Written by Lance Roberts, Clarity Financial

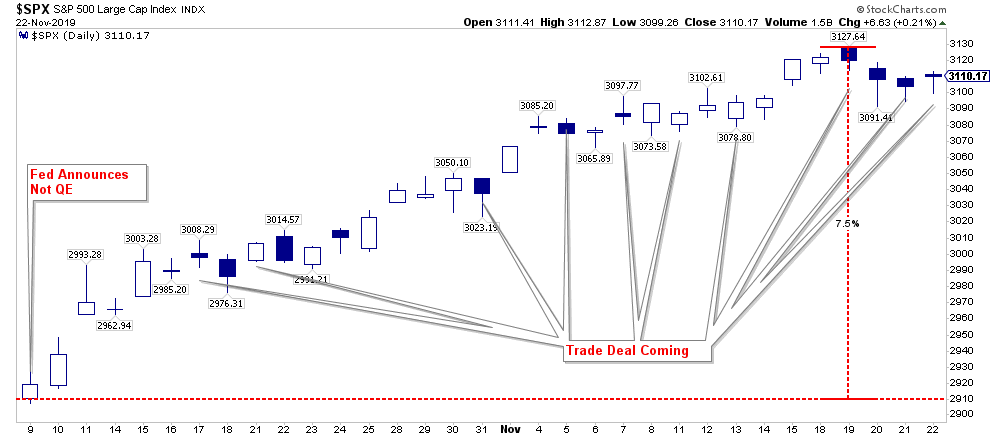

Over the last few weeks, we have been discussing the “QE, Not QE” rally. Regardless of what the Fed wishes to call their bond purchases, the market has interpreted the expansion of their balance sheet as a “QE” program. Given that investors have been “trained” by the Fed’s “ringing of the bell,” the subsequent 6-week advance was not surprising.

Please share this article – Go to very top of page, right hand side, for social media buttons.

(I might have missed a couple of “trade deal” headlines but you get the drift.)

The important part of our discussion over the last several weeks has been twofold:

- What are the expected returns from various asset classes during a QE program, and;

- Hedging for a short-term correction given the rather extreme overbought condition that occurred.

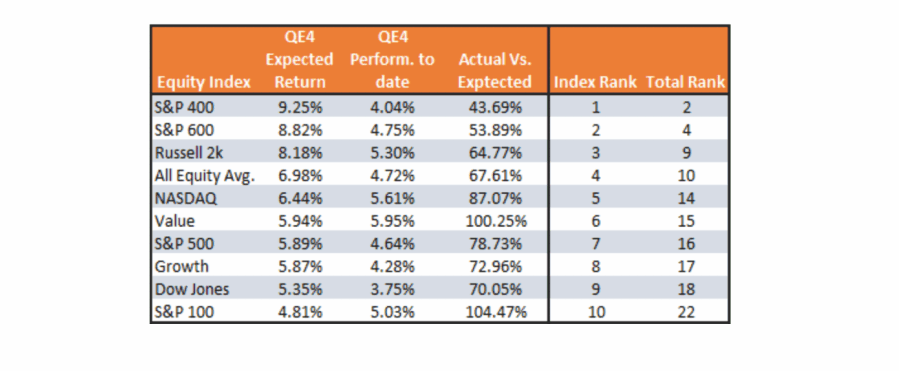

This week, we updated our previous analysis for our RIAPro Subscribers (30-Day Free Trial) on historical QE programs to review how far each of these markets and sectors have responded so far. The results were quite surprising. (If you subscribe for a 30-day Free Trial you can read the entire report ‘An Investor’s Guide To QE-4 The Update’)”

“The bottom line is that the Fed has taken massive steps over the last few months to provide liquidity to the financial markets. As we saw in prior QEs, this liquidity distorts financial markets. The following table provides the original return projections by asset class as well as performance returns since October 14th. The rankings are based on projected performance by asset class and total.”

(Get the FREE trial to see the full table of all markets, sectors, and commodities.)

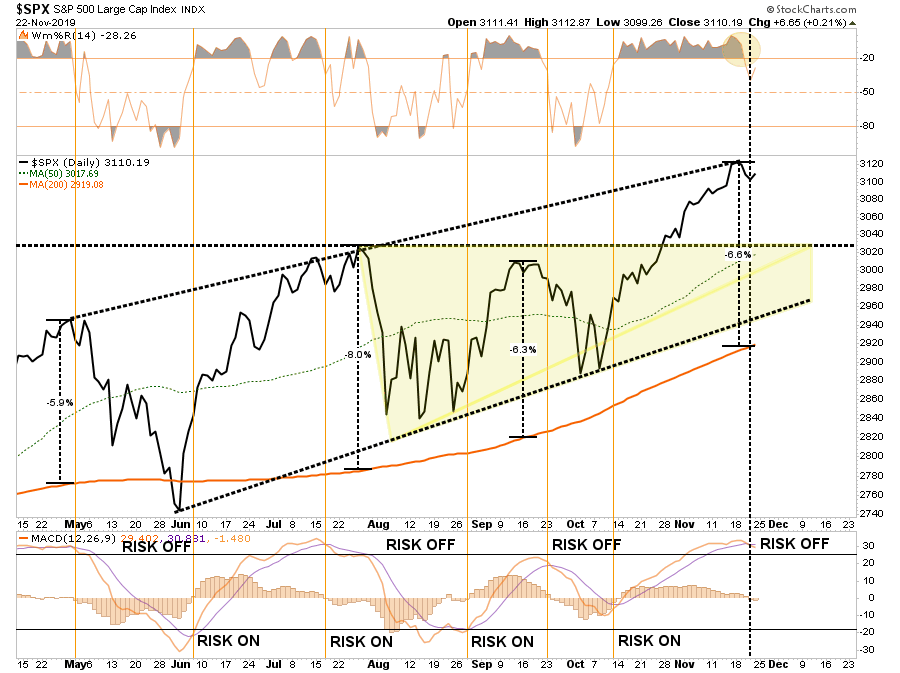

With QE-4 in play, the bias remains to the upside keeping our target of 3300 on the S&P 500 in place. This is particularly the case as we head further into the seasonally strong period combined with an election year cycle.

As shown in the chart below, the breakout to all-time highs was substantial, and regardless of your bias, this was a “bullish” advance and suggests higher prices in the short-term.

However, nothing travels in a straight line, and given the exceedingly overbought condition which currently exists, as we discussed previously, is why we hedged our portfolios. To wit:

“With the Fed engaged in pumping liquidity into the markets, and any day may also include a random market manipulation from a ‘Trump tweet,’ the most opportunistic method to hedge risk is to add a ‘short S&P 500’ index position to the portfolio.”

We currently still maintain our hedge at the moment.

Our short-term concern remains Trump’s “trade deal” dealings. The Chinese are stringing him along, now with calls for more meetings, even as he signs a bill which will directly infuriate the Chinese Government over their dealings with Hong Kong.

As I stated many times in this weekly missive, the Chinese are under NO pressure to “do any deal” with Trump which is not beneficial to their long-term economic goals.

“China is out for “China’s” best interest and will not acquiesce to any deal which derails their long-term plans. In the short-term, they may ‘play the game’ to get what they need as a country, but in the long-run, they will protect their own interests.

The pressure is on the Trump Administration to conclude a ‘deal,’ not China. Trump needs a deal done before the 2020 election cycle; AND he needs the markets and economy to be strong. If the markets and economy weaken because of tariffs, which are a tax on domestic consumers and corporate profits, as they did in 2018, the risk of electoral losses rise.”

There is a lot of room for disappointment over “trade” with respect to the markets.

- Trump continues to delay

- The Chinese “push back” over Hong Kong, or

- Trump reignites, or just fails to delay, tariffs.

The market will likely not respond kindly to any of these disappointments as invetors have already priced in the most optimistic of outcomes.

Holiday Publication Note

All of us at RIA Advisors, and Real Investment Advice, want to wish you, and your family, a very happy, healthy, and filling Thanksgiving Holiday. (Okay, skip the “healthy” part because I am all about “the pie” in every flavor.)

Next week, unless something significant happens, we will likely not publish a weekly report. However, not to worry, we will resume our regular publication schedule beginning December 2nd.

In the meantime, should you have any questions, comments, or concerns please do not hesitate to email me.

Happy Thanksgiving

.

include(“/home/aleta/public_html/files/ad_openx.htm”); ?>