Written by Lance Roberts, Clarity Financial

The $70 Trillion Dollar Graveyard

Please share this article – Go to very top of page, right hand side, for social media buttons.

Last Thursday, Congress passed the spending bill we discussed earlier last week:

“A divided House on Thursday passed a two-year budget deal that would raise spending by hundreds of billions of dollars over existing caps and allow the Government to keep borrowing to cover its debts, amid grumbling from fiscal conservatives over the measure’s effect on the federal deficit.

65 Republicans joined the Democratic majority in the 284-149 vote, with 132 Republicans voting against the bill, despite President Trump’s endorsement and pressure from key outside groups, including the Chamber of Commerce, to avoid a potentially catastrophic default on the Government’s debt.”

I highlighted the last sentence in red because it is an outright “LIE” used to convince Americans that out of control spending must be done.

The reality is that “interest payments on the debt” are part of the MANDATORY spending in our budget along with social security, medicare, etc. Currently, about $0.75 of every dollar of tax revenue goes to mandatory spending. For the last few months the Government has been at its statutory debt limit, and “surprise” we didn’t default on our debt. Why? Because there is enough revenue currently coming in to cover the mandatory spending.

As I noted specifically last week,

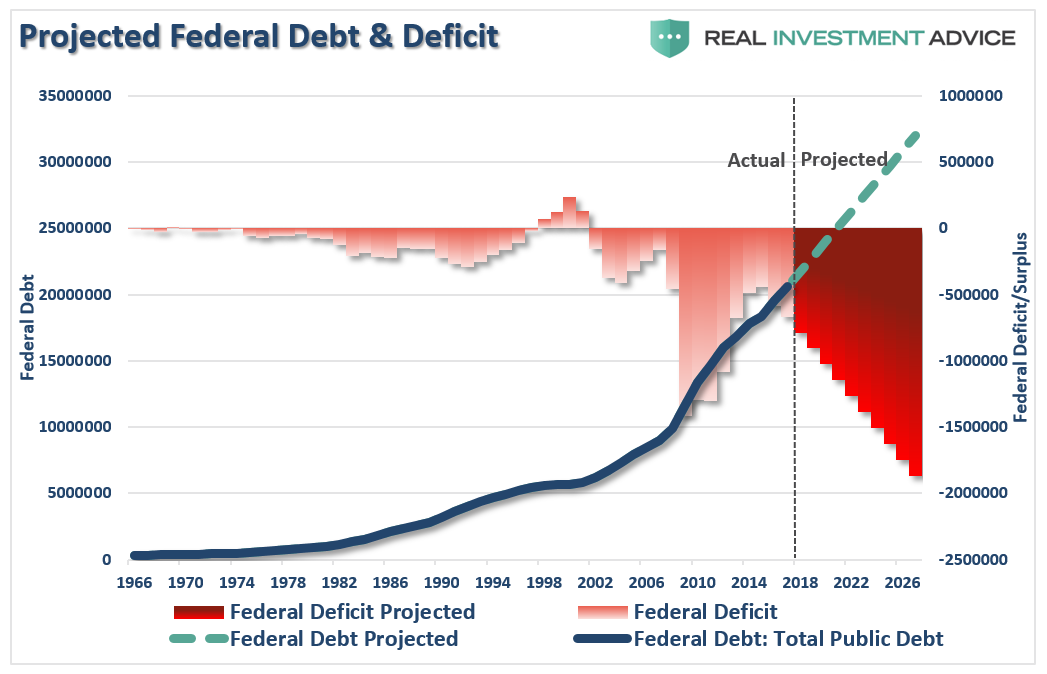

“In 2018, the Federal Government spent $4.48 Trillion, which was equivalent to 22% of the nation’s entire nominal GDP. Of that total spending, ONLY $3.5 Trillion was financed by Federal revenues, and $986 billion was financed through debt.

In other words, if 75% of all expenditures is social welfare and interest on the debt, those payments required $3.36 Trillion of the $3.5 Trillion (or 96%) of revenue coming in.”

Do some math here.

The U.S. spent $986 billion more than it received in revenue in 2018, which is the overall ‘deficit.’ If you just add the $320 billion to that number you are now running a $1.3 Trillion deficit.

The U.S. will not default on its debt.

This is particularly the case since we no longer have any budgetary controls.

Importantly, the spending increase of $320 billion is on top of the annual 8% automated budget increase and the preexisting deficit. My original projection above is too conservative by $500 billion, or more.

But that’s not the real story.

The crux of that article was focused on the roughly $6 Trillion of unfunded liabilities of U.S. pension funds which Congress is now drafting a piece of legislation for entitled the “Rehabilitation For Multi-employer Pensions Act.”

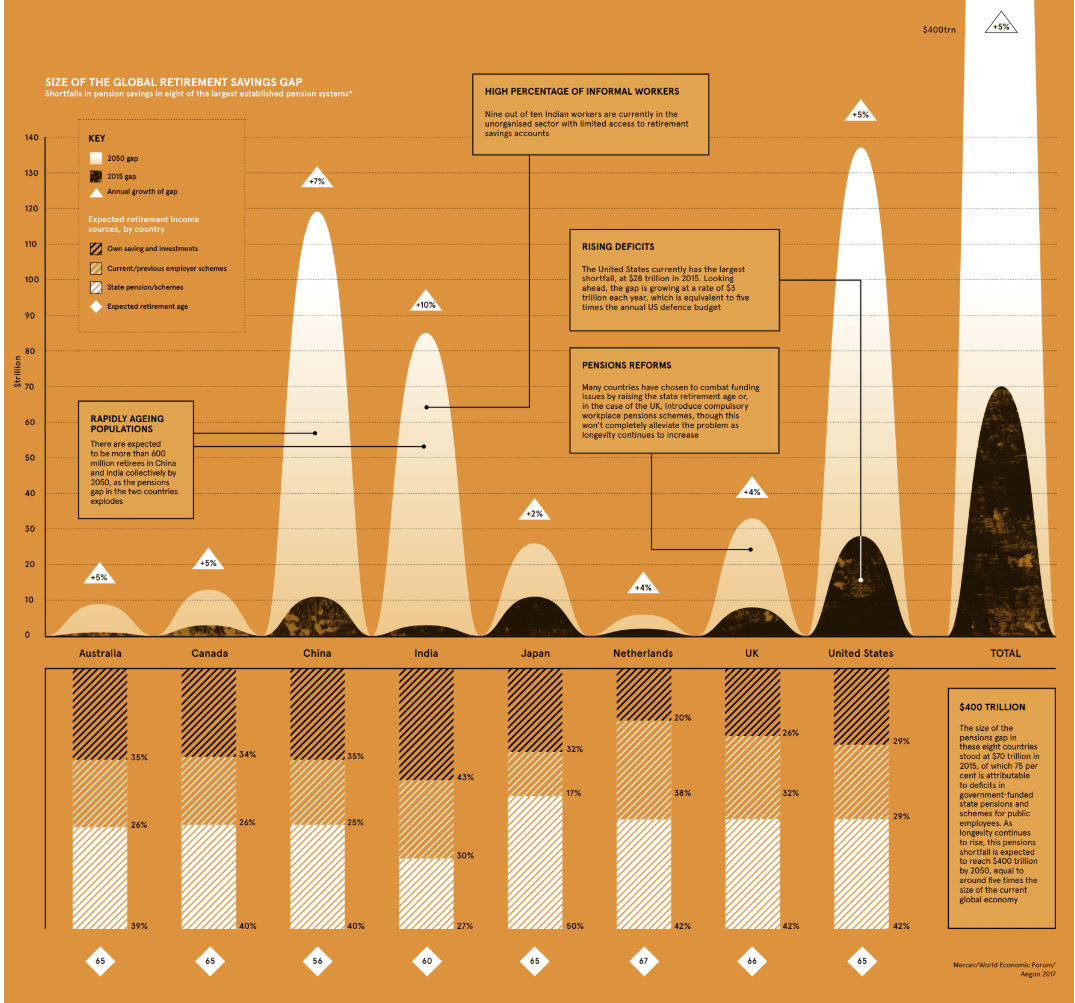

As noted in that article, while Congress is preparing a bailout for U.S. pension funds, there is a $70 Trillion pension problem globally which is not being addressed.

“According to an analysis by the World Economic Forum (WEF), there was a combined retirement savings gap in excess of $70 trillion in 2015, spread between eight major economies…

However, this isn’t the $70 Trillion graveyard we are addressing today. From CNN:

“America’s debt load is about to hit a record. The combination of cheap money and soaring debt helped fuel the decade-long economic expansion and bull market, but America’s gluttony of loans could work against it if its fragile economic balance shifts.

In the first quarter of 2019, the United States’ total public- and private-sector debt amounted to nearly $70 trillion, according to research by the Institute of International Finance. Federal government debt and liabilities of private corporations excluding banks both hit new highs.”

Oh…you are talking about THAT $70 Trillion.

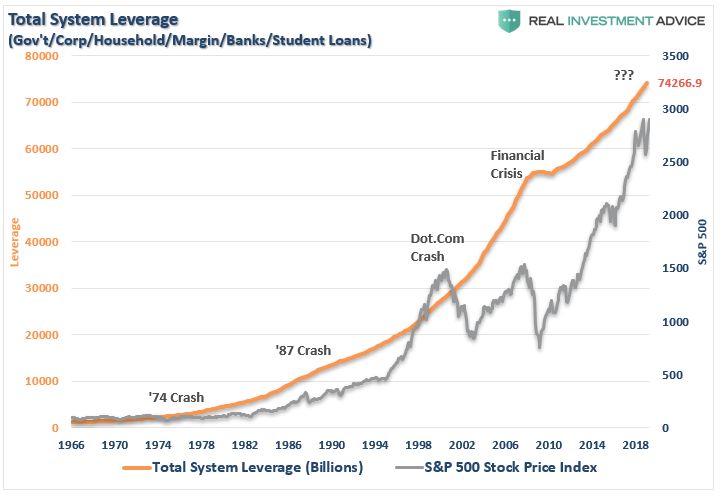

The chart below is Total U.S. Credit Market Debt (including Student Loans) which is currently running just a smidgen over $74 Trillion.The last time there was even a hint of deleveraging was during the “Financial Crisis.”

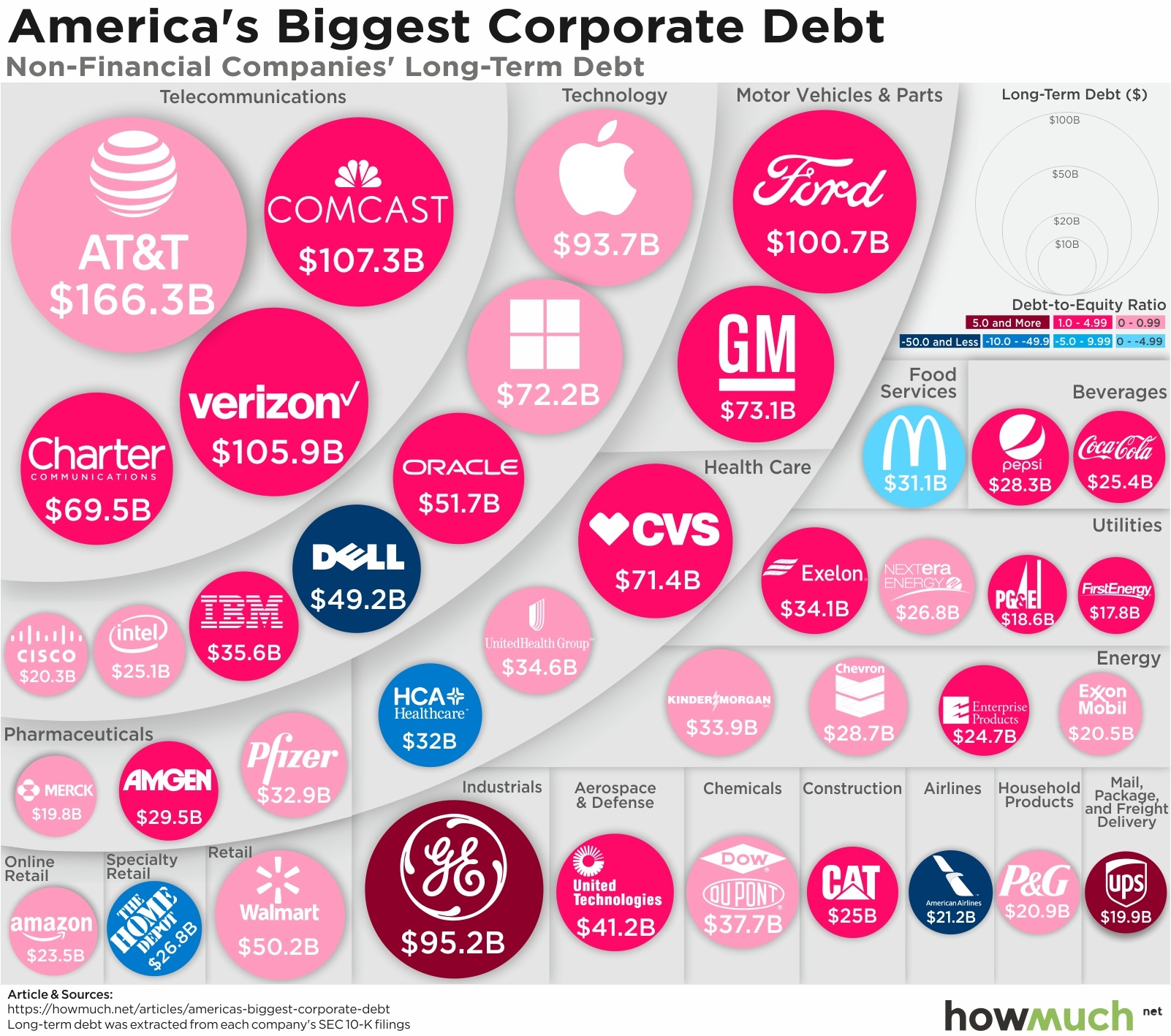

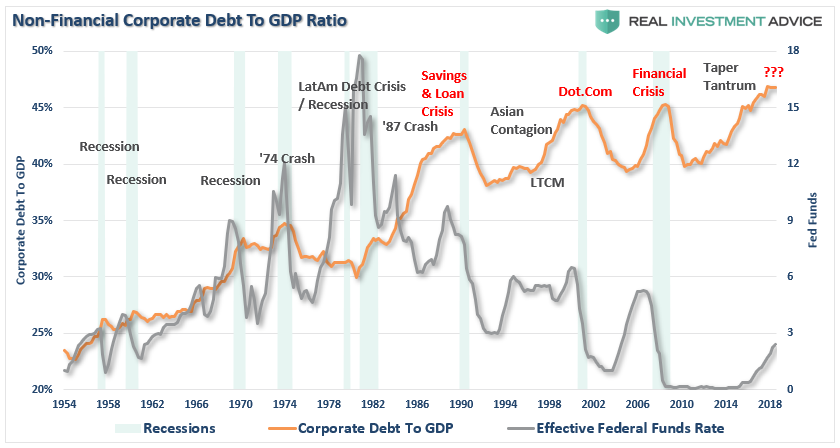

Corporate debt is a problem.

The wonderful website “HowMuch” put the corporate debt bubble into a graphic to help us visualize the potential for widespread defaults during the next economic and market downturn.

The problem with corporate debt is the amount of debt which is at risk of default during the next economic recession. (This isn’t an “IF,” it’s a “WHEN” statement.)

Let’s start with a note from Michael Lebowitz:

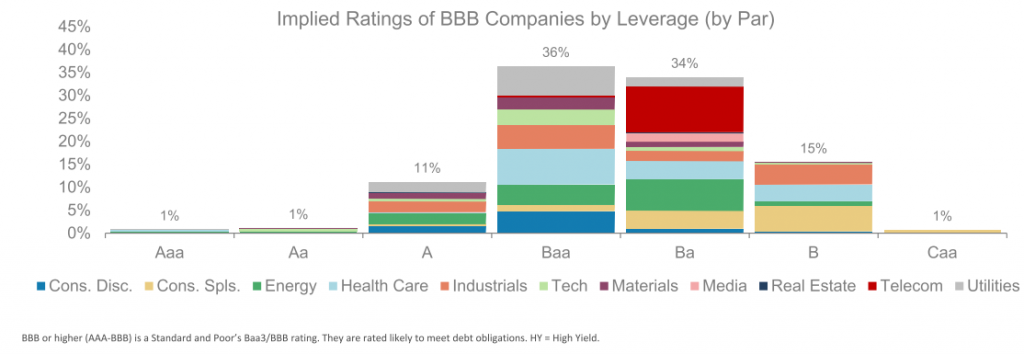

“The graph shows the implied ratings of all BBB companies based solely on the amount of leverage employed on their respective balance sheets. Bear in mind, the rating agencies use several metrics and not just leverage. The graph shows that 50% of BBB companies, based solely on leverage, are at levels typically associated with lower rated companies.”

“If 50% of BBB-rated bonds were to get downgraded, it would entail a shift of $1.30 trillion bonds to junk status. To put that into perspective, the entire junk market today is less than $1.25 trillion, and the subprime mortgage market that caused so many problems in 2008 peaked at $1.30 trillion.Keep in mind, the subprime mortgage crisis and the ensuing financial crisis was sparked by investor concerns about defaults and resulting losses.”

The reason BBB-rated debt is so plentiful is due to the Fed’s ultra-low interest rate policy over the last decade. Near zero rates, and easy credit terms, has seduced companies into taking on debt to fund operations, dividends, and stock buybacks. The consequence is we are now seeing corporate debt exceeding the levels of the global financial crisis.

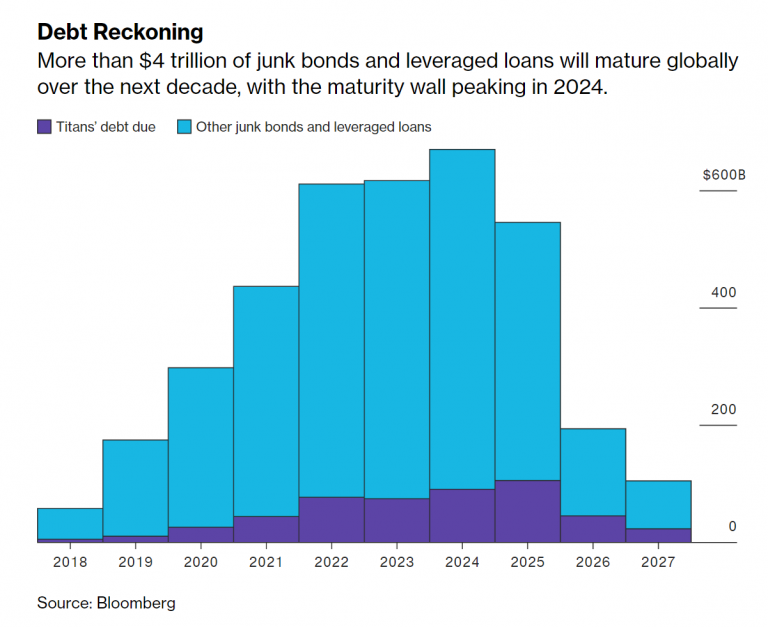

The real risk is that over the next 5-years more than 50% of the junk-bonds and leveraged-loans (which is sub-prime debt for corporations) is maturing and must be refinanced.

Let that sink in for a minute.

A weaker economy, recession risk, falling asset prices, or rising rates could well lock many corporations OUT of refinancing their share of this $4.88 trillion debt. Defaults will move significantly higher, and much of this debt will be downgraded to junk.

But it isn’t just corporate debt that’s a problem. We will discuss the bigger problem tomorrow.

.