Written by Lance Roberts, Clarity Financial

On Thursday, the Fed announced that they will nearly double the daily repo liquidity operations to $120 billion, as well they said the sizing of the 14-day term repo programs would rise from $30 billion to $45 billion. For the most part these daily and term repo operations have been oversubscribed, meaning there is more demand than liquidity being offered by the Fed. This growing problem is a reason for the recent announcement of QE (not QE).

Please share this article – Go to very top of page, right hand side, for social media buttons.

(For more on “Repo” read this.)

As noted by Zerohedge on Thursday morning:

“In a statement published at 1515ET, precisely when the S&P ramp started (on Wednesday), the New York Fed confirmed it would dramatically increase both its overnight and term liquidity provisions beginning tomorrow through November 14th.

‘The Desk has released an update to the schedule of repurchase agreement (repo) operations for the current monthly period. Consistent with the most recent FOMC directive, to ensure that the supply of reserves remains ample even during periods of sharp increases in non-reserve liabilities, and to mitigate the risk of money market pressures that could adversely affect policy implementation'”

This is a massive 60% increase in the overnight repo liquidity availability (from $75 billion to $120 billion) and a 28% jump in the term repo provision (from $35 billion to $45 billion).

The Fed continues to insist this is not “Quantitative Easing,” and this is simply short-term funding for short-term cash needs (the original excuse were corporate tax payments which have long since passed.)

However, as we addressed just recently, we suspect it is something significantly different when you consider the most recent Term Repo operation was 1.38x oversubscribed.

“This was not about covering unexpected cash draws to pay quarterly taxes, which was one of the initial excuses for the funding shortfalls.”

Nope.

This was bailing out a bank that is in serious financial trouble. It started with the ECB a month ago loosening requirements on banks, then proceeded to the Fed reducing capital reserve requirements and flooding the system with reserves.

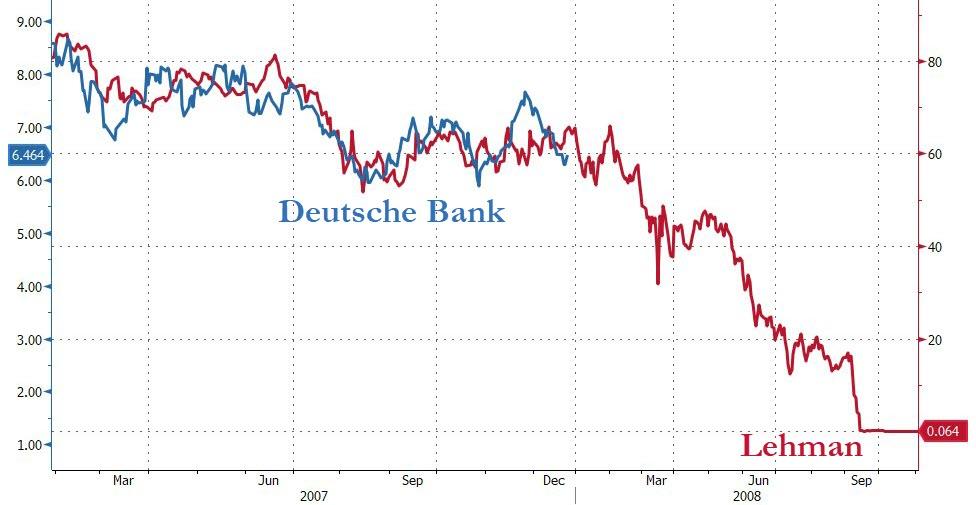

Who was the biggest beneficiary of all of these actions? Deutsche Bank.

Deutsche is about 4x as large as Lehman was in 2008 and is currently following the same price path as well. Let me repeat, the Fed is terrified of another “Lehman Crisis” as they do not have the tools to deal with it this time.

(Courtesy of ZeroHedge)

Clearly, the Fed is concerned about something other than the impact of “Trump’s Trade War” on the economy.

As noted by Zerohedge:

“Needless to say, if the funding shortage was getting better, none of this would be happening; instead it appears that with every passing day the liquidity shortage is getting worse, even as the Fed’s balance sheet is surging.

The only possible explanation, is someone really needed to lock in cash for month end (the maturity of the op is on Nov 7) which is when a ‘No Deal’ Brexit may go live, and as a result one or more banks are bracing for the worst.

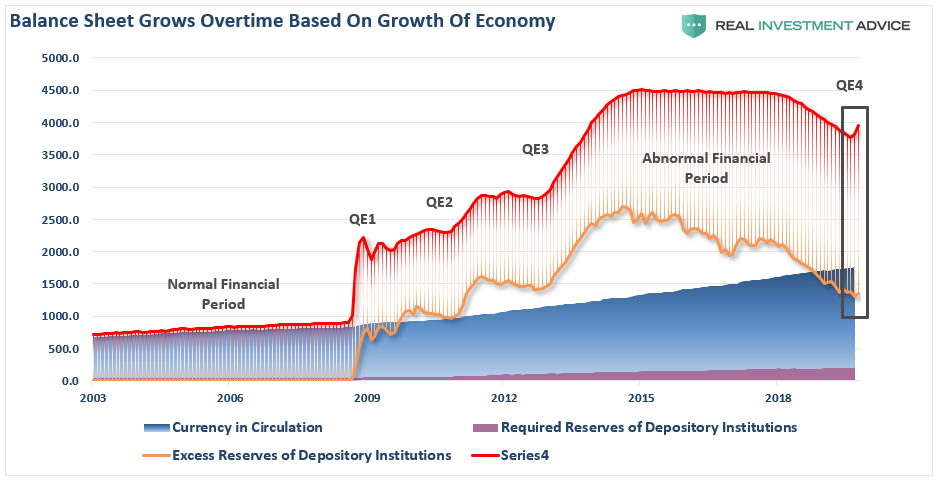

The question, as before, remains why? Just what is the source of this unprecedented spike in liquidity needs in a system which already has $1.5 trillion in excess reserves?”

That is the correct question.

But in the meantime, the injection of liquidity continues to support asset prices as the litany of “algo’s” which drive -80% of the trading on Wall Street, respond in “Pavlovian” fashion to more liquidity.

.