Written by Lance Roberts, Clarity Financial

Note: This article was written before Monday’s dramatic selloff.

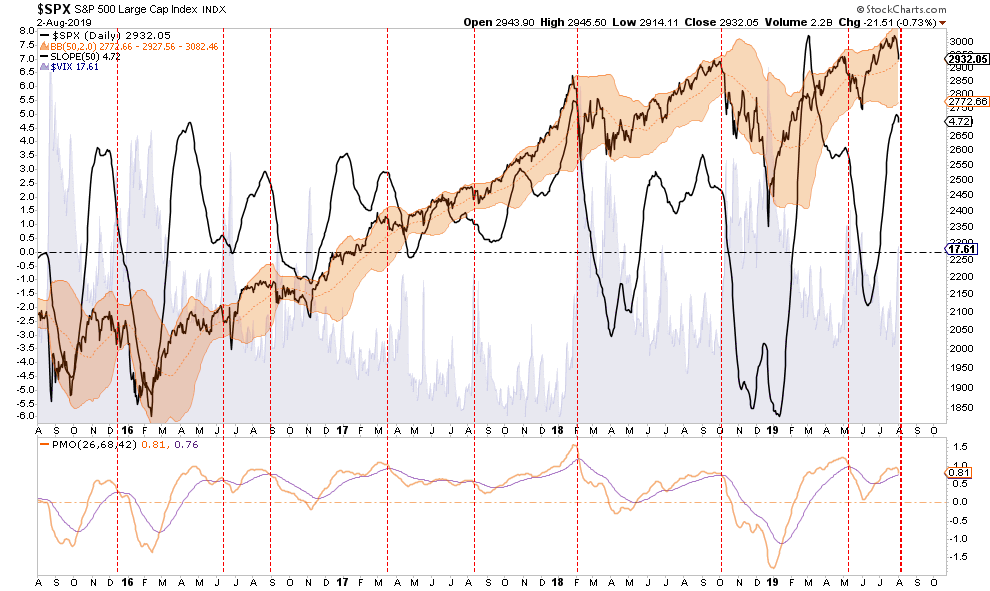

While the current correction has now traced back to initial support at the 50-dma, as shown above, our models still suggest a potential for a continued correction over the next two months.

Please share this article – Go to very top of page, right hand side, for social media buttons.

I loved this note from my friend Victor Adair at Polar Futures Group:

“The market had a lot to digest this past week and thinner-than-normal mid-summer conditions may have exaggerated the moves…but it still feels like there’s a ‘sea-change’ happening here that may be foreshadowing bigger moves to come.

I wrapped up my July 19 TD Notes with, ‘It feels like the stage is set for volatility to jump… I think a lot of recent positioning might have to be reversed.’

This week saw reversals everywhere, and reversals of reversals! Markets had not correctly ‘priced-in’ the Fed and hadn’t anticipated Tariff Man taking another swipe at China. (Retaliation coming?) So…markets has to price-in a ‘new reality’ or, more accurately a ‘new imagining of what is to come.’ The common feature across markets was that volatility surged higher. Fear happens fast.”

Fear does happen fast.

Importantly, while the markets did hold support on Friday, there was enough selling last week to generate are very short-term oversold condition. Markets don’t move in a straight line.

From that view, it is likely we will see a bounce next week following 5-days of fairly brutal selling. Use that bounce to take profits and rebalance risk in portfolios for now.

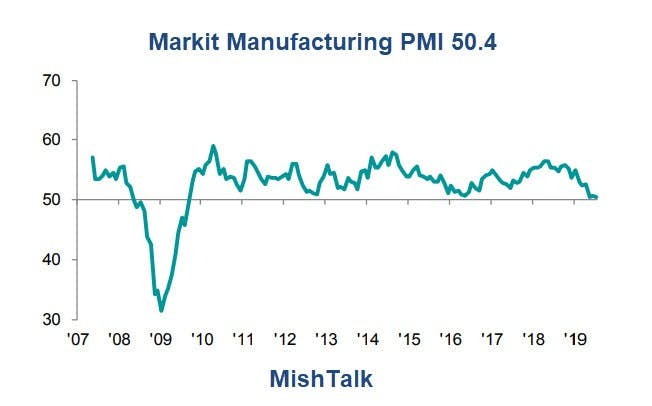

As the markets move past the Fed, and begin to focus on weaker earnings and economic growth, the backdrop becomes more problematic for the bullish case. We suggested last week, the Fed signaled their “rate cut” may be “one and done” for the time being. This could well put them behind the curve, given the ongoing collapse in many of the economic indicators. As noted by Mike Shedlock this week:

“Look at new export orders, deliveries that are expanding while the backlog of orders is now deep in contraction. Manufacturers cannot use backlogs to keep production up with new orders barely above break even. The details suggest production will go into contraction next month. Markit PMI Lowest Since September 2009″

More importantly, the backdrop to equities has skewed to levels which have historically denoted elevated risks for investors. As noted by BofA’s Michael Harnett (via Zerohedge)

- Fed cut makes it 729 global central bank cuts since Lehman bankruptcy. (You shouldn’t be cutting rates if economic growth was strong and supportive of higher asset values)

- Soaring US consumer confidence at highest level vs. plunging German business confidence since Q4’98…when Fed cut rates “mid-cycle” igniting bubble of ’99.

- EM equities at lowest level vs. US equities since 2003…China weak, US$ strong.

- Wall St (US private sector financial assets) now 5.5x the size of Main St (US GDP)… between 1950 & 2000 the norm was 2.5-3.5x…Wall Street is now “too big to fail”.

- Global debt now 3.2x the size of global GDP, an all-time high.

- Fresh China tariffs in Sept would raise average US tariff on total imports to 5.6% from 4.5%, highest since 1972…was 1.5% before Trump.

- US companies spent $114 on buybacks for every $100 of capex in past 2 years… between 1998 & 2017 they spent $60 for every $100 of capex.

- Inflows to bond funds ($278bn) rising at a record pace in 2019.

- Past 10 years $4.1tn into passive investment funds vs. $1.5tn out of active funds.

- Just 6% of MSCI ACWI stocks account for 53% of YTD global equity return.

Here is the overlooked issue. It is taking sustained lower rates, and more debt, to just maintain the system currently. The problem for the Fed, and the markets, is that rate cuts, at this late stage of the economic cycle, will have a muted effect due to a broken transmission system. As noted by Austan Goolsby via NYT:

“It’s not just that the Fed has a ‘short runway,’ rates are already so low that it is impossible to cut them four or five percentage points in the face of a recession, as the Fed has done in the past. The real problem is that recent experience and new economic research suggest that rate cuts in general may have a more modest impact on the economy now than they usually do.

The worry, arising from some important new research, is that the benefits of Fed rate cuts in today’s environment may be substantially overrated.”

His point is critically important.

Lower rates have less impact on the “economy,” when the monetary transmission system is weak. This is evident from the fact that surging asset prices have left 90% of the population behind in terms of higher levels of prosperity.

This also is why tax cuts failed to work as intended. After a decade of low rates, and excess liquidity, the ability to “pull-forward” demand has become limited. As Austan notes:

“A similar dynamic probably helps explain why the 2017 corporate tax cut has had such an underwhelming impact on companies’ capital investment. Fundamentally, there wasn’t much pent-up demand for investment after years of low rates, accelerated depreciation, “temporary” investment expensing and other stimulus. That lack of pent-up demand also means that cutting interest rates now is unlikely to entice businesses to invest much more.

So it’s a twofold problem: The Fed has less room to cut rates, and the benefit from cutting them is smaller than usual. We should be wary of vesting too much importance on Fed moves.”

Then you have a President “hellbent” on making this worse by Tweeting out yesterday:

“Trade talks are continuing, and during the talks the U.S. will start, on September 1st, putting a small additional Tariff of 10% on the remaining 300 Billion Dollars of goods and products coming from China into our Country. This does not include the 250 Billion Dollars already Tariffed at 25%.

As I have stated repeatedly in the past, this action was likely.

- A Trade deal wasn’t reached and China will continue to refuse to give in to demands for economic reform. Additional tariffs are coming by the end of the summer.

- Existing tariffs, which were just ratcheted up at the beginning of June, have not been fully recognized in the economy as of yet. More “pain” is coming by the end of the summer.

- While the markets think that Trump has the ‘upper hand,’ it is China for now. They can hold out to economic pressures far longer than Trump, as Xi is not facing re-election. China knows this.

While the latest move by President Trump could well be an attempt to force the Fed to lower rates further, this is a dangerous game of brinkmanship. The Fed’s rate cuts, and changes in monetary policy, take between nine and twelve months to filter into the economy. However, Trumps “tariffs,” have an almost immediate impact on market and corporate psychology.

While Trump may well get his rate cuts, as noted above, it will likely have a much more muted effect than what is currently believed. With the additional pressure on corporate profits, in an already deteriorating environment, this could develop into a potentially worse outcome for investors.