Written by Lance Roberts, Clarity Financial

As noted last week, in July of 2019, we laid out our prognostication the S&P 500 could reach 3300 amid a market melt-up though the end of the year. On Friday, the S&P 500 closed at 3329, with the Dow pushing toward 29,350.

Please share this article – Go to very top of page, right hand side, for social media buttons.

With the Federal Reserve continuing to pump liquidity into the market currently, we are raising our 2020 estimate for the S&P to 3500 as “the mania” goes mainstream. There is absolutely NO FUNDAMENTAL basis for raising the target; it is ONLY a function of the momentum chase.

This urgency to take on “risk,” as investors pile into “passive indexes” under a “no market risk” assumption, can be seen in the extreme lows of the put/call ratio.

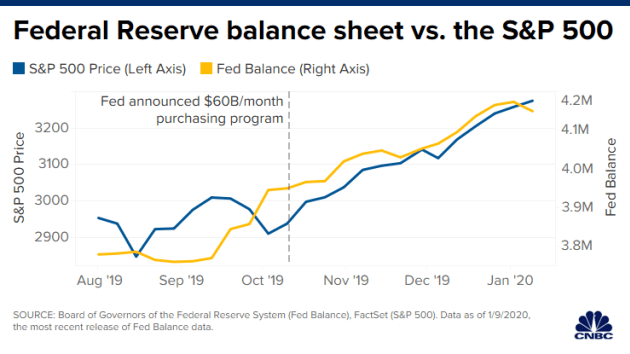

With the Federal Reserve’s ongoing “Not QE,” it is entirely possible the markets could continue their upward momentum towards S&P 3500, and Dow 30,000. Clearly, the “cat is out of the bag” if CNBC even realizes it’s the Fed:

“On Oct. 11, the central bank announced it would begin purchasing $60 billion of Treasury bills a month to keep control over short-term rates. The magnitude of the purchases resembles the quantitative easing program the Fed conducted during and after the financial crisis.”

“The increase in the Fed’s balance sheet has been in near lockstep with the stock market’s climb. The balance sheet has expanded 10% since October, while the S&P 500 shot up 12%, including notching its best fourth quarter since 2013.”

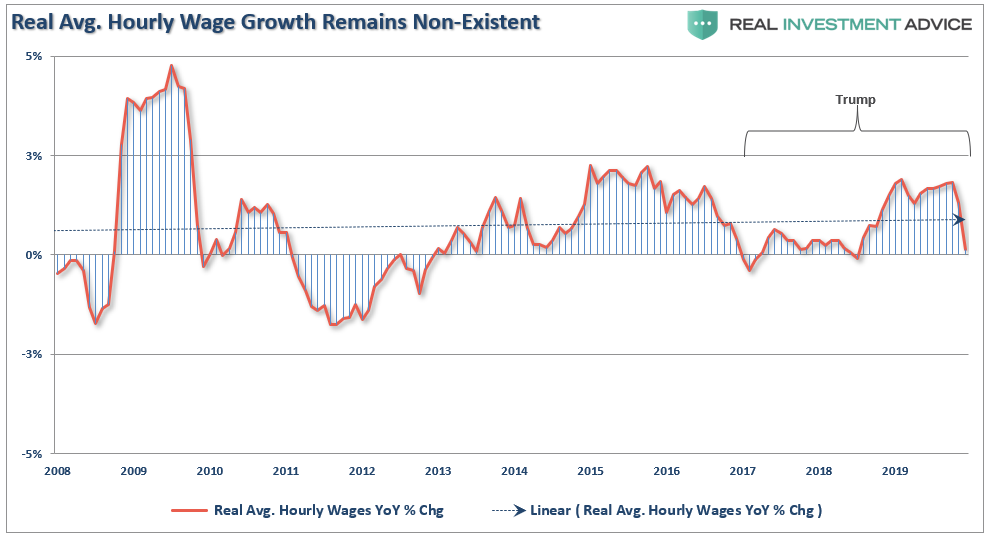

With the Federal Reserve continuing to “ease” financial conditions, there is little to derail higher asset prices in the short-term. However, we continue to see cracks in the “economic armor,” like Friday’s plunge in “job openings,” continued deterioration in earnings estimates, weaker growth rates in employment, and negative revisions to data, like wages, which suggest the market is well ahead of the economy. (Last week, negative revisions wiped out all the wage growth for the bottom 80% of workers.)

But, as I said, “fundamentals” don’t matter currently. As CNBC noted:

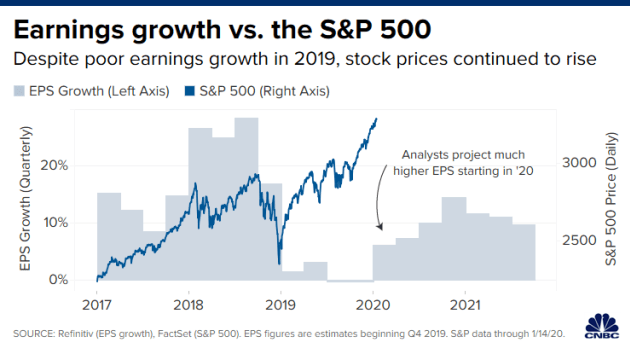

“The problem front and center is how investors are looking past the continuous earnings rout, betting on a snapback as soon as the first quarter of 2020. S&P 500 earnings are expected to drop by 0.3% in the fourth quarter of 2019, marking the first back-to-back quarterly decline since 2016, according to Refinitiv.”

While “fundamentals” may not seem to matter much currently, eventually, they will.