Written by Lance Roberts, Clarity Financial

Last week, I asked the question: “Is The Correction Over?“ To wit:

“On a very short-term basis, there is a potential for a reflexive bounce. If your ‘investment duration,’ or rather your ‘investment holding period’ is very short, there may be a ‘trading’ opportunity for you.”

Please share this article – Go to very top of page, right hand side, for social media buttons.

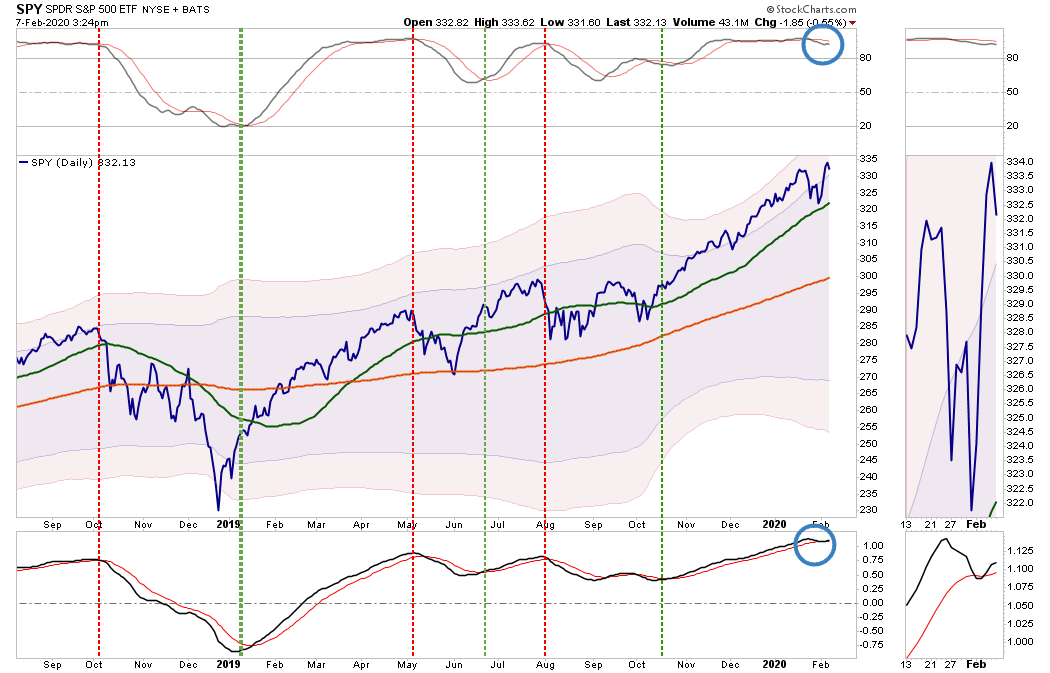

Well, that bounce came hard and fast during the first half of the week, as the S&P 500 rebounded off the 50-dma to set new highs on Thursday.

The Good News

As noted, the market bounced firmly off the 50-dma and rallied back to new highs on Thursday. While Friday saw a bit of retracement, which isn’t surprising given the torrid move early in the week, the “virus correction” was recovered. Importantly, the “buy signal,” in the lower panel, was close to registering a “sell signal.” The sharp early-week rally kept that signal from triggering, which would have confirmed the “sell signal” in the top panel. Historically, when both “sell signals” are triggered, deeper corrections have tended to follow.

The Not-So-Good News

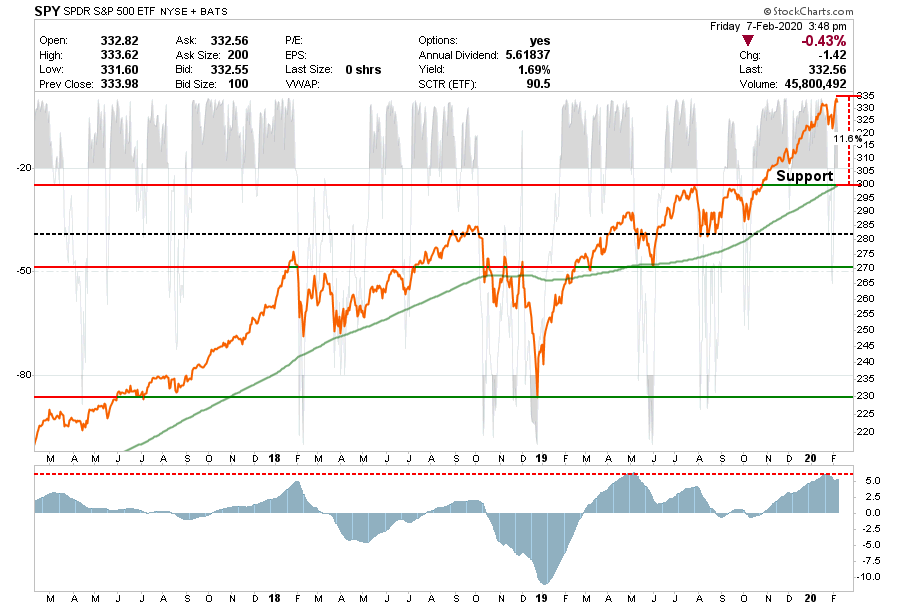

Previously, we discussed that we had taken profits out of portfolios as we were expecting between a 3-5% correction to allow for a better entry point to add equity exposure. While the “virus correction” did encompass a correction of 3%, it was too shallow to reverse the rather extreme extension of the market. The rally this past week has reversed the corrective process, and returned the markets to 3-standard deviations above the 200-dma. Furthermore, all daily, weekly, and monthly conditions have returned to more extreme overbought levels as well.

Of course, the reason for the rally was more liquidity from the Federal Reserve.

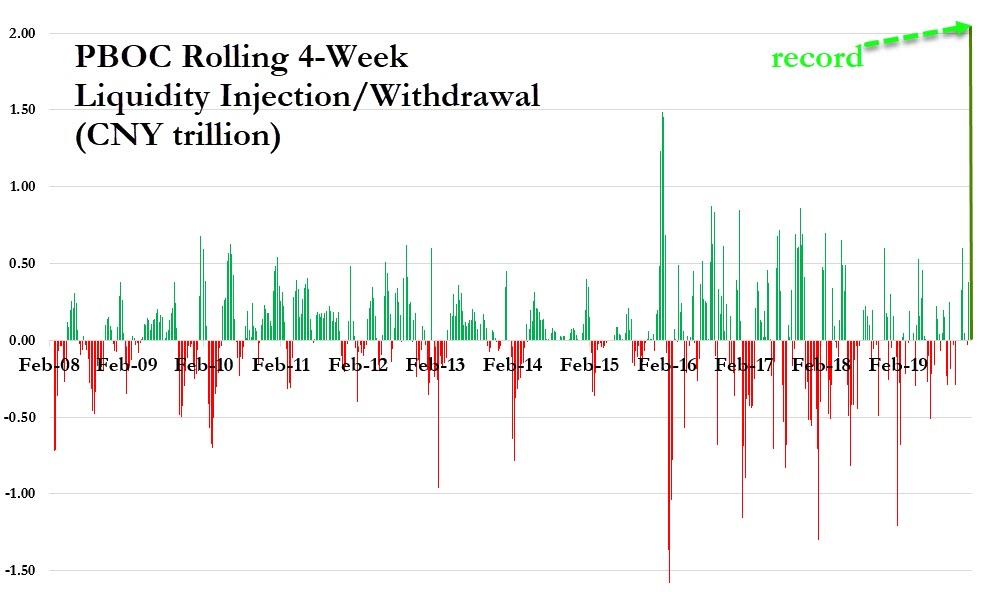

While the economic impact from the virus is likely to be substantial, as discussed previously, traders looked past economic realities. They focused instead on more liquidity being pumped into the markets by both the Fed, and the PBOC (Peoples Bank of China).

“The PBOC decided that instead of unwinding the large liquidity provision, they would double-down on it… and that they did in size. The last four weeks have seen China supply over CNY2 trillion (net!) into its financial system – something we have never seen anything like before…” – Zerohedge

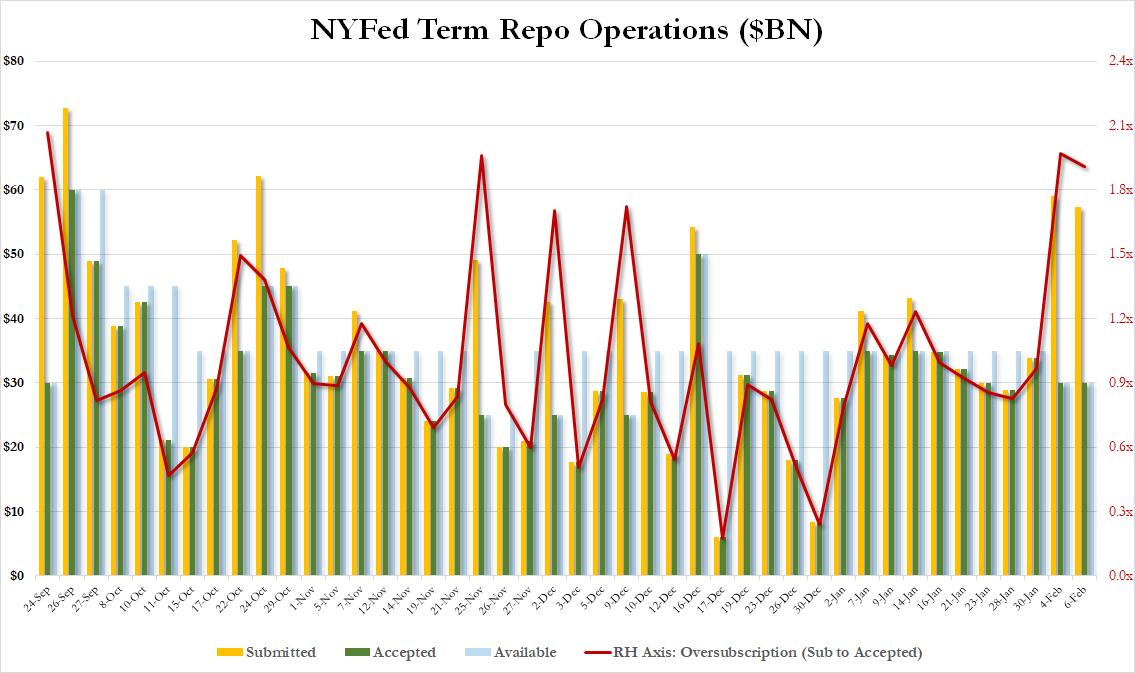

But, as I stated, it wasn’t just the PBOC, but also the Federal Reserve dumping tremendous amounts of liquidity into the markets which only had one place to go….equities.

While the Fed continues to deny current liquidity interventions are indeed “QE,” they have been clearly concerned about the potential of global instability impacting the U.S. In their most recent report to Congress, the “coronavirus” made its appearance as the latest threat to the global economic instability.

Do NOT dismiss that last sentence lightly.

Since last October, the Fed has been injecting the financial system with massive quantities of liquidity to fix “short-term funding needs.” Each time they have tried to slow the rates of funding, the market has declined, so they extended the facility. Initially, the facility was for October tax payments. Then it was extended for the “year-end” turn. Then it was extended for April “tax payments.” The “coronavirus” will be the next reason to extend the program into June.

Just in case you missed our previous report on this issue, the importance is that this type of funding has not occurred to such a magnitude outside of a financial crisis.

The question you should be asking is: “exactly what is going on?”