Written by Lance Roberts, Clarity Financial

We Don’t Know What Happens Next

Last week, we discussed “Navigating What Happens Next,“ and set out to answer 3-important questions:

- Is the correction over?

- Is this a buying opportunity?

- Has the decade long bull market ended?

Please share this article – Go to very top of page, right hand side, for social media buttons.

We also included a set of “rules to follow,” based on our analysis.

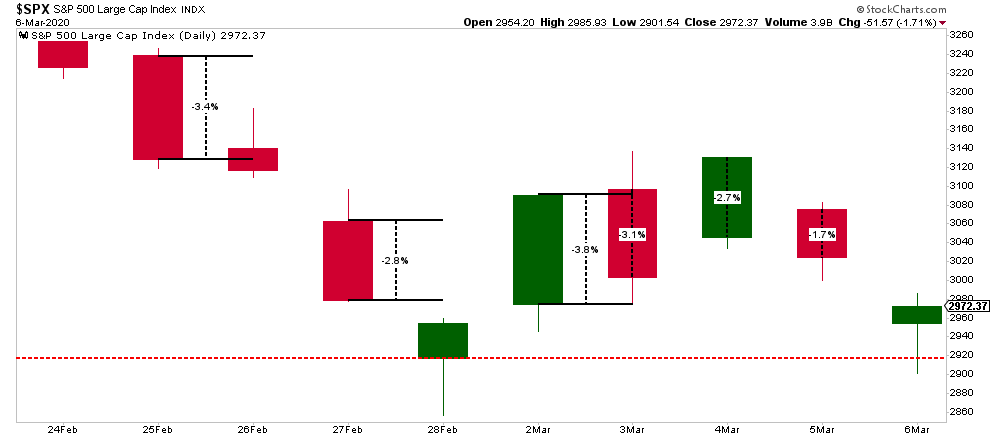

Importantly, while we have adhered to our investment process and discipline, to protect capital while participating in the markets, the volatility over the last couple of weeks has been unnerving to say the least. The chart below shows the daily percentage swings.

With markets swinging wildly by 2-3% daily, it has been more nauseating than the 418-foot drop of the Kingda Ka roller coaster in Jackson, NJ. While it seems like last week was another “horrible” week for the market, it actually ended slightly above where we ended last week.

It’s important to keep some perspective with respect to your portfolio management, particularly when volatility surges. Emotions are the biggest risk to your investments, and capital, over time.

We Really Don’t Know

While we laid out a fairly detailed game plan last week, looking a daily, weekly, and monthly indicators, the reality is that we don’t know with any certainty what happens next, particularly when you have an exogenous situation like “COVID-19.”

However, we agree with Carl Swenlin that you can’t rule out a “bear market” has now started, like we saw in 2018, and the highs of the year are in.

“Even though it is not officially a bear market, I think we should begin to interpret charts and indicators in the context of a bear market template.”

We agree, particularly within the scope of the comments made by my colleague Doug Kass on Friday morning:

“The proximate cause for the precipitous drop in yields is the spread of the coronavirus – which is delivering a body blow to global economic growth (which will come to a standstill in the months ahead).

In all likelihood, world GDP growth will likely be flat over the next few months – to unnaturally low levels of activity. To be sure some segments of the economy (in this reset) will not recoup sales and will have a permanent loss, i.e., hotels, travel, etc.

However, other segments of the economy – like technology – will likely recoup almost all the growth delayed by the coronavirus shock.

The next few months will be challenging from an economic standpoint and volatile from a stock market perspective. Moreover, evolving market structure issues will introduce more uncertainty – and likely deliver a continuation of the extreme volatility seen since mid-February.”

We agree with Doug’s view and have spent the last month moving OUT of areas like Basic Materials (XLB), Industrials (XLI), Discretionary (XLY), Energy (XLE), Transports (XTN), and Financials (XLF).

While financials don’t have as much direct “virus” related risk, the risk to major banks is two-fold:

- The collapse in “net interest margins” as the Fed cuts rates; and

- Potential for a wave of corporate-debt defaults coming from the economic slowdown/recession, particularly in the Energy sector.

The second point was noted by Mish Shedlock on Friday:

“There is a credit implosion coming up. A lot of leveraged drillers and crude suppliers dependent on prices above $50/bbl are going to facing credit defaults.

This will lead to a deflationary outcome. But you can blame the Fed.

Deflation is not really about prices. It’s about the value of debt on the books of banks that cannot be paid back by zombie corporations and individuals.”

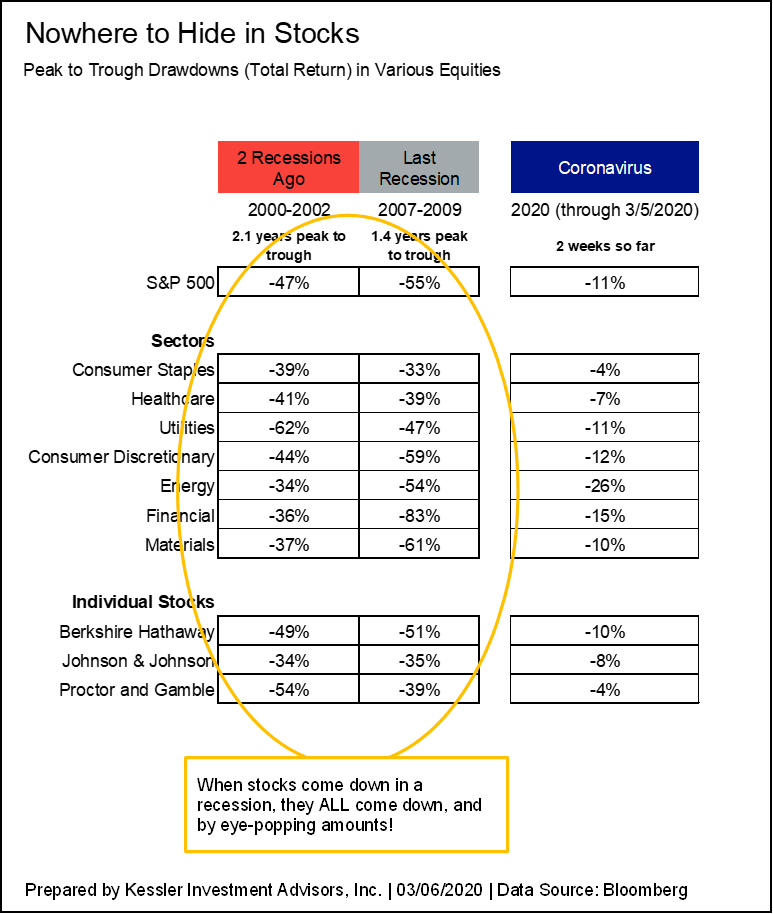

Collapsing yields, oil prices, and “emergency rate cuts,” are signs which suggest something has “broken” in the economy. These ramifications are not inconsequential. My friend Eric Hickman, of Kessler Investment Advisors, sent me an excellent note on Friday:

“Unsurprisingly, I think that the Coronavirus is the catalyst to tip the U.S. into a recession. We all know that recessions are not good for stocks, but by how much, and which ones?

The last two recessions hit all sectors of the S&P 500 significantly. Even so-called “defensive sectors” like consumer staples and healthcare got hit by at least a third of their value (33%). We are just two weeks, and 11% away from an all-time high in the S&P 500. There is plenty of downside left.”

He is right.

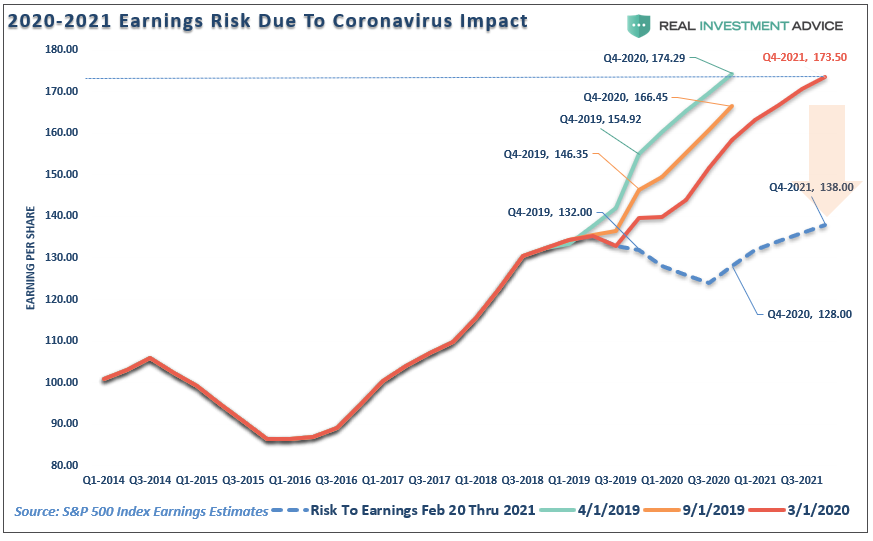

What we know, with almost absolute certainty, is that we will be in an economic recession within the next couple of quarters. We also know that earnings estimates are still way too elevated to account for the disruption coming from the COVID-19.

What we DON’T KNOW is where the ultimate bottom for the market is. All we can do is navigate the volatility to the best of our ability and recalibrate portfolio risk to adjust for downside risk without sacrificing the portfolio’s ability to quickly adjust for a massive “bazooka-style” monetary intervention from global Central Banks if needed.

This is why, over the last 6-weeks, we have been getting more “defensive” by increasing our CASH holdings to 15% of the portfolio, with our 40% in bonds doing the majority of the heavy lifting in mitigating the risk in our remaining equity holdings.

Regardless, of the hedges and cash, the portfolio management process over the last two weeks has not been pretty and has frayed our nerves. (Despite our best efforts, we are still subject to human emotions). However, for the year, the Sector Rotation model is down 1.7% versus 9% for the S&P 500.

That is volatility we can live with.

.