Written by Lance Roberts, Clarity Financial

“If you are a bull, what is there not to love?”

That was the message from two weeks ago, and the reasoning behind increasing our equity exposure in portfolios as we head into the end of the year.

Please share this article – Go to very top of page, right hand side, for social media buttons.

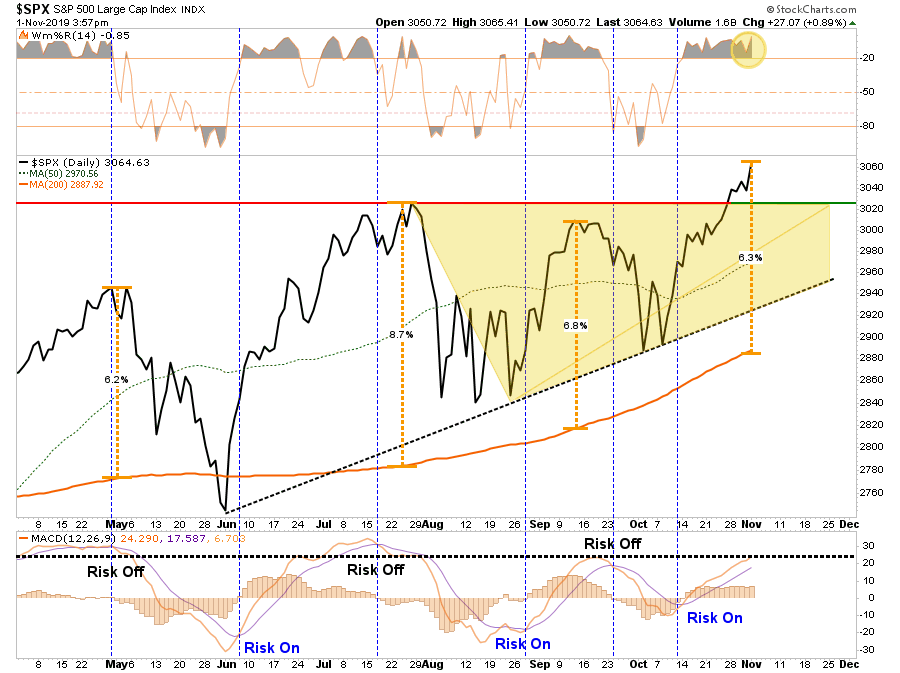

With the Fed cutting rates on Wednesday, and companies winning the “beat the estimate game” as earnings season progresses, the markets finally broke out to new “all-time” highs this past week.

This breakout is consistent with the “revival of the bulls” which is needed as there is too much attention focused on a “recession” and “bear market.” (If a recession/bear market would have occurred it would have been the first time in history “everyone” saw it coming.)

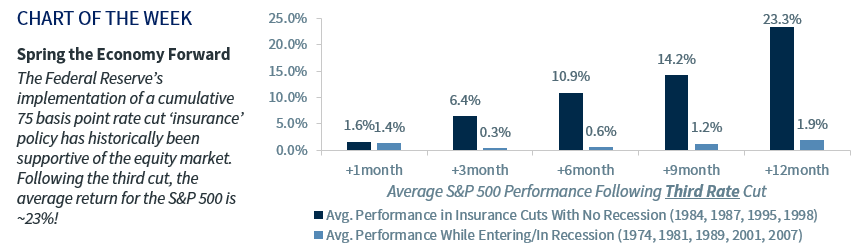

“Over the last 30 years, when the Fed has implemented an ‘insurance’ rate cut policy of 75 basis points, the equity market has been ‘lights out’ as the S&P 500 has posted a 12-month forward return of ~23%, on average.” – Raymond James

(H/T G. O’brien)

That’s the good news.

However, before you go jumping in with both feet, there are a couple of points to be made.

Concerning the chart above, you have to decide whether the recent rate cuts by the Fed are “mid-cycle adjustments” or “cuts entering a recession.” While most people only notice the tall black bars, given we are in the longest economic expansion in history, the short-blue bars may be important.

Again, since bear markets/recessions NEVER occur when everyone is expecting them, the breakout to new highs is exactly what is needed to “suck investors” back into the market at the potential peak. This is how bear markets have always begun in history.

On a shorter-term basis, whether you are bullish or bearish, the market is now more than 6% above its 200-dma. These more extreme price extensions tend to denote short-term tops to the market, and waiting for a pull-back to add exposures has been prudent.

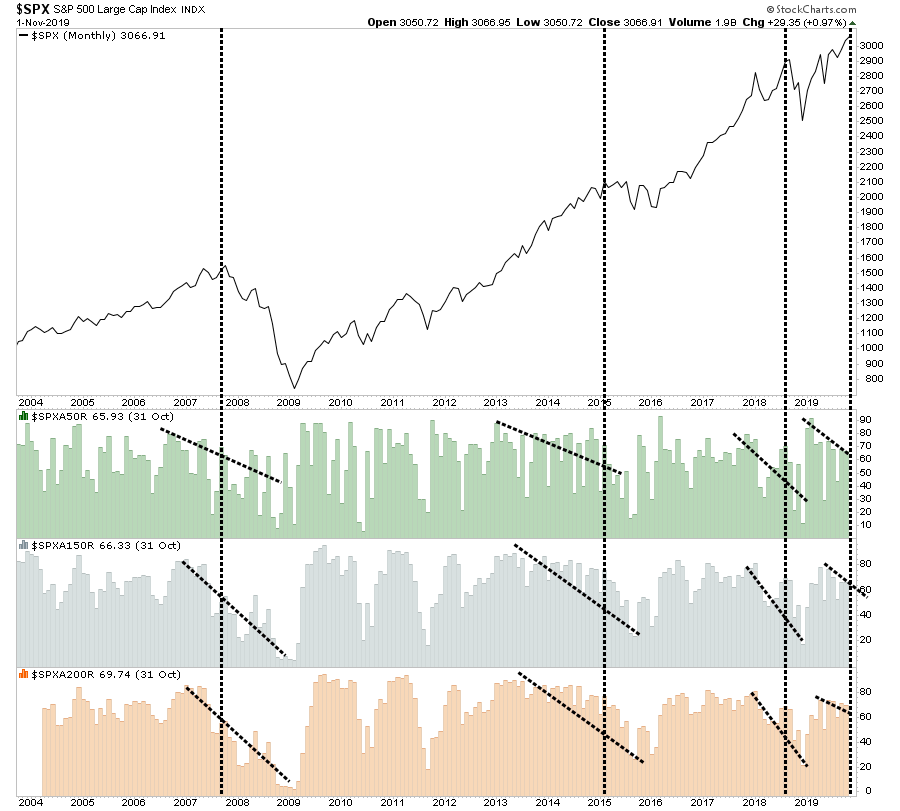

The other concern is the weakness in overall participation in the market. Despite the markets pushing to all-time highs, the number of stocks trading above their respective 50, 150, and 200-dma’s remain in downtrends. These negative divergences have preceded short to intermediate-term corrections in the past.

How To Play It

As we have been noting over the last month, with the Fed’s more accommodative positioning, we continue to maintain a long-equity bias in our portfolios currently. We have reduced our hedges, along with some of our more defensive positioning. We are also adding opportunistically, to our equity allocations, even as we carry a slightly higher than normal level of cash along with our fixed income positioning.

We also realize that “all good things do come to an end.” While we are currently “riding the bull,” we are simply waiting for the “8-second buzzer” to prepare for our dismount. (That’s a Texas rodeo thing if you don’t know the reference.)

Therefore, make sure you have stop-losses in place on all positions and be prepared to execute accordingly. The worst thing investors consistently do over time is to turn a “winner” into a “loser” before they eventually sell. (And they always sell.)

While you will certainly reduce your tax liability with this method, it is not a strategy by which you will increase your wealth. Being “rich on paper” and having “cash in the bank” are two ENTIRELY different things.

.