Written by Lance Roberts, Clarity Financial

Fortunately, the market rallied on Friday as traders scrambled to hold important support levels following confirmation from Richard Clarida that the Fed has no intention of moving interest rates anytime soon.

Please share this article – Go to very top of page, right hand side, for social media buttons.

Via Bloomberg:

- CLARIDA: INFLATION PRESSURES MUTED, EXPECTED INFLATION STABLE

- CLARIDA: WE’LL WEIGH `WHAT, IF ANY, FURTHER ADJUSTMENTS’ NEEDED

- CLARIDA: FED FUNDS RATE NOW IN RANGE OF NEUTRAL ESTIMATES

- CLARIDA SAYS FED CAN AFFORD TO BE DATA DEPENDENT

- FED’S CLARIDA SAYS U.S. ECONOMY IS IN A `VERY GOOD PLACE’

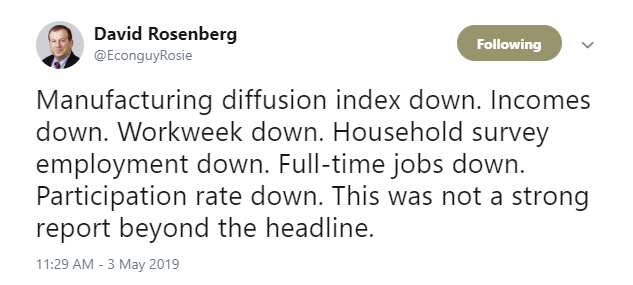

Despite headlines to the contrary, the employment report on Friday was NOT good and we will likely see a good bit of payback next month. David Rosenberg summed it up well:

Nonetheless, the market did rally keeping us in the same place as last week.

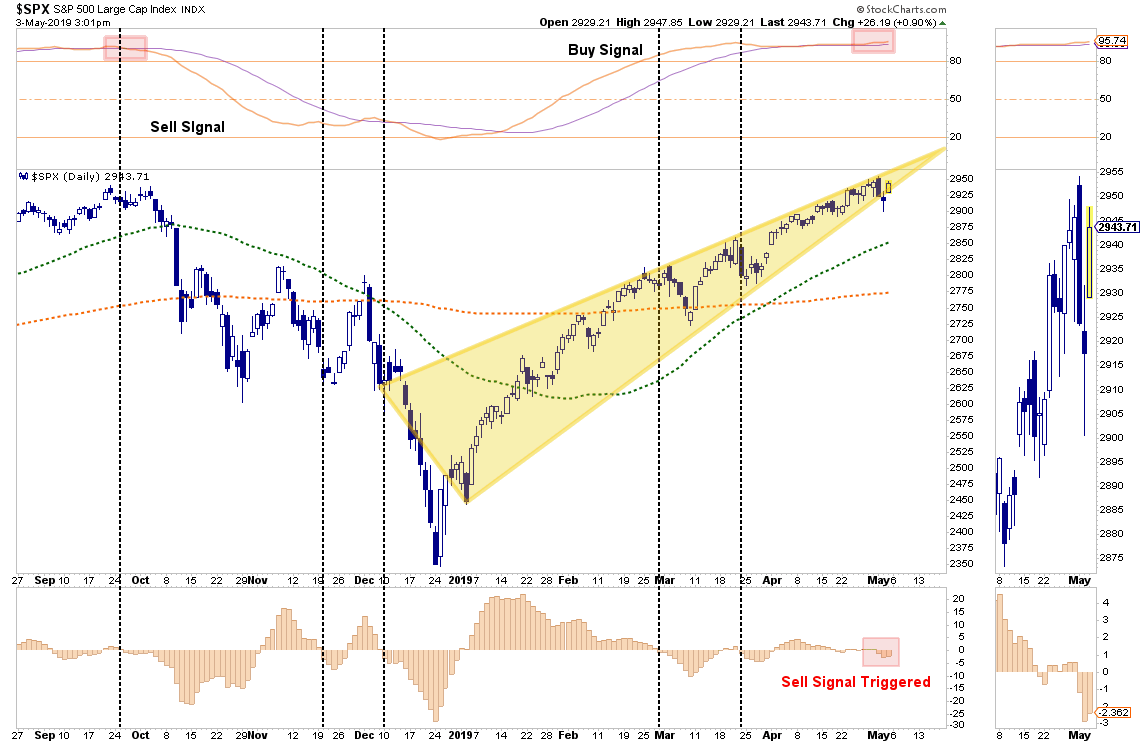

“While that break to the upside was indeed bullish, the market remains very confined to a rising consolidation pattern and failed to close above the intraday all-time highs from last September. With the markets trading on VERY light volume on Friday, combined short-term ‘sell signals’ forming, and pushing more extreme overbought conditions, it is too early to completely remove all risk management controls in portfolios.”

The chart below is updated from last week.

While the market did hold inside of its consolidation pattern, we are still lower than the previous peak suggesting we wait until next week for clarity. However, a bit of caution to overly aggressive equity exposure is certainly warranted.I say this for a couple of reasons.

- The market has had a stellar run since the beginning of the year and while earnings season is giving a “bid” to stocks currently, both current and forecast earnings continue to weaken.

- We are at the end of the seasonally strong period for stocks and given the outsized run since the beginning of the year a decent mid-year correction is not only normal, but should be anticipated.

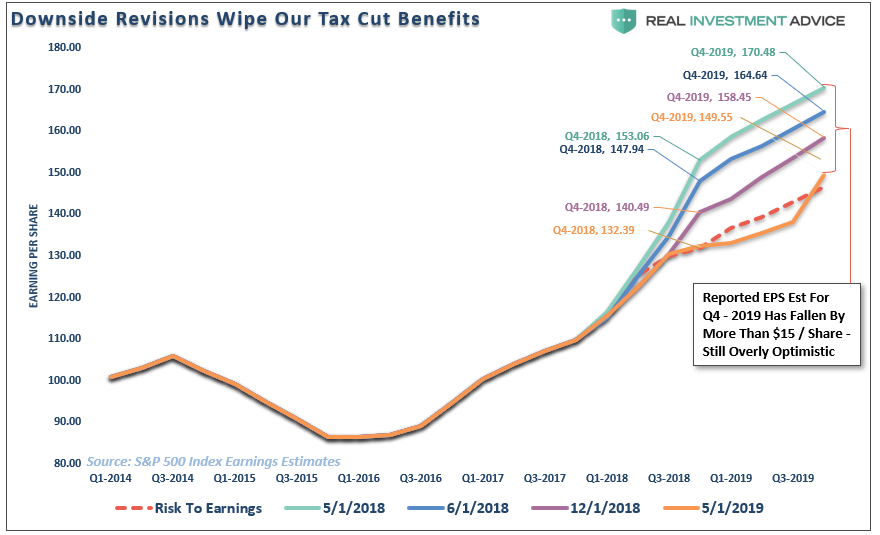

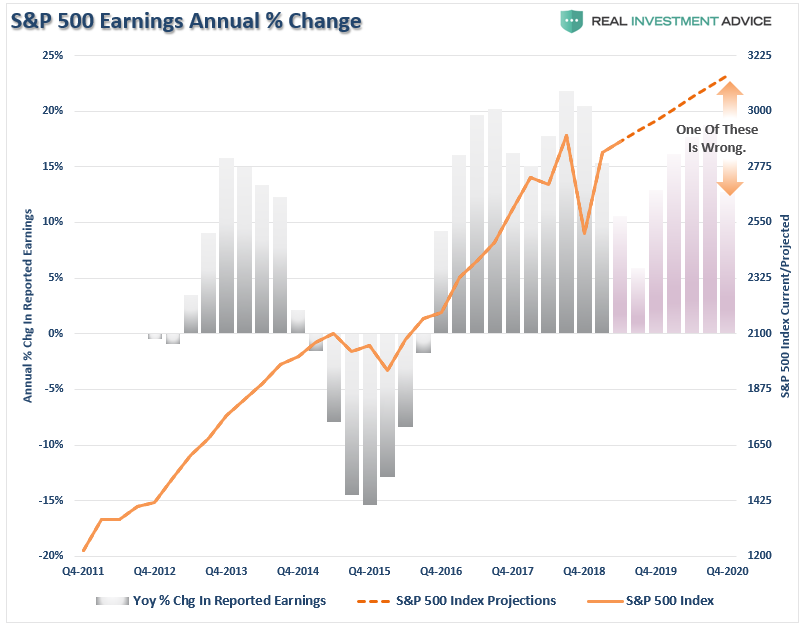

With respect to earnings, and as we have stated many times previously, estimates continue to be revised lower, and have now exceed our original revision target (red dashed line) set out in early 2018.

Note: The Q4-2019 hockey-stick earnings jump WILL BE revised down markedly over the next few months.

Why do I say that?

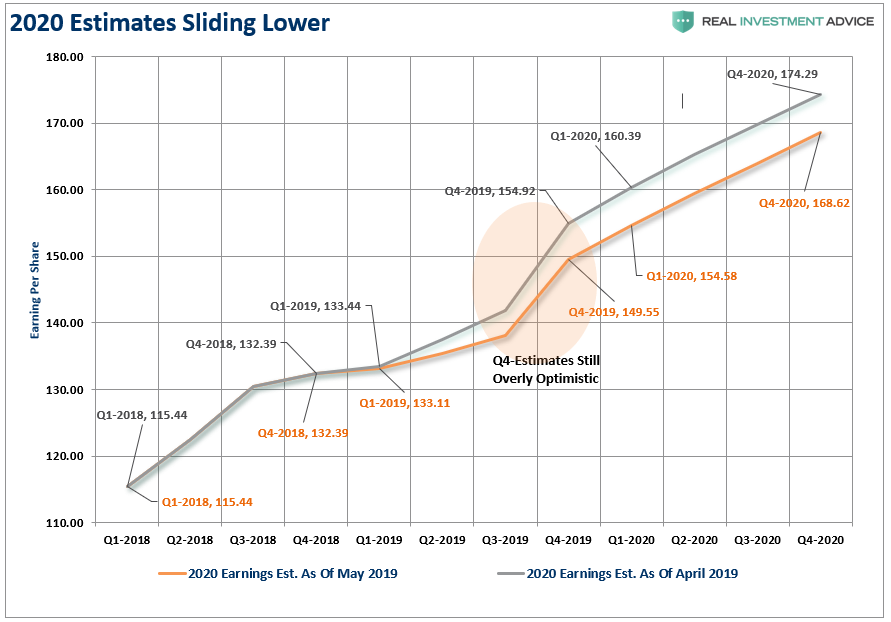

Because 2020 estimates are already being revised down rather sharply as well.

This is important as markets push all-time highs at a time when forward earnings estimates for the next 18-months are all lower than previously estimated. Despite the rise in expected earnings in 2020, the peaks of those expectations (which are predictably about 33% too high currently) are all lower than the 2018 earnings peaks.

In other words, further increases in the markets over the next two years will be a function of multiple expansion rather than increased “value.”

Such an environment tells us a few things about the market.

- In the short-term prices will be driven by momentum and optimism. (1-3 months)

- Over the intermediate-term prices will become more subject to higher volatility due to potential disappointments as “bad news” is treated as “bad news” (4-9 months)

- Longer-term the market is simply a weighing machine and current expectations of 8% annual growth rates in asset prices will be realigned with weaker earnings prospects (10-24 months)

As noted above, the market’s stellar run is set for a breather over the next couple of months. Specifically, as we approach the end of the seasonally strong period, the odds of a “reset” rise markedly. As noted on Thursday by StockTraders Almanac the seasonal “sell” signal has also been triggered. To wit:

“Yesterday after the market closed, we sent out our Tactical Seasonal Switching Strategy Sell Alert for DJIA and S&P 500…we are shifting the ETF Portfolio to a market-neutral position by adding some exposure to short and longer duration bonds.”