Written by Lance Roberts, Clarity Financial

On Friday, the first estimate of Q1 GDP report was much stronger than expected coming in at 3.2% versus estimates of 2.3%.

Please share this article – Go to very top of page, right hand side, for social media buttons.

There are a couple of important takeaways from the report:

- The first estimate is simply a collection of economists estimates as most of the data for the first quarter has not been fully compiled yet. This suggests the next two estimates will likely be revised lower due to some of the recent softness in data we have seen.

- Almost 50% of the increase in GDP came from slower imports and a massive surge in inventories which suggests slower consumer consumption which comprises roughly 70% of economic growth. (In other words, future GDP reports will also likely be weaker. (Net Trade and Inventories was 1.68% of the 3.2% rise.)

- Had CPI been used rather than the BEA’s more questionable measure of “inflation,” GDP in the first quarter would have been just 1.56% which is more aligned with the actual activity seen in the first quarter.

- This puts the Federal Reserve in a very tough position of NOT raising rates further and eliminates any possibility of a reduction in the Fed’s balance sheet.

- Lastly, bonds yields should have surged on this number suggesting a much strong economic growth rate. However, yields fell on Friday signaling that investors are continuing to question both economic growth and the market rally.

“But…the global slowdown is temporary.”

The expectation of an economic recovery to support the continuation of the bull market is likely misplaced for several reasons.

- The Fed rate hikes that were done in 2018 are still working their way through the economy, Higher rates are impacting economically sensitive sectors like autos, housing, and manufacturing.

- Economic growth globally remains weak and is impacting growth in the U.S.

- Interest rates, and the yield curve, despite stocks hitting “all-time” highs are suggesting that economic weakness is likely more pervasive than currently believed.

- The rising trend of the U.S. dollar will impact exports which makes up between 40-50% corporate profits.

- Imports continue to suggest the U.S. consumer, 70% of the economy, is weaker than headlines suggest.

- Rising oil prices, and gasoline prices, are a tax on consumers and will further impair economic growth.

- Deflation is a rising concern.

- There is no massive slate of natural disasters to pull forward consumption or boost manufacturing, construction or commodity demand.

- While deficit spending is certainly supportive of growth, with the deficit already at $1.2 trillion, the rate of change in deficit spending will not be supportive of stronger economic growth.

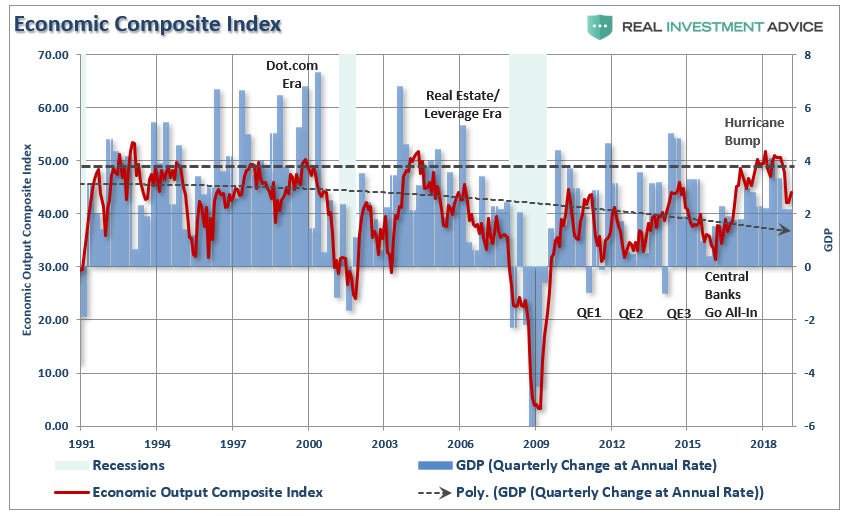

The RIA economic composite index (a broad composite of hard, soft, and leading indicators and surveys) has turned lower. Historically, turns from high levels (dashed black line) tend to revert to the lower bound suggesting more economic weakness is likely in the quarters ahead.

Oh…you are just being bearish.

Maybe, but as I stated in Q2 of 2018:

“The deterioration in earnings is something worth watching closely. While earnings have improved in the recent quarter, due to the benefit of tax cuts, it is likely transient given the late stage of the current economic cycle, continued strength in the dollar and potentially weaker commodity prices in the future. Wall Street is notorious for missing the major turning of the markets and leaving investors scrambling for the exits.

Of course, no one on Wall Street told you to be wary of the markets in 2018. While we did, it largely fell on deaf ears.

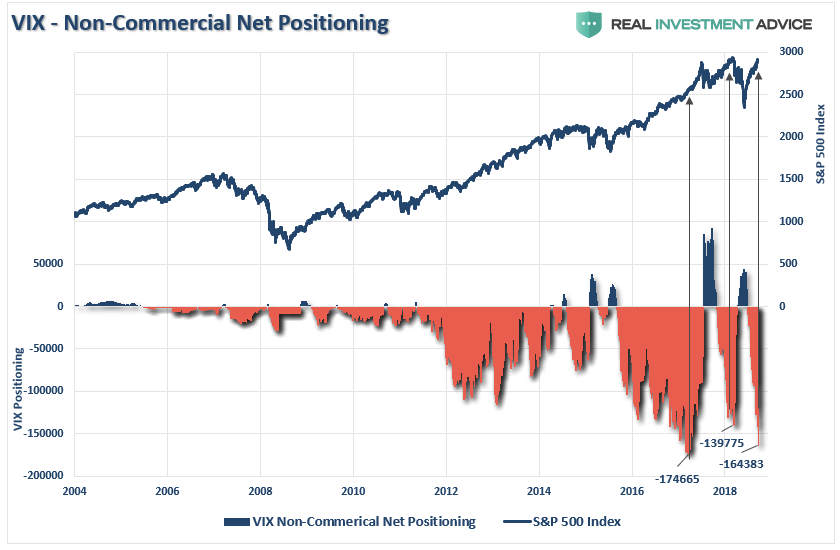

Currently, there is “no perceived risk” in the markets as represented by the second highest levels of VIX shorts on record.

However, “risk” is like grabbing the tail of a rattlesnake. Nothing happens at first, but it can whip around and bite you faster than you can imagine.

See you next week.