Written by Lance Roberts, Clarity Financial

Last week, we discussed the setup for a near-term mean reversion because of the massive extension above the long-term mean.

Please share this article – Go to very top of page, right hand side, for social media buttons.

To wit:

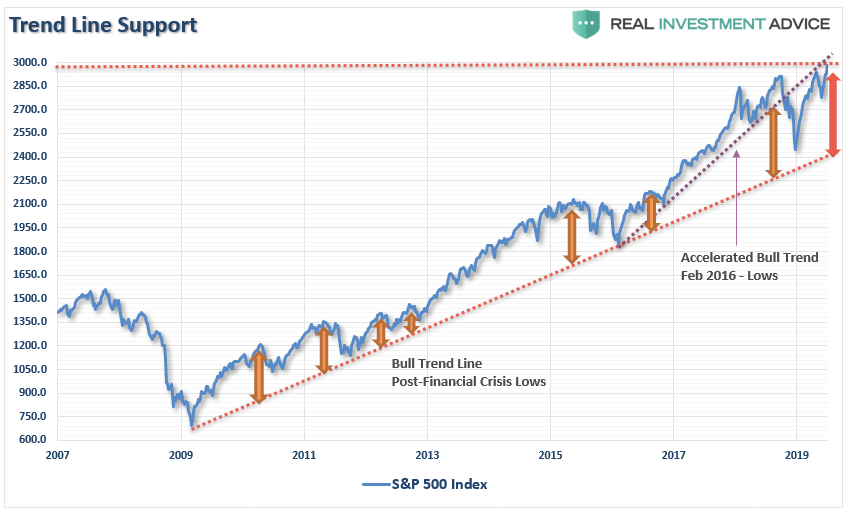

“There is also just the simple issue that markets are very extended above their long-term trends, as shown in the chart below. A geopolitical event, a shift in expectations, or an acceleration in economic weakness in the U.S. could spark a mean-reverting event which would be quite the norm of what we have seen in recent years.”

This analysis is what led us to take action for our RIAPRO subscribers last week (30-Day Free Trial), as we added a 2x-short S&P 500 index fund to Equity Long-Short Account to hedge our longs (GOOG, CRM, NVDA, EMN, IVV, RSP) against a potential mean reversion.

“This morning, we are adding a small 2x S&P 500 short position to the trading portfolio to hedge our core long positions against a retracement over the next few weeks. We will remove the short if the market can regain its footing and move higher, or the market sells off and reaches oversold conditions.”

This is the purpose of hedging, as it reduces volatility over time, which inherently reduces the risk of emotionally based trading mistakes.

My friends at Polar Futures Group laid out the same concerns on Friday:

“The mean reversion trade: For the past few weeks I’ve been musing that the “irresistible force” that has moved all markets has been the aggressive repricing of future interest rate expectations since last November. We’ve had a HUGE rally in the bond market, MASSIVE flows into bond funds, record levels (>$13.7T) of negative yielding bonds, inverted yield curves, even Greek bonds trading through Treasuries…as markets anticipate a recession and much more Central Bank largess…which might just take us into MMT and/or never-never land where the Central Banks just buy all the bonds and that’s that. I’ve thought that this irresistible force may have gone too far too fast and was due for a “set-back” which would precipitate mean reversion trades across markets.

The core concepts of the mean reversion trades I’m considering are as simple as, 1) the public buys the most at the top (thank you, Bob Farrell,) and 2) when they’re yelling you should be selling, and 3) positioning risk leaves some markets especially vulnerable.”

They are exactly right.

While the market is rallying in anticipation of more Central Bank easing, especially following the recent announcement by the ECB of lower rates and more QE, the markets are momentarily detached from weaker earnings growth, weaker economic growth, and a variety of other market-related risks.

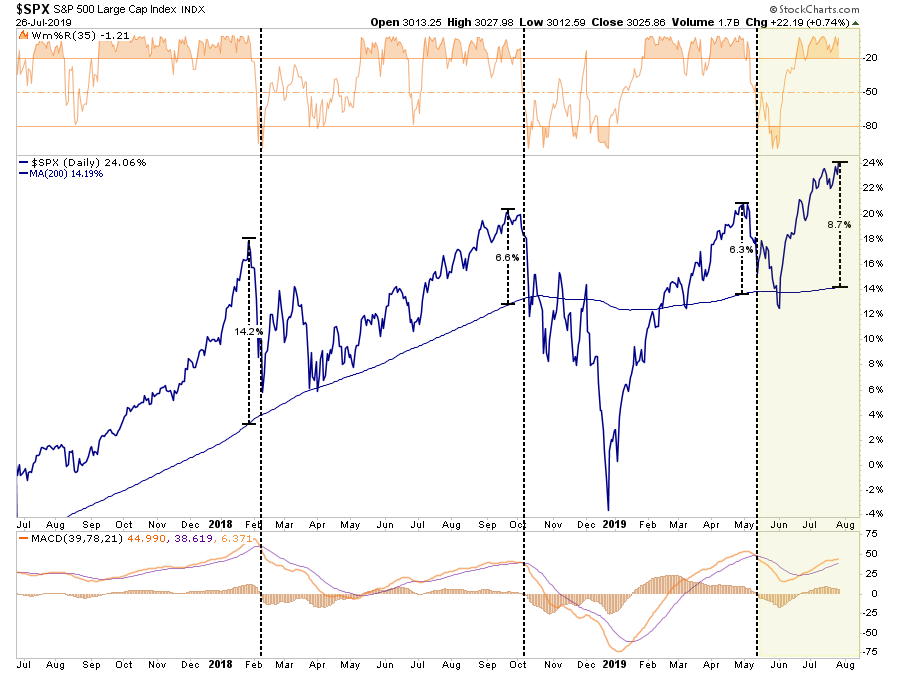

However, in the very short-term, the market is grossly extended and in need of some correction action to return the market to a more normal state. As shown below, while the market is on a near-term “buy signal” (lower panel) the overbought condition, and near 9% extension above the 200-dma, suggests a pullback is in order.

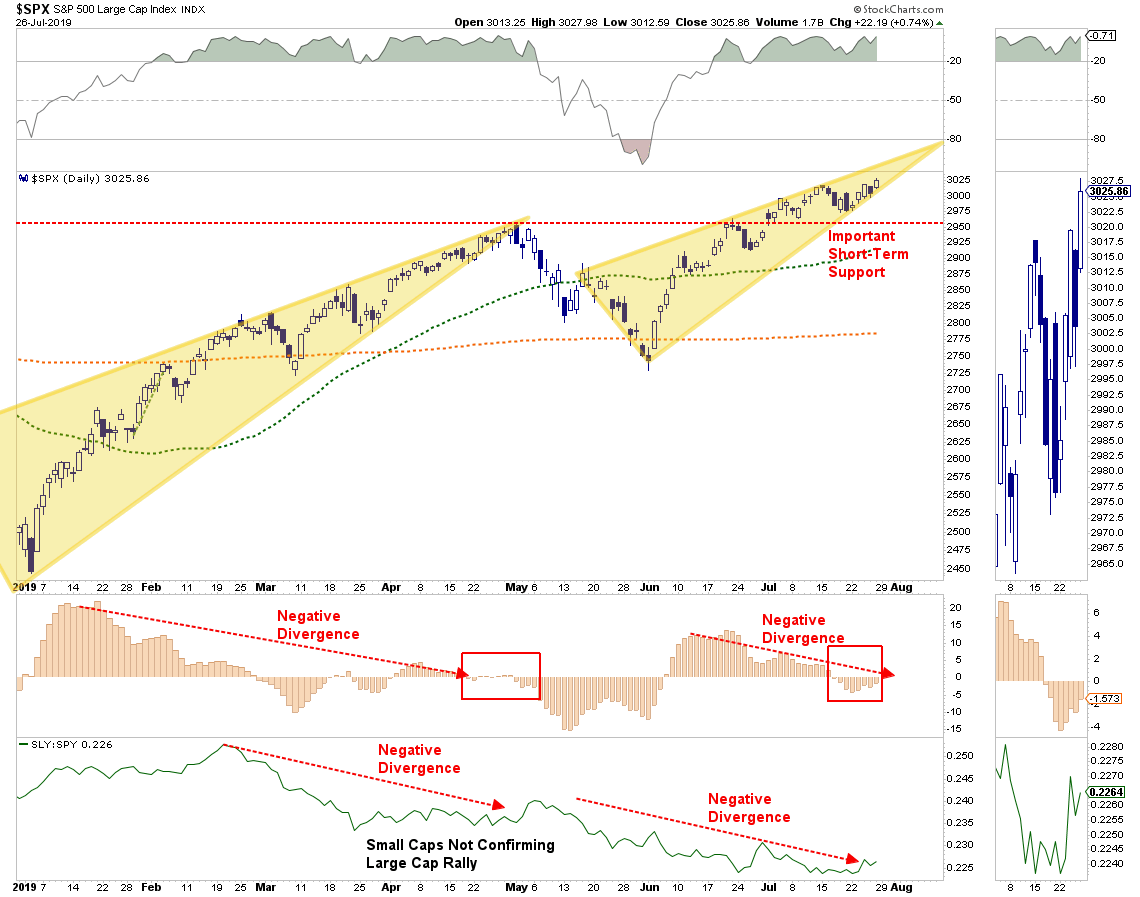

As we have noted over the last few weeks, the very tight trading range combined with negative divergences also does not historically suggests continued bullish runs higher without some type of corrective action first.

All of this supports why we trimmed our long positions slightly last week and increased our cash holdings for the time being.

Our models still suggest a likely correction over the next two months as we move past the Fed. Such is particularly the case if the Fed signals their “rate cut” may be “one and done” for the time being.

But for now, we are going to opt to “wait and see” what happens.

.