Written by Lance Roberts, Clarity Financial

As noted above, after previously reducing exposure “slightly” to equities, we are now starting to actively scan for opportunities for a “risk rotation” in the market.

Please share this article – Go to very top of page, right hand side, for social media buttons.

For quite some time, we have been portfolio weight to overweight in defensive areas of the market like Utilities, Real Estate and Staples as well as Treasury bonds. Those areas are now extremely extended. We will look to take profits out of these sectors and rebalance weights in Technology, Financials, Healthcare, and Communications, which we reduced previously.

This rebalancing of risk will not dramatically increase our equity exposure; as noted above, the longer-term technical outlook remains cautious. We are very late-cycle in the current market, but with the Fed still intervening, we must give deference to the “bullish bias,” which remains at the moment. In other words, it is not time to be “bearish” yet, but “cautious” is likely a better attitude to have.

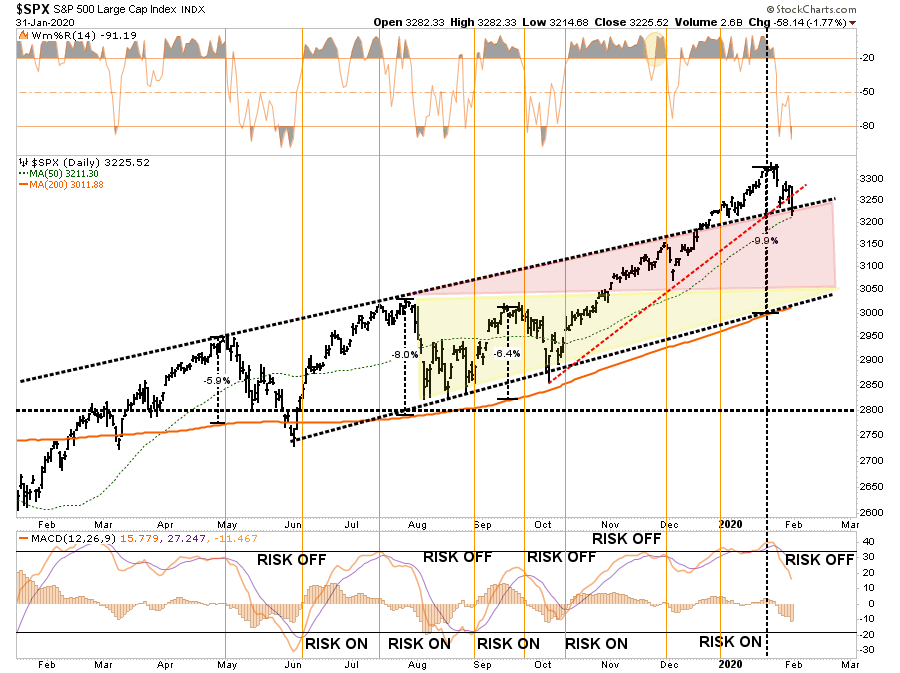

With bond yields plummeting this past week, our bond exposures have gotten extremely stretched. The sell-off in the market, combined with the “risk off” rotation to bonds, sets the market up for a reflexive bounce. The duration and magnitude of that bounce will be critical as to our next steps in positioning.

A reflexive bounce that fails at the bottom of the trendline from the October lows (red dashed line) will be fairly negative, and suggest lower lows are coming. With February typically a “weak month” anyway, there is a high likelihood of this event occurring, especially if the virus is not contained soon.

If the bounce holds the 50-dma, and reclaims the bullish trendline, then a run back towards the previous highs is likely. This is will likely coincide with a containment of the virus, or help from the Fed in terms of “guidance” combined with an extension of “Repo” funding past April.

Our reduced positioning has helped shelter our portfolios this month, as portfolio drag was about 1/3rd of the overall market. We can now use our stored cash to take advantage of some trading opportunities that have presented themselves.

The “bullish bias” is not dead as of yet, and investors will be quick to try and “write off” the impact of the “virus.” After a decade of “macro-events” not stopping the bullish charge, the belief the market is “bulletproof” has become so deeply ingrained into investor mentality it won’t be dislodged until it is far too late to matter.

Is this “the” event that triggers the next “bear market” and “recession?”

Maybe. Maybe not.

We won’t know for sure until after the fact. But this is why we manage risk in the short-term, so that we can navigate the “twists and turns” of the market without careening off the cliff.