Written by Lance Roberts, Clarity Financial

Michael Lebowitz, CFA recently penned:

“A Honus Wagner baseball card from 1909 was recently auctioned for over $3 million. While that may seem like a lot of money, it is not necessarily expensive. A baseball card is nothing more than paper and ink with no real value. Its street value, or price, is based on the whims of collectors. “Whim” is impossible to value.

Please share this article – Go to very top of page, right hand side, for social media buttons.

Stocks are not baseball cards. Stocks represent ownership in a corporation, and therefore, their share prices are based on a future series of expected earnings and cash flows. Further, there are many other types of investments that serve not only as alternatives, but provide a means to assess relative value.

Today, investors are trading stocks on a “whim,” with scant attention to their value. Unlike a baseball card, when a stock’s street value rises much more than its real value, an inevitable correction will occur. The only question is not if but when will investors realize what they are truly buying.”

There is an important distinction to be made here between “investing” vs. “speculating.”

Benjamin Graham, in his seminal work Security Analysis (1934) defined investing as:

“An operation in which, upon thorough analysis, promises safety of principal and a satisfactory return. Operations not meeting these requirements are speculative.”

The problem is that today, the term “investor” is now being applied ubiquitously to anyone who participates in the stock market. As Graham noted later in “The Intelligent Investor:”

“The newspaper employed the word ‘investor’ in these instances because, in the easy language of Wall Street, everyone who buys or sells a security has become an investor, regardless of what he buys, or for what purpose, or at what price, or whether for cash or on margin.”

To understand “what happens next,” one must understand the difference between “investment” and “speculation.”

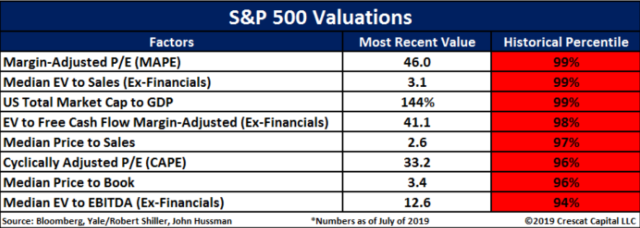

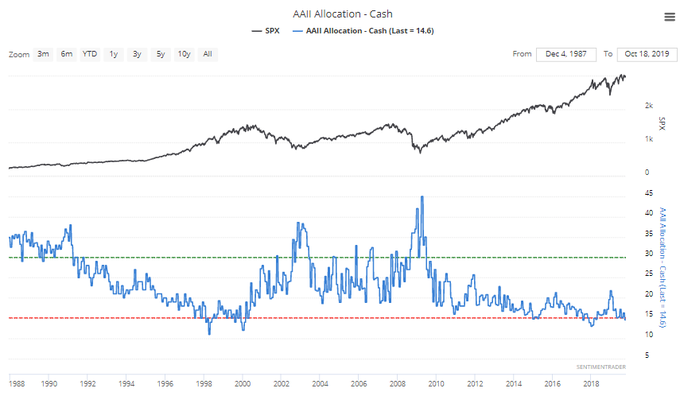

While QE-4 may be driving stocks higher today based on a “whim,” there are two very important difference between QE-4 and QE-1 or 2; 1) stocks are no longer undervalued or 2) under-owned.

“With cash levels at the lowest level since 1997, and equity allocations near the highest levels since 1999 and 2007, it suggests investors are now functionally ‘all in.’”

With investors paying exceptionally high prices for equity ownership, expected forward returns becomes much more problematic. As we addressed last Thursday:

“The detachment of the stock market from underlying profitability guarantees poor future outcomes for investors. But, as has always been the case, the markets can certainly seem to ‘remain irrational longer than logic would predict,’ but it never lasts indefinitely.

‘Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system, and it is not functioning properly.’” – Jeremy Grantham

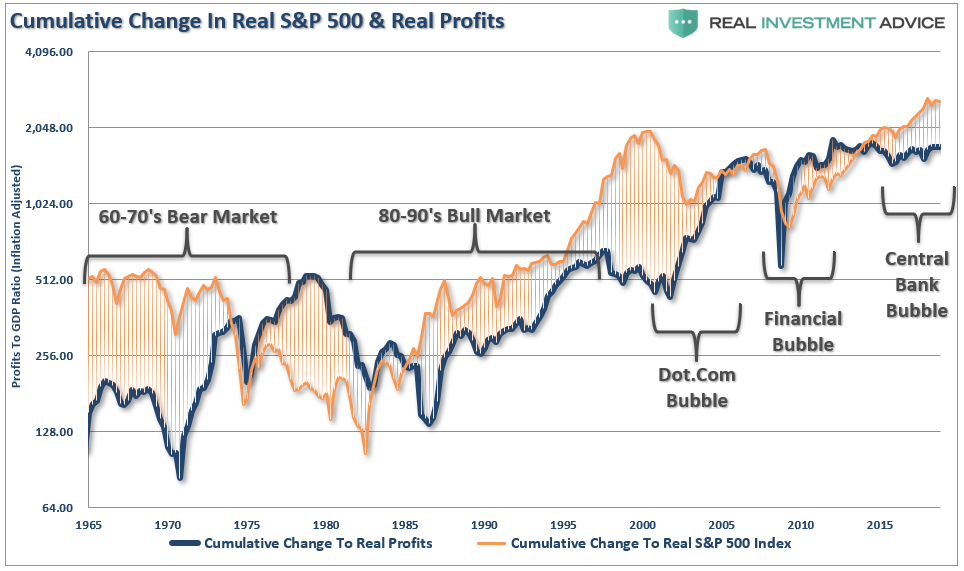

Another way to look at the issue of profits as it relates to the market is shown below. When we measure the cumulative change in the S&P 500 index as compared to the level of profits, we find again that when investors pay more than $1 for a $1 worth of profits there is an eventual mean reversion.

With investors paying more today than at any point in history for each $1 of profit, the next mean reversion will be a humbling event.

That is just math.

However, in the meantime, individuals are “speculating” within the markets based solely on the premise that a “greater fool” will be there when the time comes to sell.

Unfortunately, that is rarely the case.

There are virtually no measures of valuation which suggest making investments today, and holding them for the next 20-30 years, will work to any great degree.

This is the difference between “investing” and “speculation.”

When you think about QE-4, as it relates to your portfolio, you have to consider the premise of valuations, margin of safety, and risk. Yes, the markets are indeed bullish by all measures, and holding risk will likely pay off in the short-term. (speculation) However, over the long-term, the “house will always win.” (investing)

If you need help or have questions, we are always glad to help. Just email me.

See you next week.

.