Written by Lance Roberts, Clarity Financial

We have had quite a few emails from readers over the past week asking why we were “buying” into our RIAPRO portfolios this past week. (You can register for a 30-day RISK-FREE trial if you want to view our current portfolios.)

Please share this article – Go to very top of page, right hand side, for social media buttons.

The short answer is:

“Because that is what our process required us to do.”

To understand the process, we have to go back.

A few weeks ago, Shawn Langlois at MarketWatch picked up our article discussing why we were selling positions in our portfolio. To wit:

“Specifically, Roberts raised cash by selling off shares of Apple, Microsoft, United Healthcare, Johnson & Johnson, and Micron, and scaling back overweight holdings in various ETF sector plays, such as the Technology Select Sector SPDR, and the Health Care Select Sector.“

While at the time, it seemed like a wrong move, a couple of weeks later, the market sold off. The benefit was the extra cash, and reduced exposure, help limit the downside draw to about 1/3rd of the market decline.

Then, last week, things changed:

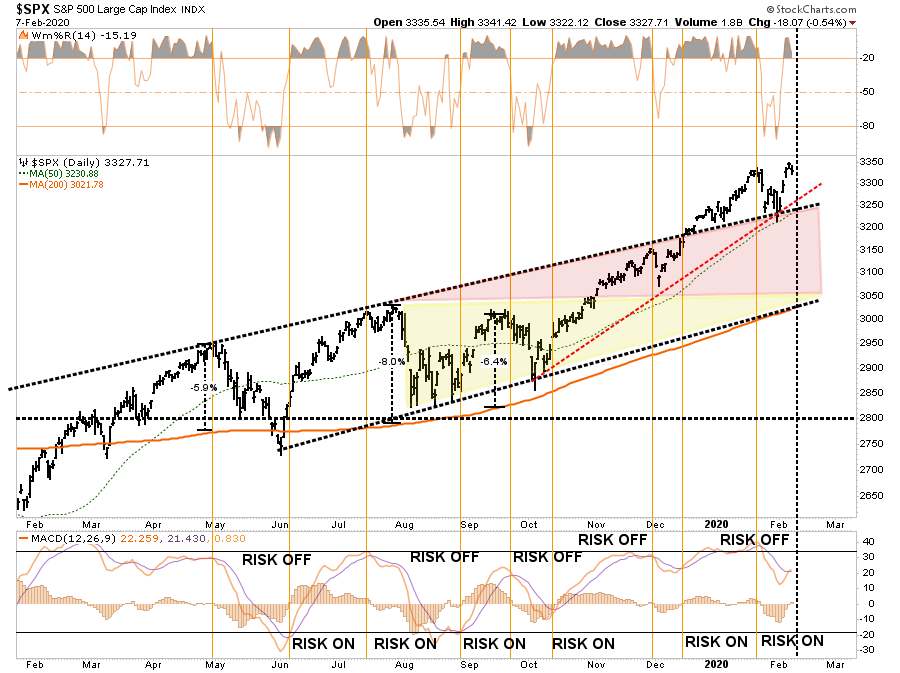

“With bond yields plummeting this past week, our bond exposures have gotten extremely stretched. The sell-off in the market, combined with the ‘risk off’ rotation to bonds, sets the market up for a reflexive bounce. The duration and magnitude of that bounce will be critical as to our next steps in positioning.”

Chart updated through Friday

As noted, the market had gotten oversold on a short-term basis, which brought the risk/reward measures back into better alignment. This is where our process required we add equity exposure back into portfolios.

- In the ETF Model, we added Financials (XLF) and increased our stake in HealthCare (XLV) with both of those sectors having gotten oversold and bouncing off their respective 50-dma’s.

- In the EQUITY Model, we added JP Morgan (JPM) and Pfizer (PFE) while increasing our stakes in Abbvie (ABBV), United Healthcare (UNH), and Alerian MLP (AMLP).

Importantly, this rebalancing of risk did not dramatically increase our equity exposure. This is because, as noted above, the longer-term technical outlook remains “cautious.”

Yes, we realize we are very late-cycle, we also know that with the Fed, and global Central Banks, still intervening, we must give deference to the “bullish bias.” At the moment, the bullish bias remains, and functioned as we predicted last week.

“The ‘bullish bias’ is not dead as of yet, and investors will be quick to try and ‘write off’ the impact of the ‘virus.’ After a decade of ‘macro-events’ not stopping the bullish charge, the belief the market is ‘bulletproof’ has become so deeply ingrained into investor mentality it won’t be dislodged until it is far too late to matter.”

We have no certainty about when, or what will trigger the next bear market.

What we do know is that such an event will likely be far more brutal than most realize due to years of excess risk-taking, leverage, and demographics.

However, this is what our process is designed to handle:

- The portfolio is managed for risk by adjusting the level of equity exposure relative to market dynamics, return outlooks, and technical deviations from long-term means.

- The allocation is managed for risk by balancing positions for relative performance to our benchmark.

- The positions are managed for risk by:

- Employing trailing stop-losses

- Regularly rebalancing positions back to target weights (taking profits)

- Cutting laggards which aren’t performing as expected

- Monitoring relative performance and participation

Importantly, notice that everything the process covers is the management against the “risk” of loss.

If we manage against the risk of capital loss, we can safely participate with markets as they rise. When something eventually does goes wrong, the process will systematically close out positions, protecting our investment capital, until that process is complete. Then the process reverses to rebuild exposure when risk/reward dynamics are greatly improved.

As long as the process is followed, risk can be controlled. Where the majority of investors go wrong, is by not having a process.

“Hoping” markets will continue higher indefinitely, is not a process.

As we concluded last week:

“We won’t know for sure until after the fact. This is why we manage risk in the short-term. Managing risk allows us to navigate the ‘twists and turns’ of the market without careening off the cliff.”