Written by Lance Roberts, Clarity Financial

Every morning, at RIAPro.net, we post commentary as to what is moving the markets. On Thursday we pointed out a dynamic in the funding of the U.S. Treasury that few are following despite the implications it has on monetary policy.

Please share this article – Go to very top of page, right hand side, for social media buttons.

On Thursday, we posted the following:

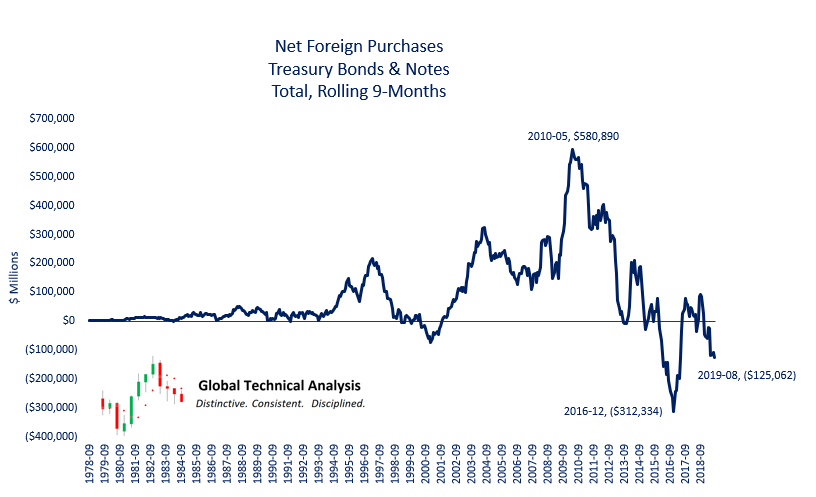

“Today’s Chart of the Day is probably one of the most important macro charts to understand, yet is so underappreciated. The chart highlights that net purchases of U.S. Treasury debt by foreign investors (central banks, governments, corporations, and citizens) have been negative over the last two years. This is occurring as deficits topple the $1 trillion mark. In other words, not only are trillion dollar deficits being entirely funded with domestic funds, but domestic funds must also absorb the foreign net selling. To better understand the implications of this new dynamic, we suggest reading an article we wrote in June titled Who is Funding Uncle Sam?“

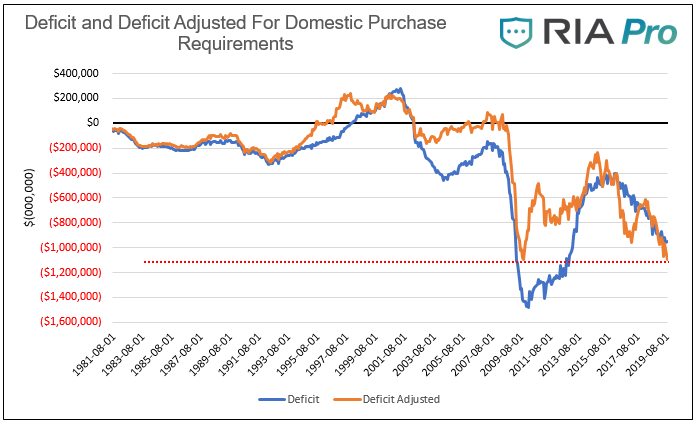

The problem is something we have discussed previously, which is a “dollar funding shortage.” In other words, the Treasury needs to sell bonds to cover deficit spending. If there is a “shortage” of buyers, then the Treasury can’t “raise the money” it needs to meet spending demands.

Hence the need for the Fed to step into to monetize existing debt so domestic issuers can take up new issues. We believe the funding situation is one causes of the overnight funding issues, and the sudden introduction of QE. As shown, despite deficits not being as large as in the last recession, the amount of domestic funds required to fund the Treasury deficit is now larger.

Regardless of the reason, the Fed is injecting liquidity into the market at the highest pace since the Financial Crisis.

This certainly doesn’t suggest that “All is well in Denmark.”

So, how do we “play it?”

Playing QE4

Tuesday’s article, “It’s Crazy, But We Are Adding Equity Risk,” was based on research we did for our portfolio allocation models.

“While it may seem ‘crazy,’ it is for these reasons, despite the longer-term bearish backdrop, that we need to ‘gradually’ and ‘incrementally’ increase exposure for the next couple of months. Importantly, I did not say leverage up and buy speculative investments. I am suggesting a slight increase in exposure toward equity risk, as opportunity presents itself, until we have an allocation model that both hedges longer-term risks, but can take advantage of shorter-term bullish cycles.”

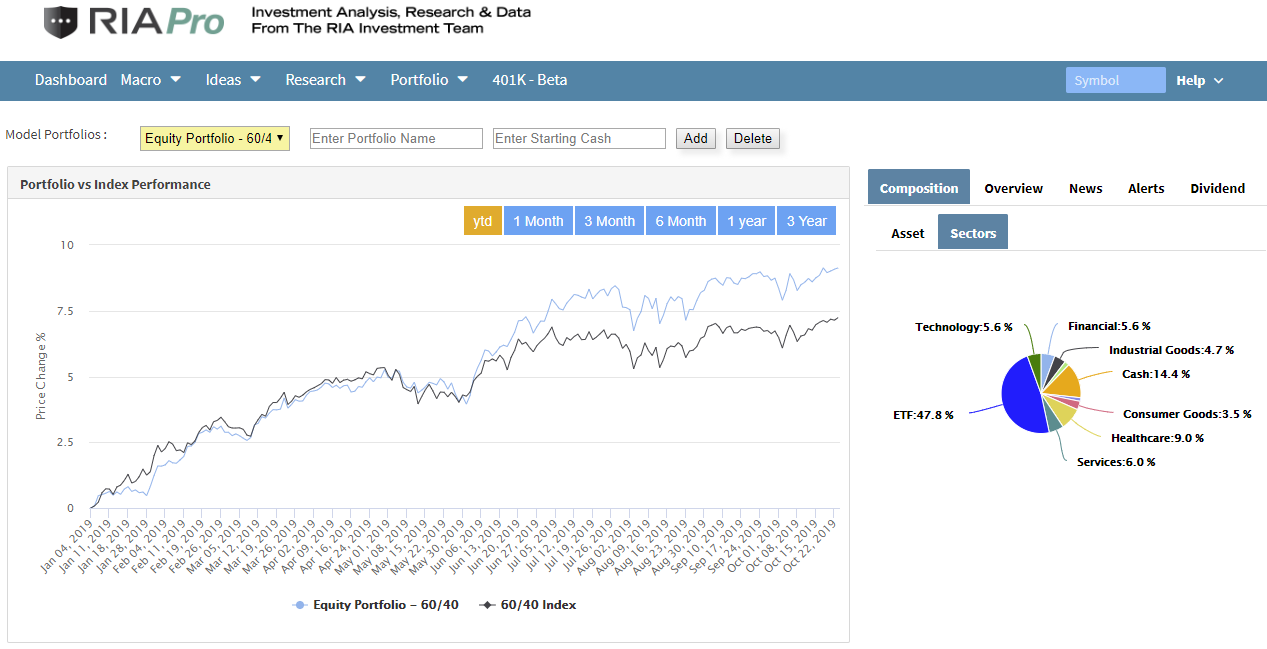

That research was just published for our RIAPro subscribers (Click here for a 30-day FREE Trial to read the entire report) which revealed the performance of equities, commodities, and bonds during periods of QE.

Here is an excerpt:

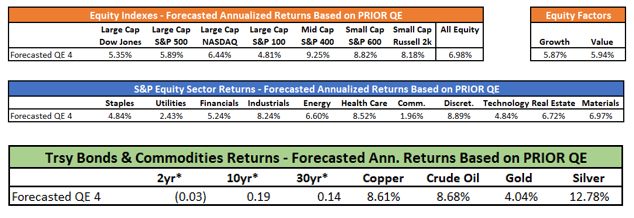

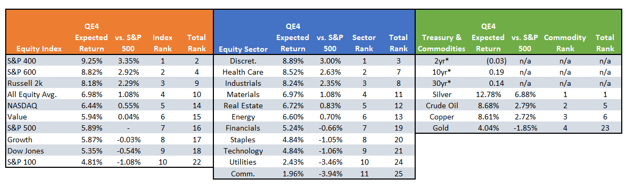

“If we assume that assets will perform similarly under QE 4, we can easily forecast returns using the normalized data from above. The following three tables show these forecasts. Below the tables are rankings by asset class as well as in aggregate. For purposes of this exercise, we assume, based on the Fed’s guidance, that they will purchase $60 billion a month for six months ($360 billion) of U.S. Treasury Bills.”

Not surprisingly, during periods of QE we find that:

- Markets exhibit higher volatility.

- Defensive positioning underperforms relative to the S&P 500.

- Growth stocks outperform (on a relative basis.)

- Longer-term bond yields rise while shorter-term yields were flat, resulting in steeper yield curves in all three instances.

- Copper, crude oil, and silver outperformed the S&P 500.

This data supports our recent changes in positioning where we have taken profits in our defensive positions like utilities and staples, and are increasing exposure to cyclical and growth sectors.

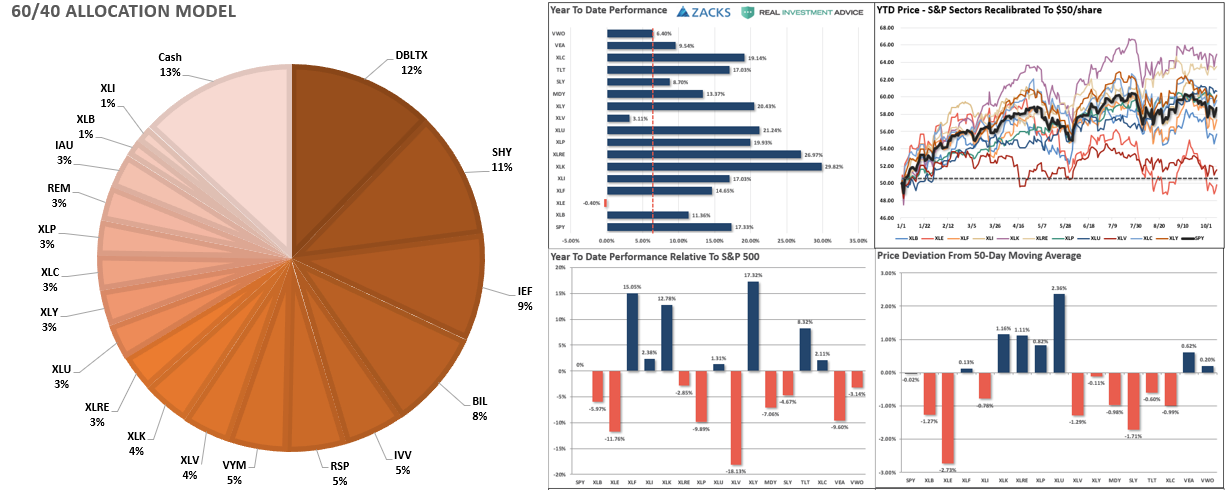

“This is why we continue to maintain a long-equity bias in our portfolios currently. We also recently slightly reduced our hedges, along with some of our more defensive positioning. We are still maintaining slightly higher than normal levels of cash.”

In our equity portfolio we have also added positions to take advantage of the steeper yield curve, while shortening duration and increasing credit quality in our bond portfolios to hedge against higher rates.

(Our portfolios are displayed “real time” at RIAPro.)

While we believe that QE4 will likely provide some upside bias (Our target expectation is 3300) there are significant differences between QE4 and QE1, namely the entire economic and financial backdrop are entirely reversed.

“The critical point is that QE and rate reductions have the MOST effect when the economy, markets, and investors have been ‘blown out,’ deviations from the ‘norm’ are negatively extended, confidence is hugely negative. In other words, there is nowhere to go but up.

The extremely negative environment that existed in 2009, particularly in the asset markets, provided a fertile starting point for monetary interventions. Today, the economic and fundamental backdrop could not be more diametrically opposed.”

While another $2-4 Trillion in QE might indeed be successful in further inflating the third bubble in asset prices since the turn of the century, there is a finite ability to continue to pull forward future consumption to stimulate economic activity. In other words, there are only so many autos, houses, etc., which can be purchased within a given cycle. There is evidence the cycle peak has been reached.

If we are correct, and the effectiveness of rate reductions and QE are more diminished that many expect. There is a limit to just how many bonds the Federal Reserve can buy, and a deep recession will likely find the Fed powerless to offset much of the negative effects.

If more “QE” works, great. We are positioning for it.

But, as portfolio managers taking care of our clients retirement savings, we are maintaining hedges and plenty of “risk controls” just in case things don’t work out as planned.

What are you doing with your money?

If you need help or have questions, we are always glad to help. Just email me.

See you next week.