Written by Lance Roberts, Clarity Financial

Sector & Market Analysis:

Be sure and catch our updates on Major Markets (Monday) and Major Sectors (Tuesday) with updated buy/stop/sell levels

Please share this article – Go to very top of page, right hand side, for social media buttons.

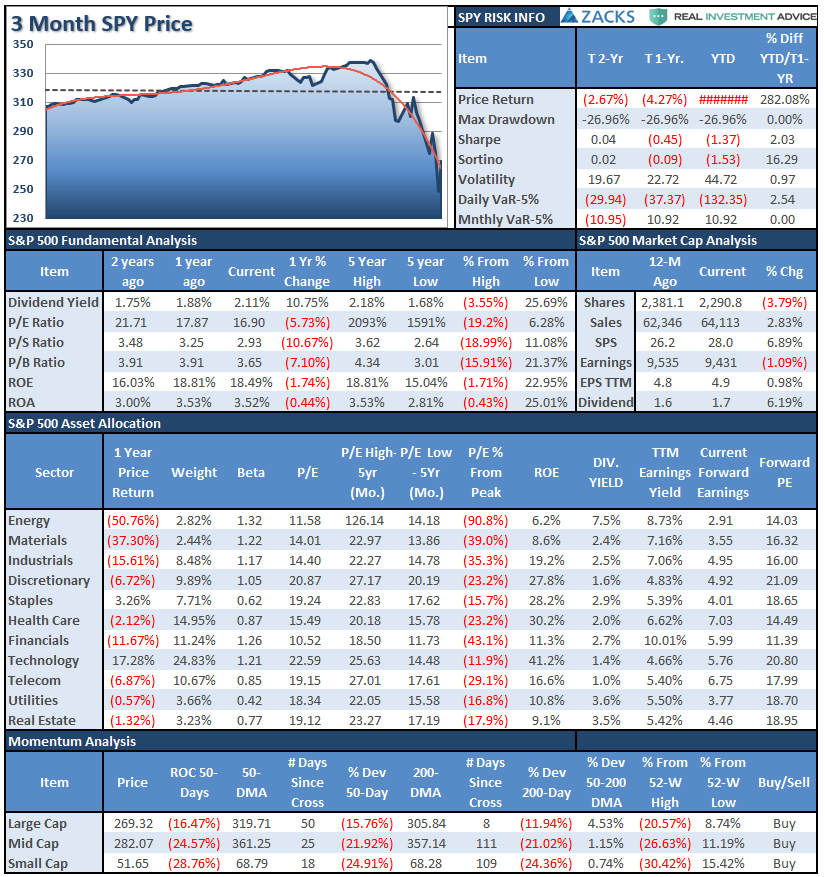

S&P 500 Tear Sheet

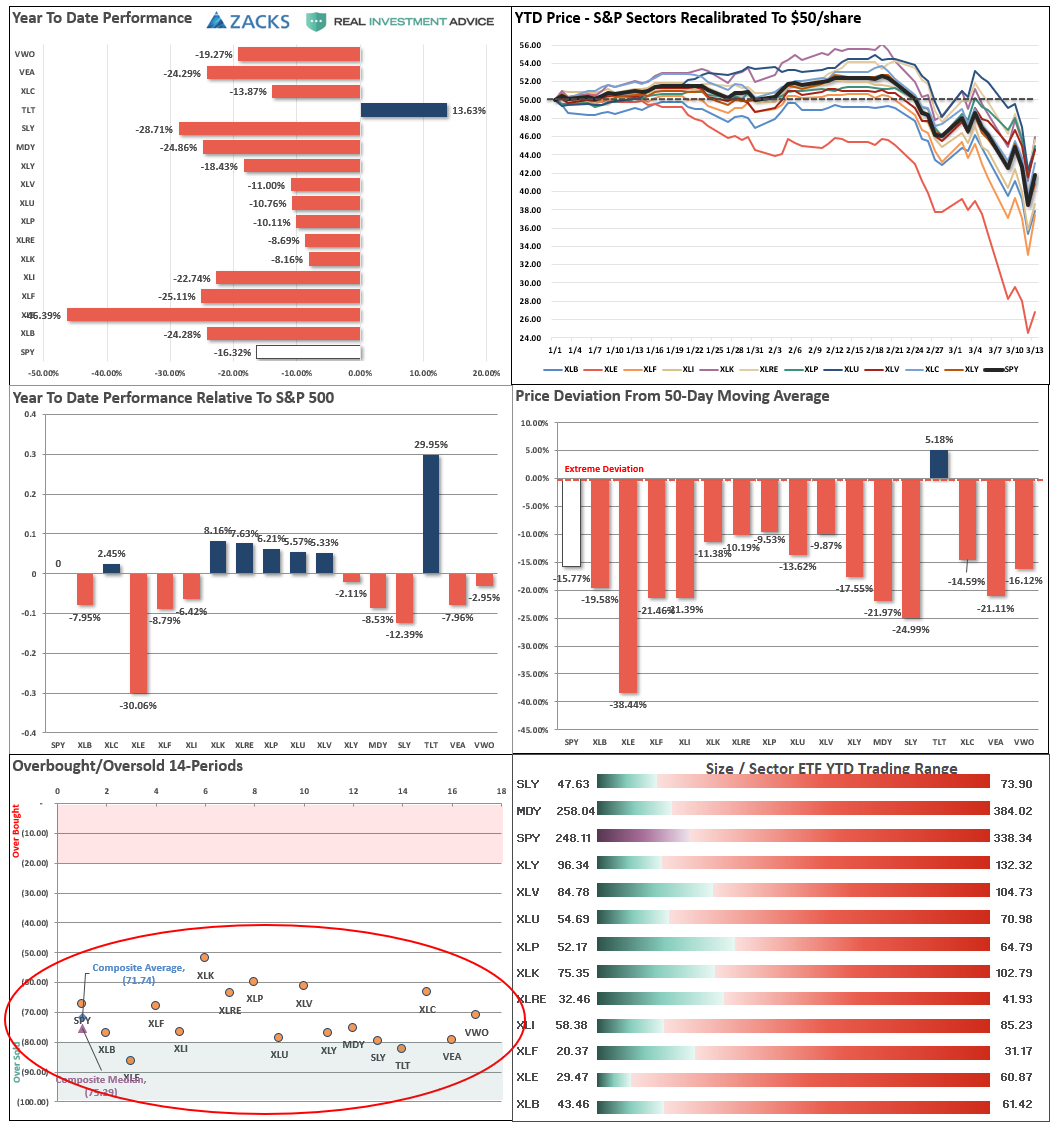

Performance Analysis

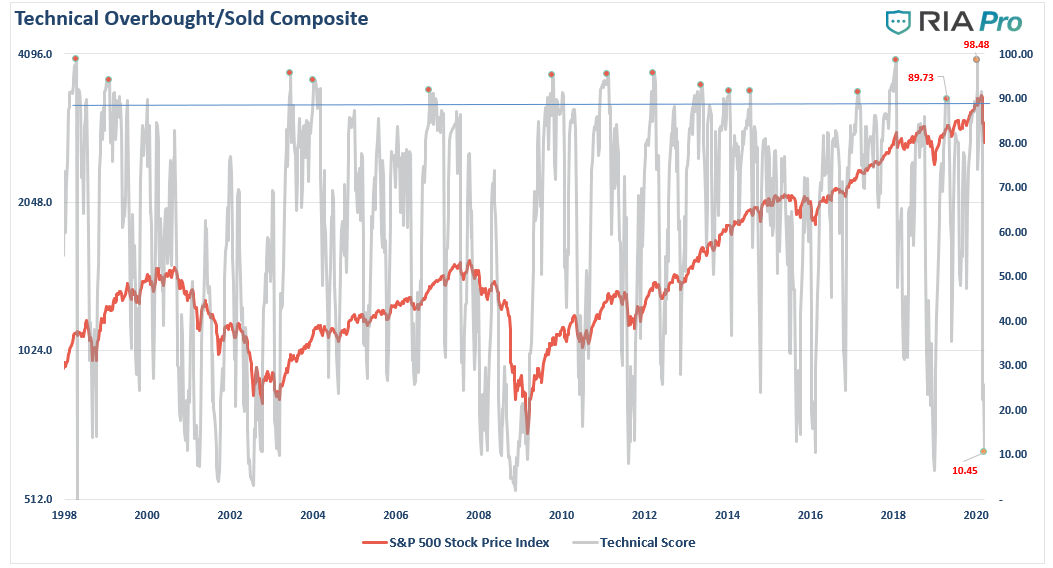

Technical Composite

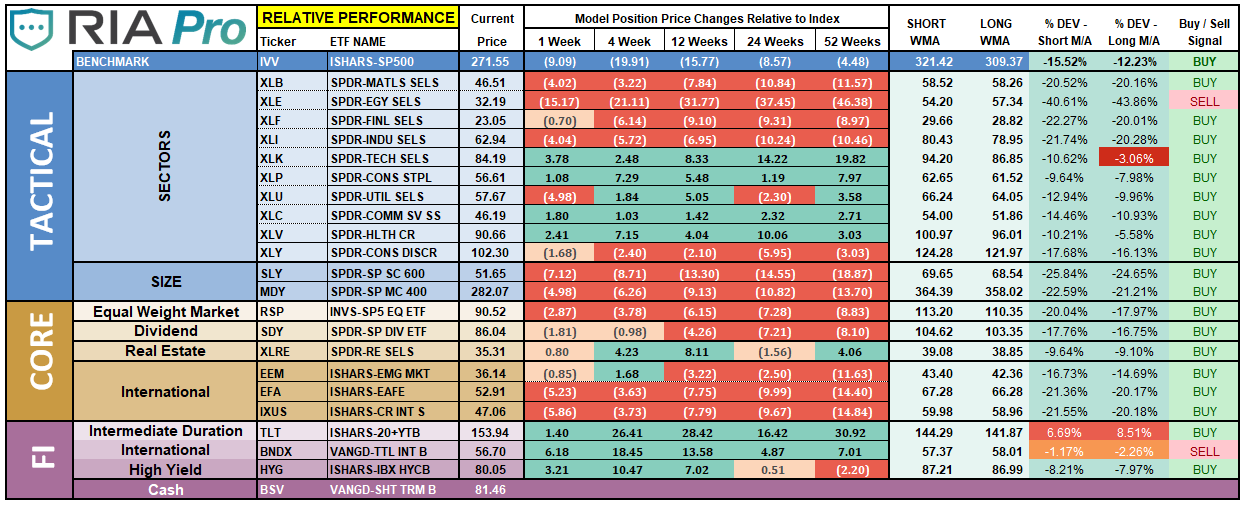

ETF Model Relative Performance Analysis

Sector & Market Analysis:

Be sure and catch our updates on Major Markets (Monday) and Major Sectors (Tuesday) with updated buy/stop/sell levels

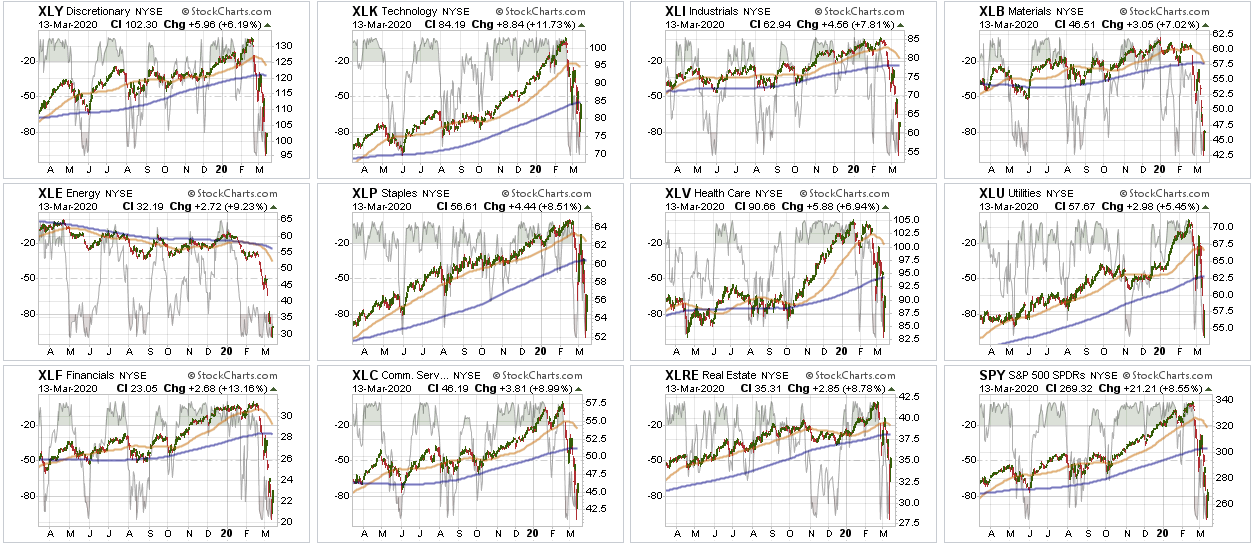

Sector-by-Sector

Everything was crushed again this past week, so the difference between leading and lagging sectors is which sector fell faster or slower than the S&P 500 index itself.

Improving – Discretionary (XLY), Real Estate (XLRE), and Staples (XLP)

Last week, we rebalanced our weightings in Real Estate and Staples, as these sectors are now improving in terms of relative performance. After getting very beaten up, we are looking not only for the “risk hedge” of non-virus related sectors but an eventual outperformance of the groups.

We sold our entire stake in Discretionary due to potential earnings impacts from a slowdown in consumption, supply chain problems, and inventory issues. This worked well as Discretionary fell sharply last week.

Current Positions: Target Weight XLU, XLRE

Outperforming – Technology (XLK), Communications (XLC), and Utilities (XLU)

The correction in Technology this past week broke support at the 200-dma but finished the week very close to our entry point, where we had slightly increased our exposure. These have “anti-virus” properties, so we are looking for the “risk hedge” relative to the broader market. Communication and Utilities didn’t perform as well but also held up better during the decline on a relative basis. We are watching Utilities and may reduce exposure if interest rates begin to rise due to the Fed. The same with Real Estate as well.

Current Positions: Target weight XLK, XLC, XLU

Weakening – Healthcare (XLV)

We did bring our healthcare positioning back to portfolio weight as the sector will ultimately benefit from a “cure” for the “coronavirus.” Also, with Bernie Sanders now lagging Joe Biden on the Democratic ticket, this removes some of the risks of “nationalized healthcare” from the sector.

Current Position: Target weight (XLV)

Lagging – Industrials (XLI), Financials (XLF), Materials (XLB), and Energy (XLE)

We had started to buy a little energy exposure previously but closed out of the positions as we were stopped out of our holdings week before last. We are going to continue to monitor the space due to its extreme oversold condition and relative value and will re-enter our positions when stability starts to take hold.

We also sold Financials due to the financial risk from a recessionary impact on the outstanding corporate debt which currently exists. The Fed’s rate cut also impacts the bank’s Net Interest Margins, which makes them less attractive. Industrials and Materials have too much exposure to the “virus risk” for now.

Current Position: None

Market By Market

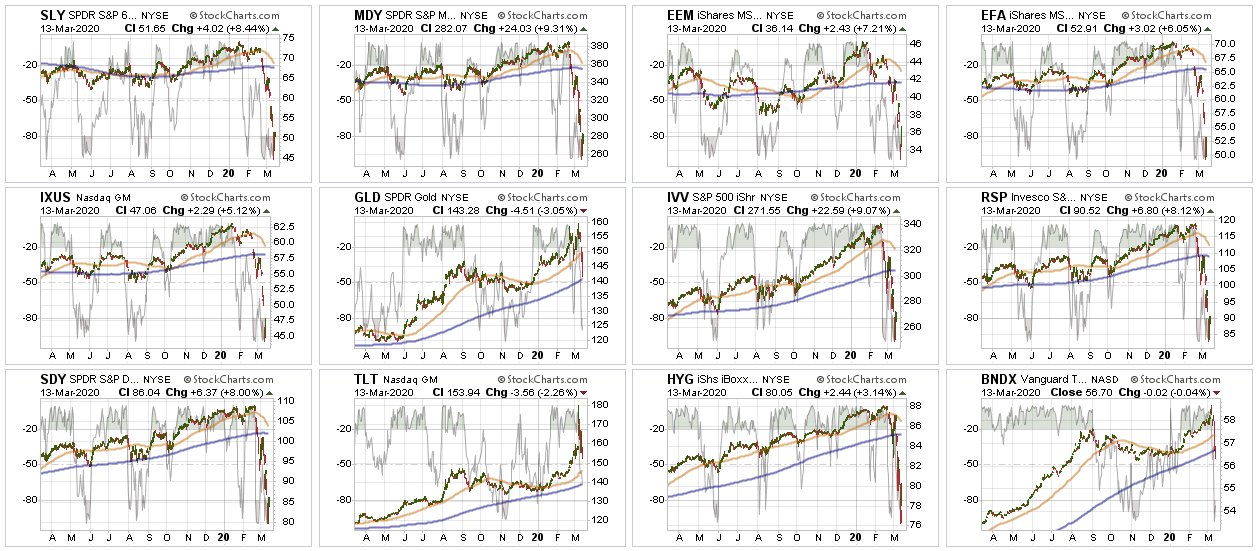

Small-Cap (SLY) and Mid Cap (MDY) – Week before last, we sold all small-cap and mid-cap exposure over concerns of the impact of the coronavirus. Remain out of these sectors for now. However, given that Central Banks are going “all in” on stimulus, we may look for a trade in these sectors short-term.

Current Position: None

Emerging, International (EEM) & Total International Markets (EFA)

Same as small-cap and mid-cap. Given the spread of the virus and the impact on the global supply chain. Trading opportunity only.

Current Position: None

Dividends (VYM), Market (IVV), and Equal Weight (RSP) – We have decided to consolidate our long-term “core” holding into IVV only. We sold RSP and VYM and added to IVV. The reason for doing this is the disparity of performance between the 3-holdings. Since we want an “exact hedge” for our portfolio, IVV is the best match for a short-S&P 500 ETF.

Current Position: IVV

Gold (GLD) – This past week, Gold sold off as the Fed introduced liquidity giving the bulls hope and removing the “fear” factor in stocks. There was also a massive “margin call” that led to a liquidation event. Gold is VERY oversold currently. Add positions to portfolios with a stop $140. We sold our GDX position due to the fact mining is people-intensive and is located in countries most susceptible to the virus.

Current Position: IAU (GOLD)

Bonds (TLT) –

Bonds also broke out to new highs as the correction ensued. Last Friday, we took profits in our 20-year bond position (TLT) to reduce our duration slightly, raise cash, and take in some profits. Bonds are extremely overbought now, so be cautious, we are maintaining the rest of our exposures for now, but we did rebalance our duration by selling 1/2 of IEF and adding to BIL.

Current Positions: DBLTX, SHY, IEF, PTIAX, BIL

Sector / Market Recommendations

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

Thank goodness. The market finally responded to the Fed on Friday.

As noted last week:

“Staying true to our discipline and strategy is difficult when you have this type of volatility. We question everything, every day. Are we in the right place? Do we have too much risk? Are we missing something?

The ghosts of 2000, and 2008, stalk us both, and we are overly protective of YOUR money. We do not take our jobs lightly.”

We took some further actions to increase cash, further rebalance risks this past week. We are now using this rally to add hedges, and reduce equities until the current “sell signals” reverse. As noted, this is most likely a “bear market” rally that will fail.

However, if it is the beginning of a new “bull market,” then we will simply remove hedges and add to our equity longs.

Be assured we are watching your portfolios very closely. However, if you have ANY questions, comments, or concerns, please don’t hesitate to email me.

Portfolio Actions Taken Last Week

- New clients: Only adding new positions as needed.

- Dynamic Model: Sold VOOG, and hedged portfolio. Currently unhedged.

- Equity Model: Sold IEF and added to BIL to shorten bond portfolio duration. Sold RSP and VYM, and added slightly to IVV to rebalance our CORE holdings for more effective hedges.

- ETF Model: Same as Equity Model.

Note for new clients:

It is important to understand that when we add to our equity allocations, ALL purchases are initially “trades” that can, and will, be closed out quickly if they fail to work as anticipated. This is why we “step” into positions initially. Once a “trade” begins to work as anticipated, it is then brought to the appropriate portfolio weight and becomes a long-term investment. We will unwind these actions either by reducing, selling, or hedging if the market environment changes for the worse.

.