growth are going to worsen materially over the next couple of quarters.

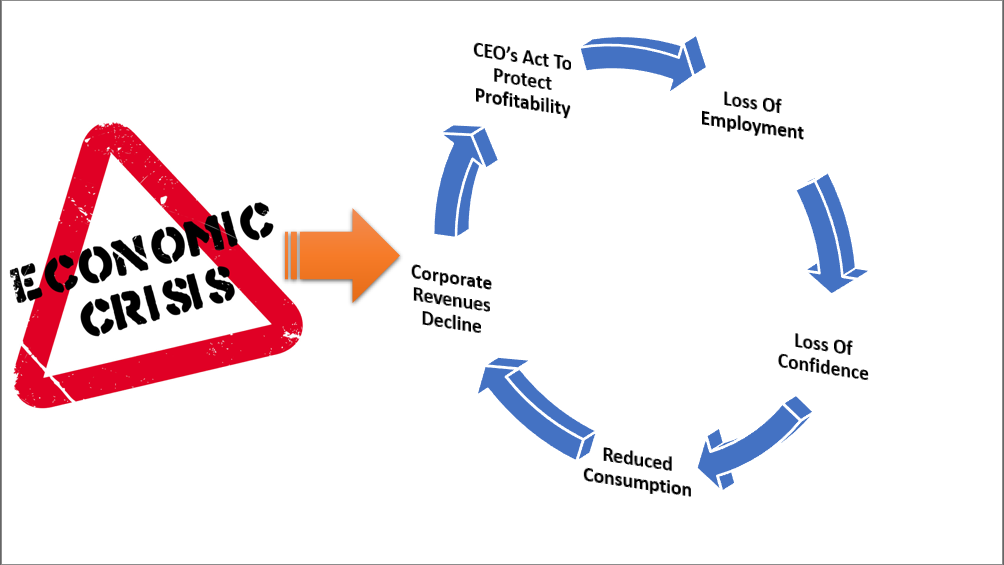

The problem with the current economic backdrop, and mounting job losses, is the vast majority of American’s were woefully unprepared for any disruption to their income going into recession. As job losses mount, a virtual spiral in the economy begins as reductions in spending put further pressures on corporate profitability. Lower profits lead to higher unemployment and lower asset prices until the cycle is complete.

Two important points:

- The economy will eventually recover, and life will return to normal.

- The damage will take longer to heal, and future growth will run at a lower long-term rate due to the escalation of debts and deficits.

For investors, this means a greater range of stock market volatility and near-zero rates of return over the next decade.

The Bear Still Rules

Over the last two weeks, we published several pieces of analysis for our RIAPro Subscribers (30-Day Risk Free Trial) discussing why the “bear market rally” should be sold into. On Friday, our colleague, Jeffery Marcus of TP Analytics, penned the following:

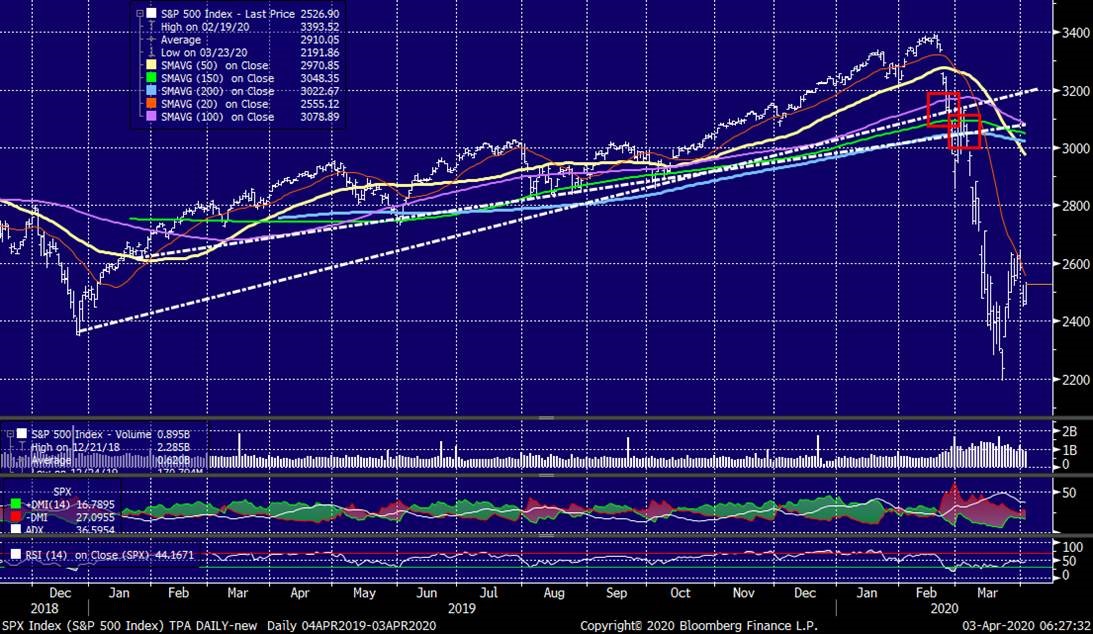

Meanwhile, the charts below of the S&P500 benchmark tell TPA the following:

- When the 11-year bull market trend ended, other shorter trends were also violated. In late February, the S&P 500 fell below its 14-month uptrend line, and in early March the 13-month uptrend line was violated. Those breaks set in place the steep declines seen in the 2nd and 3rd weeks of March.

- While it may seem like an epic battle is going on around S&P 500 2500, the real problem is the downtrend forming from the 2/19 high.

- TPA still continues to see real long term support in the 3% range between 2110 and 2180. A less likely move below that support, would leave long term support levels of the lows of 2014 and 2015.

S&P 500 – Long Term

His analysis agrees with our own, which we discussed with you on Tuesday:

“While the technical picture of the market also suggests the recent “bear market” rally will likely fade sooner than later. As we stated last week:

‘Such an advance will ‘lure’ investors back into the market, thinking the ‘bear market’ is over.’

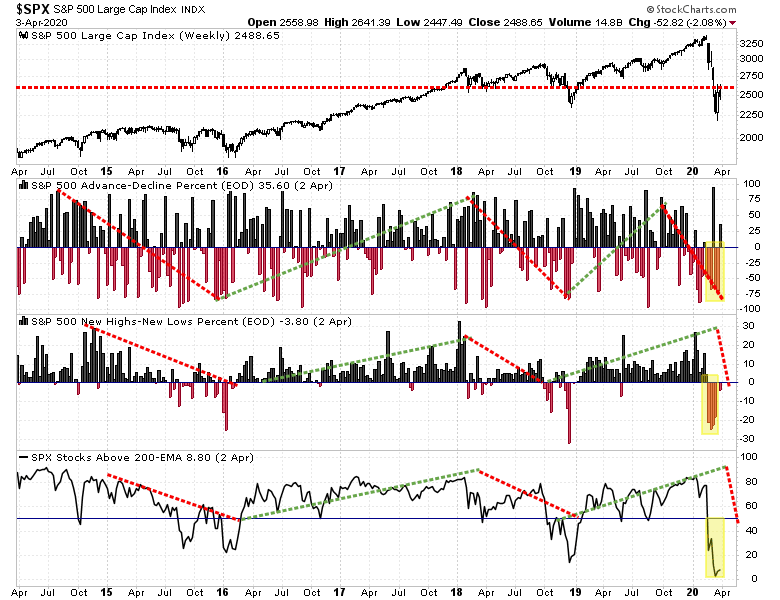

Importantly, despite the sizable rally, participation has remained extraordinarily weak. If the market was seeing strong buying, as suggested by the media, then we should see sizable upticks in the percent measures of advancing issues, issues at new highs, and a rising number of stocks above their 200-dma.”

Chart updated through Friday.

On a daily basis, these measures all have room to improve in the short-term. However, the market has now confirmed longer-term technical signals suggesting the “bear market” has only just started.

We discuss these technical signals in an article to be published in two days: “Major Technical Failures”.

.