by Lance Roberts, Clarity Financial

On Thursday and Friday, the markets mustered a “Pre-G20 rally” in anticipation of a positive outcome from the meeting between President Trump and Xi. I will discuss the outcome of this meeting in just a moment.

Please share this article – Go to very top of page, right hand side, for social media buttons.

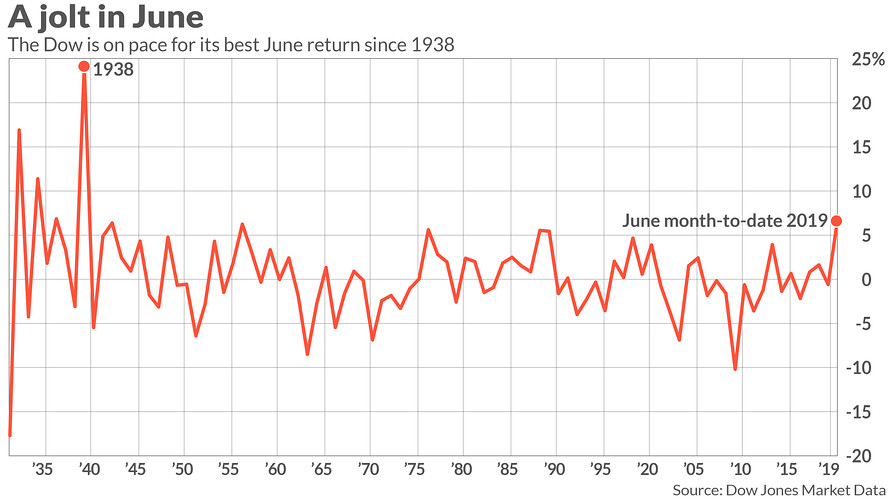

The good news is that June was one of the best performing months for the Dow Jones Industrial Average over the past 80-years.

That certainly was an impressive rally if you bought into the markets on June 1st.

Unfortunately, what the headlines don’t tell you is that the “strongest June rally in the last 80 years” failed to recover the losses from one of the worst May months on record as well.

In other words, most investors simply recovered previous losses.

However, as noted, the rally was something we had expected and discussed repeatedly in this weekly missive.

“In the very short-term, the markets are oversold on many different measures. This is an ideal setup for a reflexive rally back to overhead resistance.”

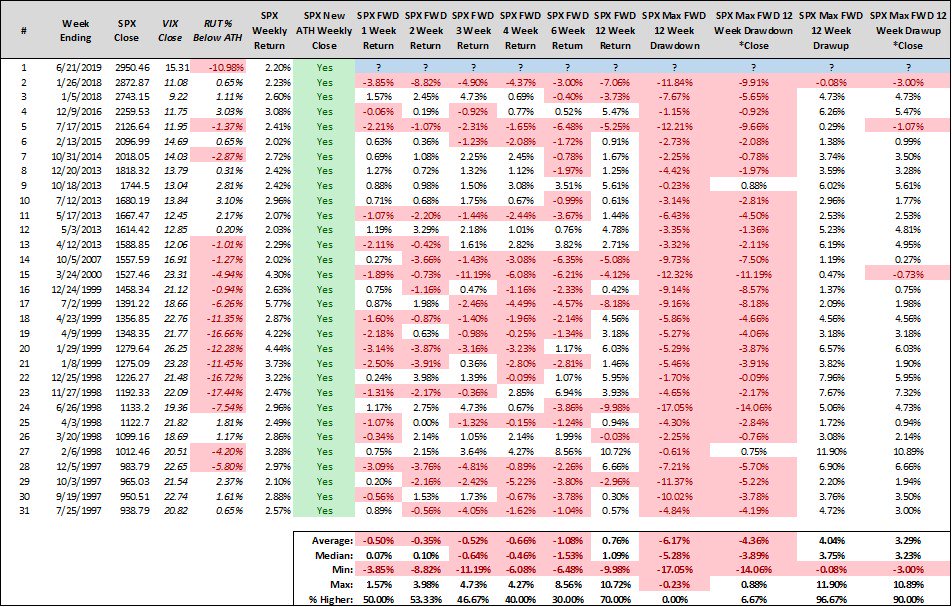

The question now is “how much more rally is there to go?”

As we noted in last Tuesday’s update:

“Steve Deppe also made an important observation Twitter that when the S&P 500 has gained at least 2% in a week and finished at a new weekly high – the case on Friday – the S&P was lower six weeks later 70% of the time.”

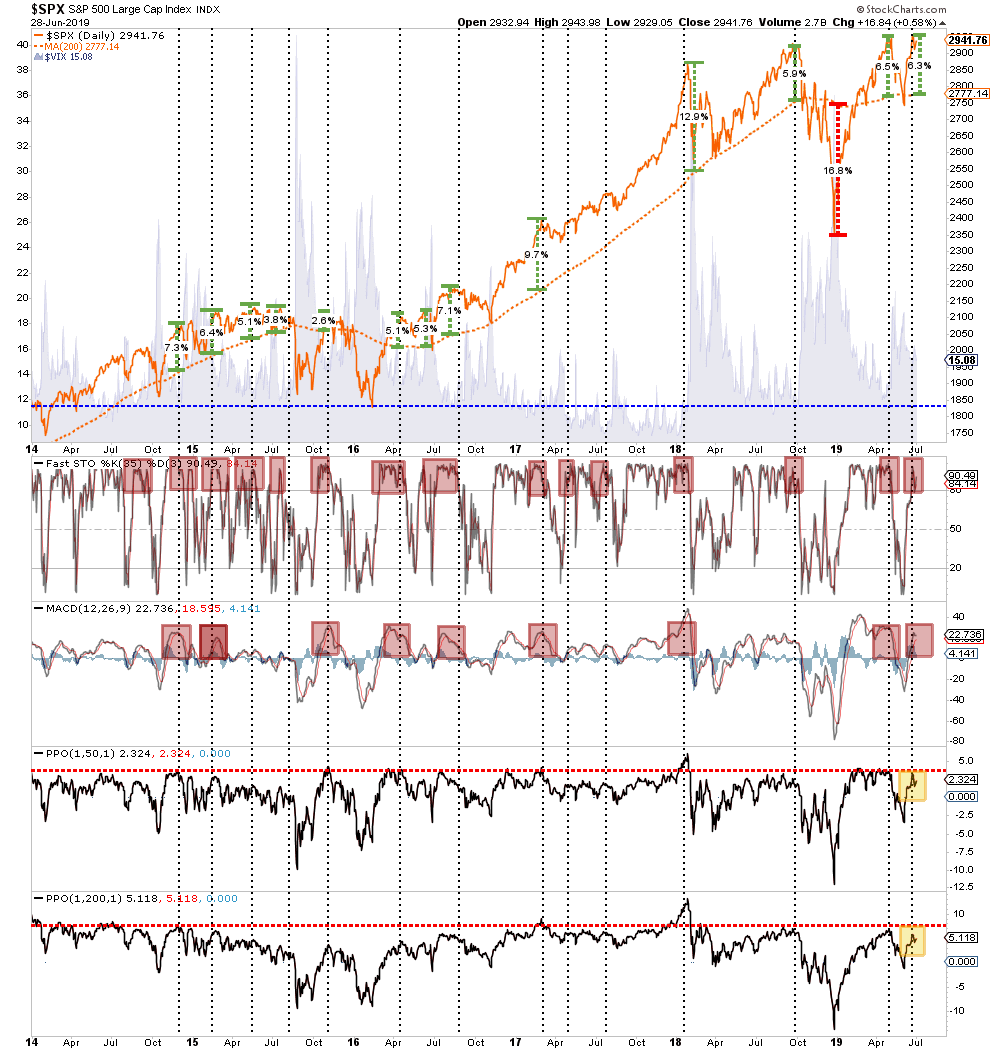

Much like an engine, markets operate on “fuel.” In other words, when there is a lot of “pent up” demand for equities, prices rise as demand is filled, and buyers are willing to pay higher prices to “get in.” The opposite is also true.

Also, prices are also confined by long-term moving averages. These moving averages, act like gravity, so when prices deviate by more than 5% from the long-term averages, reversions tend to occur.

As shown in the chart below, the market is currently very overbought, little pent-up demand, and is more than 6% above its 200-dma.

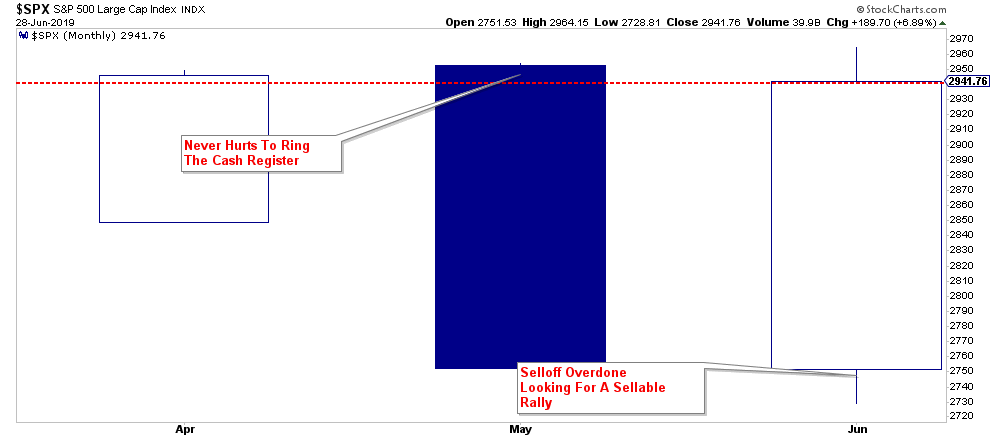

Interestingly, this was exactly the same analysis we ran in May when we suggested taking profits then. To wit:

“”From a portfolio management standpoint, the reality is that markets are very extended currently and a decline over the next couple of months is highly likely. While it is quite likely the year will end on a positive, particularly after last year’s loss, taking some profits now, rebalancing risks, and using the coming correction to add exposure as needed will yield a better result than chasing markets now.”

Since May:

- The economic backdrop has weakened materially.

- Earnings expectations continue to fall. .

- While asset prices are near record highs, corporate profits are the same level as in 2014.

- The Fed has NOT cut rates yet and is still reducing their balance sheet.

- Global economic growth continues to weaken.

- Existing tariffs are continuing to work their way through the system

- Recession risks have risen markedly in recent months.

In other words, the supportive backdrop for equity investors is hinged on the “hope” of the Fed cutting rates and a resolution to the “trade war.”

Monday is that start of Q3 for money managers so a rally is expected that could well push markets to new highs temporarily.

This is why we remain long equities currently, we are hedged with an overweight position in cash, are maintaining our fixed income exposure and have recently added plays to participate with a “steepening” yield curve.

However, there are bigger risks still at play and worth watching.