Written by Lance Roberts, Clarity Financial

Winter is Coming

Just as Jon Snow faced the “White Walkers'” in the battle to save civilization, Trump has squared off with China again over trade.

Please share this article – Go to very top of page, right hand side, for social media buttons.

Most of the comments I have read about the ongoing “trade deal” negotiations are, in my opinion, wrong. The general belief is that China “wants” a deal with the U.S. and Trump has the upper hand in this matter. To wit a recent comment by Kevin Giddis via Raymond James:

“It doesn’t help when the Chinese reportedly backed away from issues important to the U.S. just days before they are set to meet to negotiate a deal. Could this be as simple as a ‘clash of culture,’ or the way each side has postured themselves to get a deal done?”

I believe this to be incorrect and I laid out my reasoning Tuesday in “Trade War In May, Go Away:”

“The problem, is that China knows time is short for the President and subsequently there is ‘no rush’ to conclude a ‘trade deal’ for several reasons:

- China is playing a very long game. Short-term economic pain can be met with ever-increasing levels of government stimulus. The U.S. has no such mechanism currently, but explains why both Trump and Vice-President Pence have been suggesting the Fed restarts QE and cuts rates by 1%.

- The pressure is on the Trump Administration to conclude a “deal,” not on China. Trump needs a deal done before the 2020 election cycle AND he needs the markets and economy to be strong. If the markets and economy weaken because of tariffs, which are a tax on domestic consumers and corporate profits, as they did in 2018, the risk off electoral losses rise. China knows this and are willing to “wait it out” to get a better deal.

- As I have stated before, China is not going to jeopardize its 50 to 100-year economic growth plan on a current President who will be out of office within the next 5-years at most. It is unlikely, the next President will take the same hard-line approach on China that President Trump has, so agreeing to something that is unlikely to be supported in the future is unlikely. It is also why many parts of the trade deal already negotiated don’t take effect until after Trump is out of office when those agreements are unlikely to be enforced.

Even with that said, the markets rallied from the opening lows on Monday in ‘hopes’ that this is just part of Trump’s ‘Art of the Deal’ and China will quickly acquiesce to demands. I wouldn’t be so sure that is case.”

Doug Kass agreed with my views yesterday:

“It was never likely that tariff pressures were ever going to force China to succumb and altar deep rooted policy and the country’s ‘evolution’ and planned economic growth strategies.

Trump’s approach failed to comprehend the magnitude of the tough structural issues (that were never going to be resolved with China) and, instead, leaned on a focus of the bilateral trade deficit. Technology transfer, state-sponsored industrial policy, cyber issues and intellectual property theft were likely never on the table of serious negotiation from China’s standpoint and despite Trump’s protestations that discussions were going well.

As I have suggested for months, the unilateral imposition of tariffs will cause more economic disruption than the Administration recognizes (in our flat and interconnected economic world):

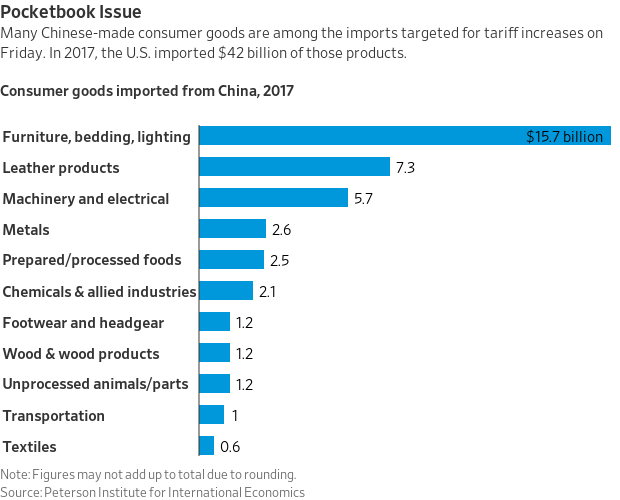

- China’s role in world trade is important – the country is the third largest exporter in the world.

- Specifically, China is a prime source of cheap, imported goods for American consumers.

- China is the largest owner of U.S. debt.

Last night at a political rally in the Panhandle of Florida the president said that “we don’t have to do business” with China. That statement is short-sighted.

I agree particularly with the last point. There is little evidence that U.S. consumers have the “willpower” to either forgo purchases or be willing to pay substantially higher prices.

Trump was also misguided on Friday when he tweeted:

The process has begun to place additional Tariffs at 25% on the remaining 325 Billion Dollars. The U.S. only sells China approximately 100 Billion Dollars of goods & products, a very big imbalance. With the over 100 Billion Dollars in Tariffs that we take in, we will buy agricultural products from our Great Farmers, in larger amounts than China ever did, and ship it to poor & starving countries in the form of humanitarian assistance.In the meantime, we will continue to negotiate with China in the hopes that they do not again try to redo deal!

Tariffs will bring in FAR MORE wealth to our country than even a phenomenal deal of the traditional kind.Also, much easier & quicker to do. Our Farmers will do better, faster, and starving nations can now be helped. Waivers on some products will be granted, or go to new source! If we bought 15 Billion Dollars of Agriculture from our Farmers, far more than China buys now, we would have more than 85 Billion Dollars left over for new Infrastructure, Healthcare, or anything else. China would greatly slow down, and we would automatically speed up! – Donald J. Trump, May 10, 2019

The economy is not built on “goodwill.” Let’s examine his comment.

- We tax China more, which means their consumption of U.S. products will decline as they seek cheaper sources elsewhere and in turn U.S. exports fall which comprises more than 40% of U.S. profits.

- U.S. buys products from farmers and gives it poor countries. While a great idea from a humanitarian standpoint, and does stabilize farmers short-term, it again has a negative impact on exports and corporate profits from other sectors of the economy.

- Trade is a zero-sum game. There is only a finite amount of supply of products and services in the world. If the cost of U.S. products and services is too high, China sources demand out to other countries which drain the supply available for U.S. consumers. As imbalances shift, prices rise, increasing costs to U.S. consumers.

As noted, tariffs impact domestic consumers more than then impact to China. If tariffs impact China they stimulate their economy with massive credit injections just as we have seen them do recently. The U.S. doesn’t have that luxury currently which is why both President Trump and Vice-President Mike Pence have discussed the need to drop rates by 1% now while the economy is still expanding. To wit:

This is also extremely short-sighted and dangerous.

Yes, it would have the effect of lifting markets higher temporarily, but would only ensure that the next recession and coinciding market crash would be larger with no “policy tools” available to offset the slide.

Secondly, Trump attacking China on the trade deficit is equally short-sighted.

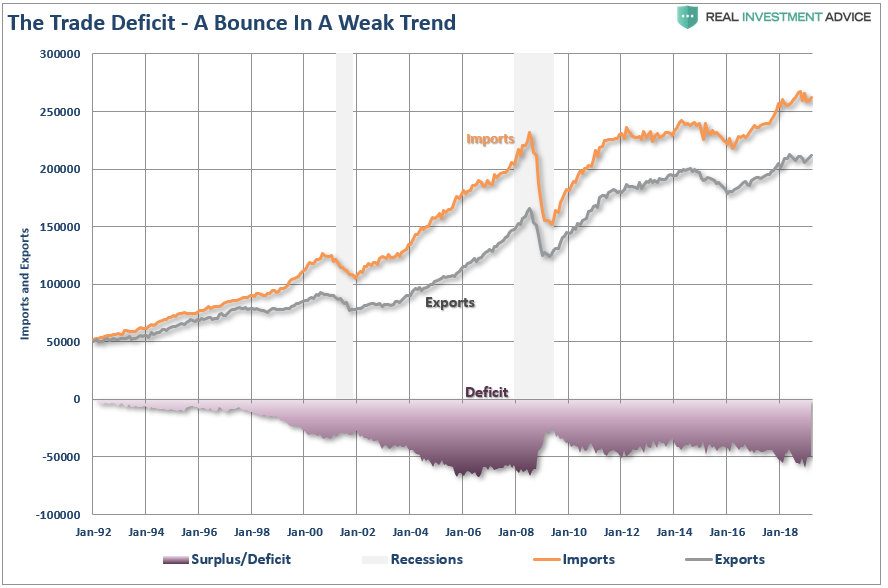

We have run a trade deficit since Reagan came into office as American’s went on a “credit-driven” consumption spending spree. That deficit has continued to grow over the years as credit-based consumption in the U.S. has outstripped the rest of the world’s ability to keep pace. As a function, we import more than we export.

Again, exports account for roughly 40-50% of corporate profitability and we are a very “flat and interconnected world.”

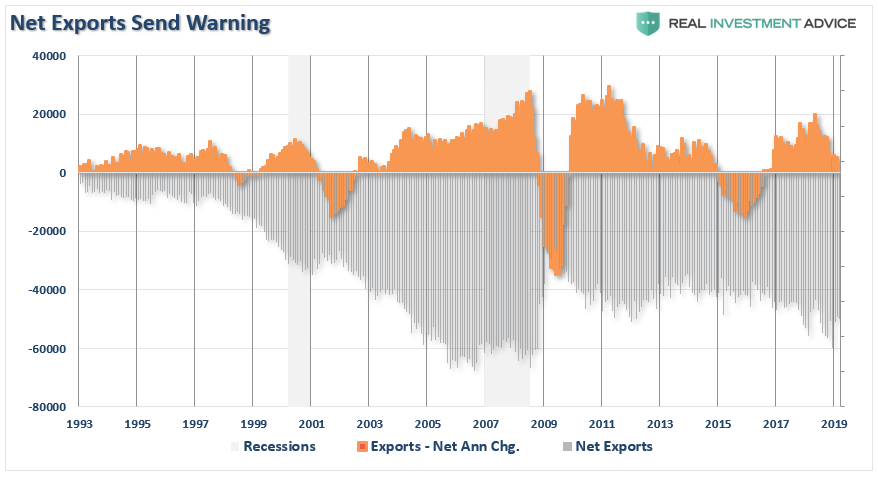

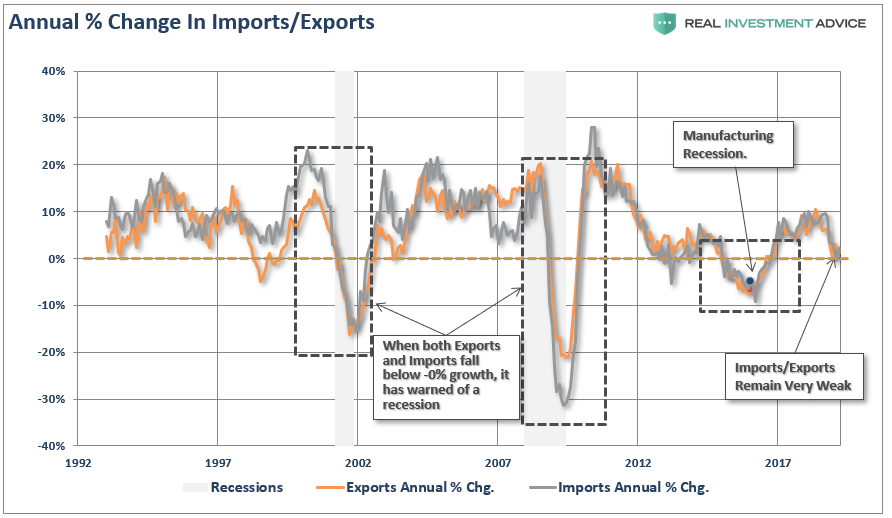

The attack on the trade is having a knock-off effect of pushing the dollar higher which is a direct negative to exporting companies. Furthermore, global economic weakness is gaining steam and the demand for exports is declining. Note in the chart below, that it is not “negative” net exports that signal recessions, but it is when net exports peak and decline toward zero. (While 2012 was not an official recession, it was for all intents and purposes a manufacturing recession.)

The chart below deconstructs net exports (exports less imports, a direct input into the GDP calculation) where you can see that both the demand for exports and imports is declining. This is indicative of a weakening economic environment which will translate into weaker earnings for U.S. multi-national corporations.

Trump is picking the wrong time in the cycle to add additional costs to both consumers and exporters. While imposing “tariffs” may sound like a good idea in theory, the reality is that it is the consumer that pays the price, literally.

For Trump…time is short. A recession is coming and the Federal Reserve is already preparing for it. Via Mish Shedlock on Friday:

“Two Fed governors now propose targeting the long end of the yield curve if there is another recession.

Targeting yields on longer-term rates gets renewed attention from a second Fed governor. The proposed QE Replacement Mechanism was Last Used in WWII.

“Federal Reserve Governor Lael Brainard on Wednesday became the second U.S. central banker to talk about the possibility of targeting longer-term interest rates as a ‘new’ tool to combat the next recession.

Fed Vice Chairman Richard Clarida floated the idea in a speech earlier this year,and has done research on its use in Japan.

‘Once the short-term interest rates we traditionally target have hit zero, we might turn to targeting slightly longer-term interest rates – initially one-year interest rates, for example, and if more stimulus is needed, perhaps moving out the curve to two-year rates,’ Brainard said.

‘Under this policy, the Fed would stand ready to use its balance sheet to hit the targeted interest rate, but unlike the asset purchases that were undertaken in the recent recession, there would be no specific commitments with regard to purchases of Treasury securities,’ she added.”

Think Japan.

Brainard and Clarida are worried about the short end of the curve. Negative interest rates did not help the ECB nor Japan. Then again, pinning the 10-year yield at 0% did not help Japan either.

The result is easy to spot: bubbles and busts of increasing amplitude over time.

By the way, this talk is indicative of a Fed that is far more concerned about a recession than they want you to believe.

In 2007, the banks were preparing for a credit crisis. No one paid attention until it was too late.

For the last 6-months, the Fed has consistently been leaking messages about rising risk in the credit markets and has been quietly prepping for a recession.

Once again, no one is paying attention.

The problem for Trump has always been “time.” He entered office at the tail-end of an economic cycle, and while his policy prescriptions have certainly helped extend the current cycle, they haven’t, and won’t, repeal it.

“Winter IS Coming.”

The only question is whether investors are prepared for it?

If you need help, or have questions, we are always glad to help. Just email me.

See you next week.