Written by Lance Roberts, Clarity Financial

“If you own 10% equities, as we do, and the market falls 100%, you will lose 10%. That said, you have 90 cents on the dollar to buy equities for free.”

. . – – Michael Lebowitz

Let me explain his comment.

Last week, we wrote a piece titled When Too Little Is Too Much in which we discussed reducing our equity risk to our lowest levels.

For the last several months, we have been issuing repeated warnings about the market. While such comments are often mistaken for “being bearish,” we have often stated it is our process of managing “risk,” which is most important.

Beginning in mid-January, we began taking profits out of our portfolios and reducing risk. To wit:

‘On Friday, we began the orderly process of reducing exposure in our portfolios to take in profits, reduce portfolio risk, and raise cash levels.’

Importantly, we did not ‘sell everything’ and go to cash.

Since then, we took profits and rebalanced risk again in late January and early February as well.

On Friday/Monday, our ‘limits’ were breached, which required us to sell more.”

There are a couple of important things to understand about our current equity exposure.

To begin with, we never go to 100% cash. The reason is that “psychologically” it is too difficult for clients to start “buying” when the market finally bottoms. Seeing the market begin to recover, along with their portfolio, makes it easier to fight the fear the market is “going to zero.”

Secondly, and most importantly, at just 10% in current equity exposure, the market could literally fall 100% and our portfolios would only decline by 10%. (Of course, given we still have 90% of our capital left, we can buy a tremendous amount of “free assets.”)

Of course, the market isn’t going to zero.

However, let’s map out a more realistic example.

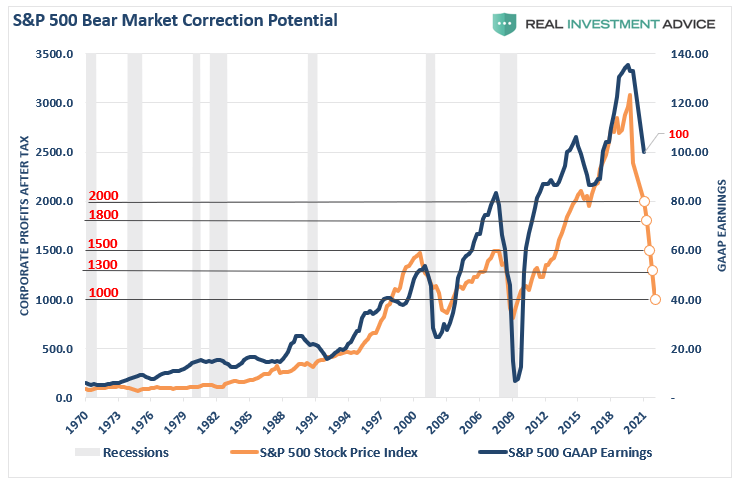

In this week’s MacroView, we discussed the “valuation” issue

“If our, and Mr. Rosenberg’s, estimates are correct of a 5-8% recessionary drag in the second quarter of 2020, then an average reduction in earnings of 30% is most likely overly optimistic.

However, here is the math:

- Current Earnings = 132.90

- 30% Reduction = $100 (rounding down for easier math)

At various P/E multiples, we can predict where “fair value” for the market is based on historical assumptions:

- 20x earnings: Historically high but markets have traded at high valuations for the last decade.

- 18x earnings: Still historically high.

- 15x earnings: Long-Term Average

- 13x earnings: Undervalued

- 10x earnings: Extremely undervalued but aligned with secular bear market bottoms.

You can pick your own level where you think P/E’s will account for the global recession but the chart below prices it into the market.”

So, let’s assume our numbers are optimistically in the “ballpark” of a valuation reversion, and earnings are only cut by 30% while the market bottoms at 1800, or 18x earnings. (I say optimistically because normal valuation reversions are 15x earnings or less.)

Here’s the math:

- For a “buy and hold” investor (who is already down 20-30% from the peak) will lose an additional 22%.

- For a client with 10% equity exposure, they will lose an additional 2.2%.

When the market does eventually bottom, and it will, it will be far easier for our clients to recover 10% of their portfolio versus 50% for most “buy and hold” strategies.

As we have often stated, “getting back to even is not an investment strategy.“

.