Written by Lance Roberts, Clarity Financial

As I noted last week in “Pavlov’s Dogs & The Ringing Of The Bell:”

“The ‘ringing of the bell’ over the last decade has trained investors to rush into equity-related risk.”

Please share this article – Go to very top of page, right hand side, for social media buttons.

With Powell disappointing traders, and Trump retaliating with additional tariffs, the initial response was to flee to “safety,” or rather should I say ” bonds.”

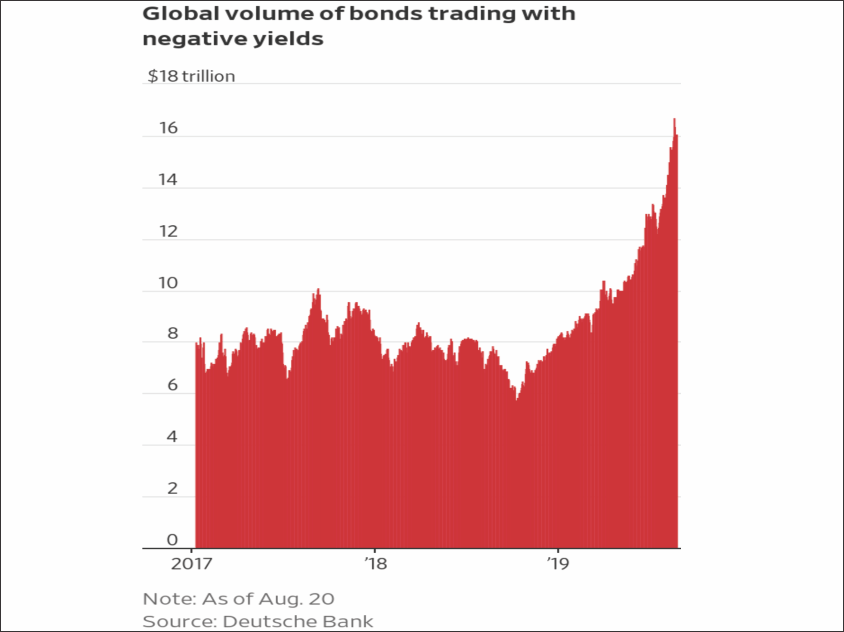

While retail investors continue to cling onto stocks hoping for a resurgence of the “bull market,” institutions are piling into bonds as the tidal wave of data continues to warn something is “broken.”

(You don’t have $17 Trillion in negative-yielding sovereign debt if there is economic and fiscal stability.)

Doug Kass reminded me on Thursday of a memorable lesson from “Wall Street.”

“Quick buck artists come and go with every bull market, but the steady players make it through the Bear Markets. Enjoy it while it lasts – ’cause it never does.'” – Lou Mannheim

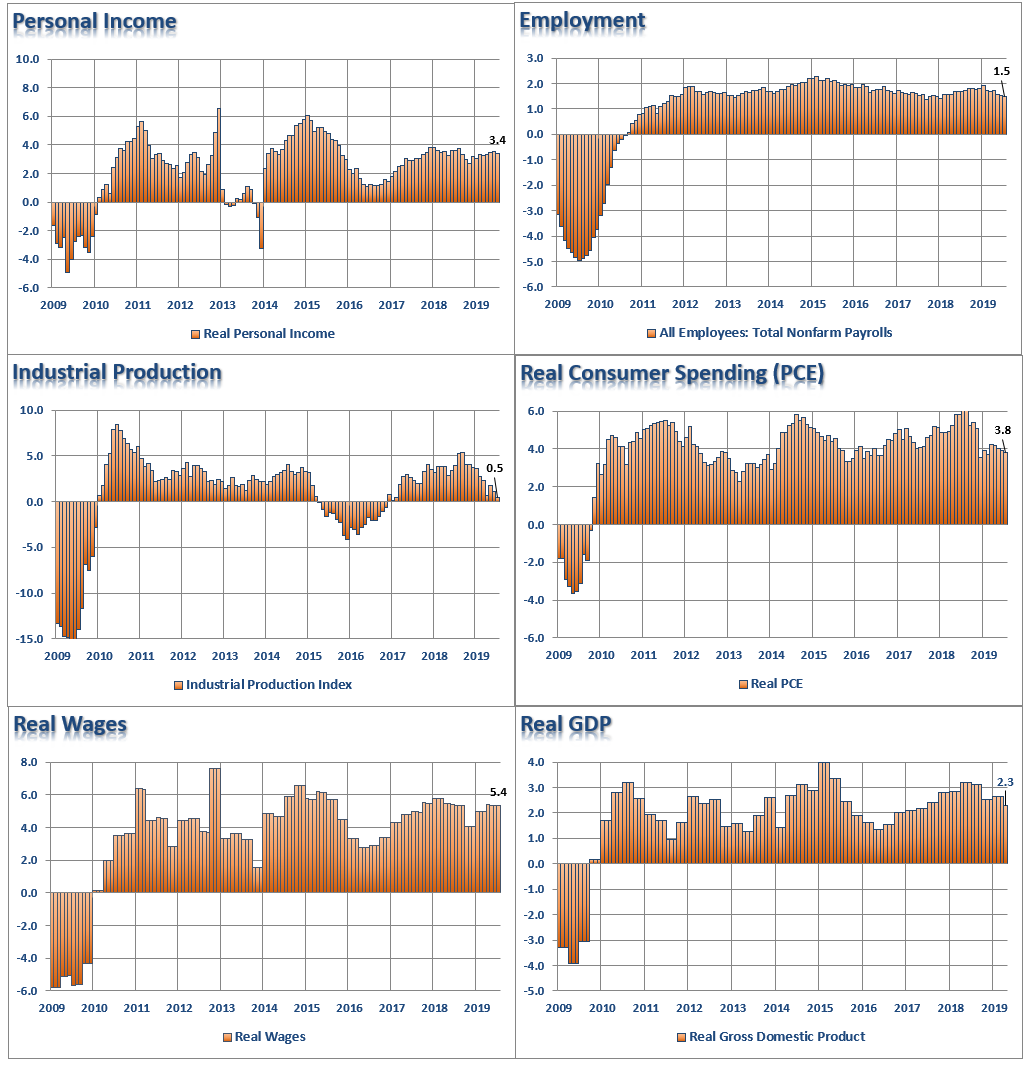

The message that negative yields are sending coincides with weaker growth rates in:

- Corporate profits

- Employment

- CapEx

- Personal Consumption Expenditures

- Real Retail Sales

- GDP

You can see this visually in the 6-panel chart from last week’s missive

Yes, the data is not negative which is why we aren’t in a recession…yet, (However, the data is subject to substantial negative revisions, and as we showed last week, the month before the last recession started all the data was positive as well.)

This is also the reason the Fed stopped hiking rates.

Last September, the Fed believed they needed to hike rates more aggressively as they believed the “neutral rate,” (code for economic growth) was considerably higher. We warned then several natural disasters were skewing the economic data, and that hiking rates was a mistake. By December, as rates reached 2%, and with the markets down 20%, the “neutral rate” had been achieved.

Don’t mistake the following comment from Fed member Patrick Harker earlier this week:

“This was a situation where we were getting back to what I would see as a neutral rate. In December 2018, we raised rates by 25 basis points. At that time, I was not supportive of that move because I thought that we didn’t need to do that. So, we’re just recalibrating back to where I thought we should have been, with a 25-basis-point cut.”

Since that is a lot of “Fed speak,” let me translate:

“Listen, as a member of the Fed, I can’t tell you the economy has weakened significantly, and the threat of a recession has risen markedly. If I did say that, the market would crash, consumer confidence would crash, and we would immediately be in a recession.

The reality is that we needed to get rates off of zero percent, and we were hoping to get rates closer to 4%, to give us some room to support the economy during the next recession.Unfortunately, we actually ‘over tightened’ which led to the market disruption last year. The rate cut in July was to be supportive of the economy short-term, but we need to hold as much ‘ammo’ as possible in reserve for when the recession hits.”

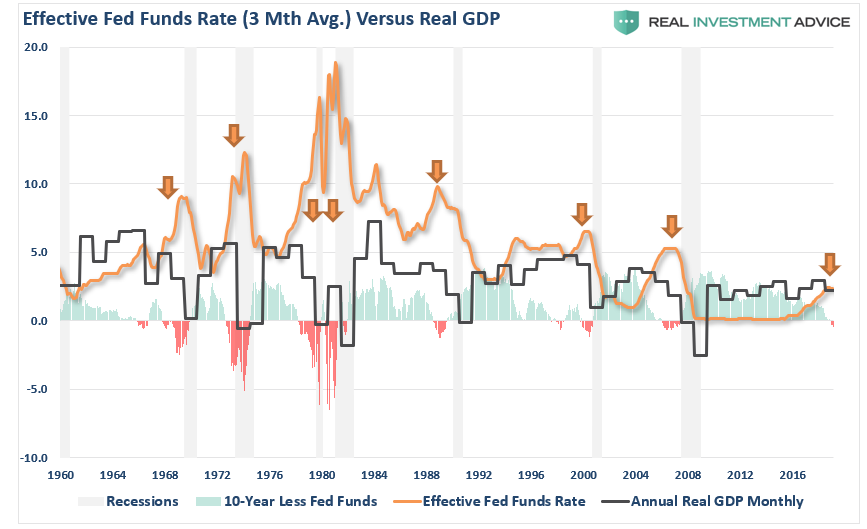

Here is a chart of the Effective Fed Funds Rate versus the Neutral Rate (Real GDP):

You should note a couple of things.

- It wasn’t until the 1990’s that the “neutral rate” became a thing. However, one of the best indicators of an impending recession is when the 10-year rate is inverted to the Fed Funds rate, as it is now.

- The indicator is even more timely when the curve is inverted combined with the Fed cutting rates, as they are now.

Could this time be different? Absolutely, there is always the possibility this time could be different. However, betting on possibilities versus probabilities tends not to work out well.