Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

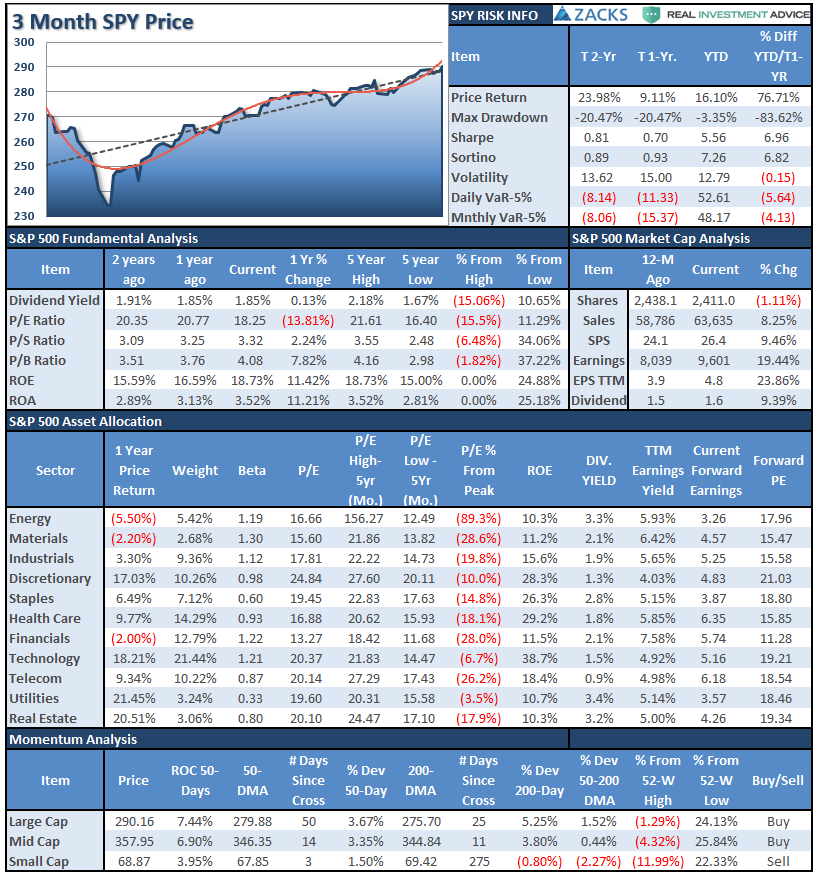

S&P 500 Tear Sheet

Performance Analysis

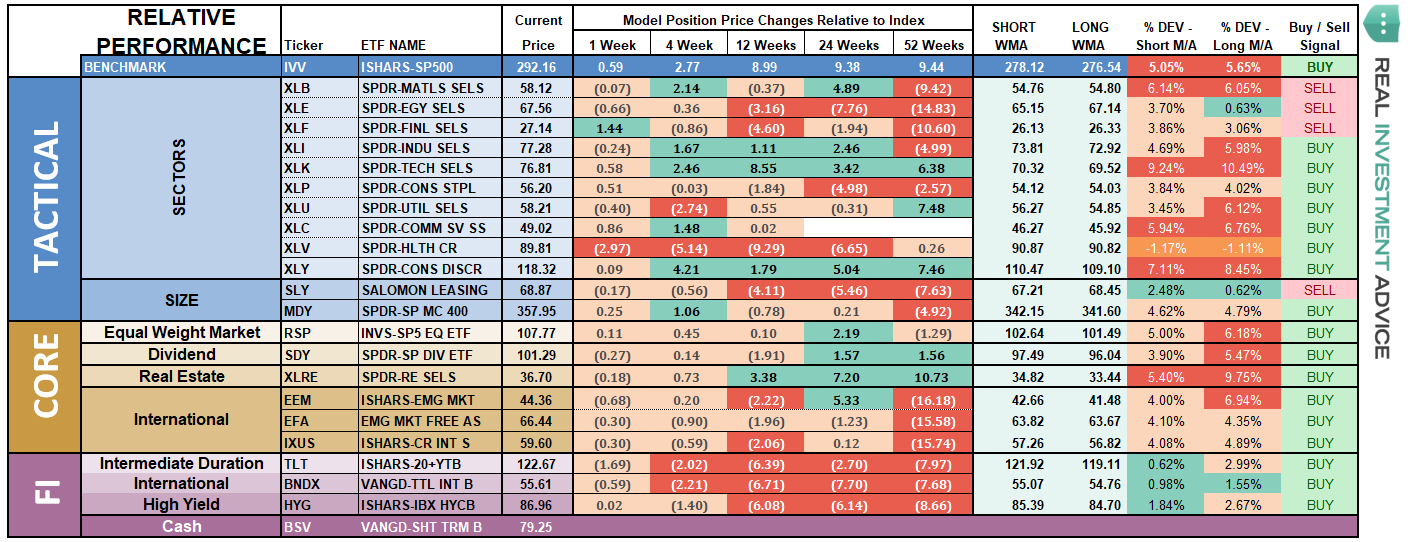

ETF Model Relative Performance Analysis

Sector & Market Analysis:

Be sure and catch our updates on Major Markets (Monday) and Major Sectors (Tuesday) with updated buy/stop/sell levels

Sector-by-Sector

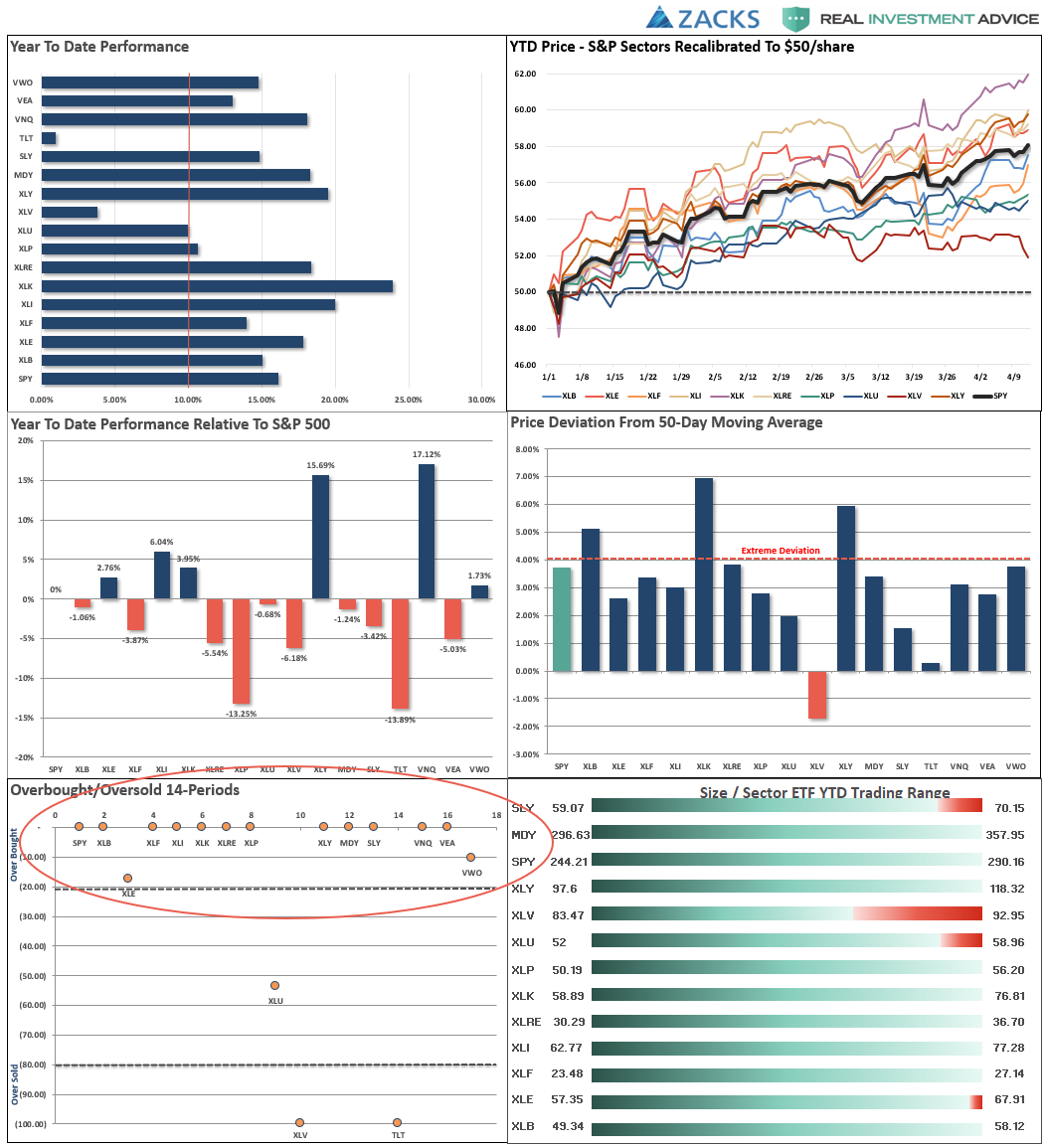

Looking at sectors on a “relative performance” basis to the S&P 500 we have seen some rotations in leadership over the last week.

Improving – Energy, Materials

With the pick up in oil prices, the Energy sector has performed better as of late. Last week, energy finally broke above its 200-dma but is still lagging many other sectors of the market. Current, with oil prices very overbought, look for a pullback in energy shares soon. Take profits for now, and if the sector can hold support we can increase our holdings accordingly. Materials have surged over the last couple of weeks on hopes of a “trade war” resolution. With the sector extremely overbought, take profits, rebalance risk, and tighten up stops.

Current Positions: 1/2 Position in XLE, XLB

Outperforming – Technology, Industrials, Discretionary

Discretionary and Technology broke out to new all-time highs last week, and continue to push higher this past week as well. While participation continues to become more concentrated in a smaller number of sectors, the bullish bias persists for now with 50-dma’s above 200-dma’s and momentum trending positively. These sectors are all overbought, so take some profits, rebalance portfolios, raise stops but remain long for now

Current Positions: XLI, XLY, XLK – Stops moved from 200 to 50-dma’s.

Weakening – Real Estate, Utilities, Communications

Despite the “bullish” bias, the more defensive sectors of the markets, namely Utilities and Real Estate, have continued to attract buyers. While Utilities recently corrected a small bit, Real Estate has not. Both sectors remain very extended and overbought. Communications has become much more bullishly biased as of late after successfully testing its 200-dma and the 50-dma crossing above the 200-dma. With the sector extremely overbought look for a correction which does not violate support to add to portfolios.

Current Position: XLU

Lagging – Healthcare, Staples, Financials

Staples recently had a very small correction which was not enough to resolve its overbought condition. However, Staples are testing previous highs as money continues to chase defensive sectors of the market. Financials, which has been struggling as of late due to the inversion of the yield curve, perked up this past week and finally broke out of its consolidation with better than expected earnings from JPM on Friday. With the performance of Financials is improving, it may attract more buyers over the next couple of weeks as it has underperformed the bulk of the rally from the December lows. Healthcare continues to struggle with repeated calls from political candidates for “Government sponsored health care.” This is very unlikely to happen, and Healthcare is likely setting up to gain from a rotation from offense to defense in the market. This is the only sector that oversold and currently sitting on support.

Current Positions: XLF, XLV, XLP

Market By Market

Small-Cap and Mid Cap – Small Cap stocks continue to lag the rest of the market and remain confined within the context of a broader downtrend. While small caps are challenging their 200-dma, a break above that level will make small-caps are more compelling play. Conversely, Mid-Caps are performing much better as of late and have broken out of its consolidation over the last couple of months. With the 50-dma crossing above the 200-dma, look for a pullback towards the 50-dma to increase exposure to Mid-caps.

Current Position: None

Emerging, International & Total International Markets

Emerging Markets continue to perform better as of late but are extremely overbought in the short-term. We are looking for a pullback which holds support to increase our holdings in that market.

Major International & Total International shares also are performing much better despite global economic weakness. This is probably misplaced optimism but nonetheless the technical backdrop has improved enough to warrant adding a position on a pullback that holds support and works off some of the extreme overbought condition.

Stops should remain tight at the running 50-dma which is also previous support.

Current Position: 1/2 position in EEM

Dividends, Market, and Equal Weight – These positions are our long-term “core” positions for the portfolio given that over the long-term markets do rise with respect to economic growth and inflation. Currently, the short-term bullish trend is positive and our core positions are providing the “base” around which we overweight/underweight our allocations based on our outlook.

Core holdings remain currently at target portfolio weights but all three of our core positions are grossly overbought. A correction is coming, it is now just a function of time.

Current Position: RSP, VYM, IVV

Gold – Gold continues to perform poorly despite concerns over the Fed, policy, and monetary policy. With gold building a bearish wedge below the 50-dma, the critical support level of $121 must be honored. Gold is very oversold in the short-term so any market sell-off in the next week will likely see gold bounce. Gold must get above $123.50 to make an attempt at higher levels.

Current Position: GDX (Gold Miners), IAU (Gold)

Bonds –

The 10-year treasury popped up to 2.54% on Friday on rising inflationary pressures in recent reports. This is going to put the Fed into a very uncomfortable position of not raising the Fed Funds rate if prices and wages continue to advance. However, rates are simply bouncing back from a very oversold condition after the plunge from last November. This is setting up a very nice entry point to add additional bond exposure in the months ahead as we move into the summer months. Look for rates to touch 2.6% as a point to begin adding exposure to portfolios. There is a potential for rates to climb as high as 2.85%, but that move is quite unlikely in the current economic environment.

Current Positions: DBLTX, SHY, TFLO, GSY

High Yield Bonds, representative of the “risk on” chase for the markets, have continued to rally this past week and are now egregiously overbought. Take profits and rebalance risk accordingly. International bonds, which are also high credit risk, have been consolidating over the last couple of weeks, but remain very overbought currently which doesn’t over a high reward/risk entry point.

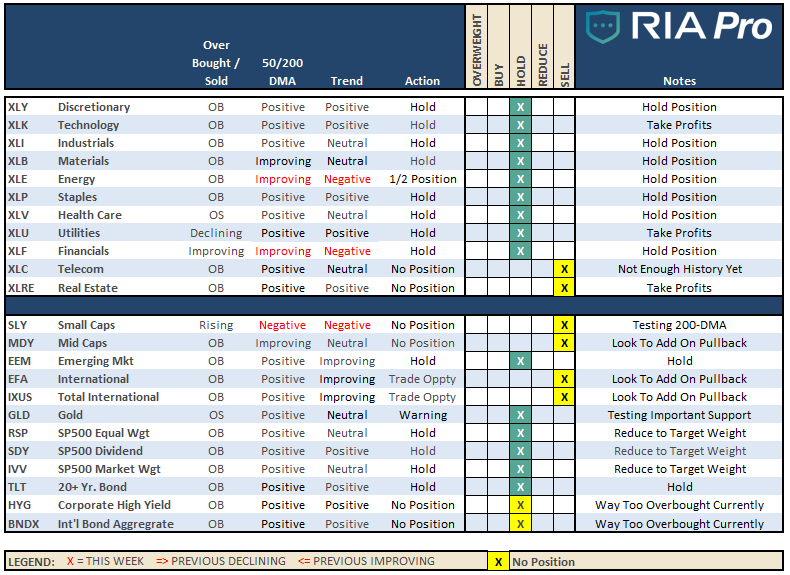

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

No actions this past week were needed.

As we noted last week, there is currently little concern about the markets despite economic weakness popping up just about everywhere. For now, the market remains glued to headlines on trade, China stimulus, and the Fed. This will turn out to be ill-advised in the months ahead, but for now it remains “Party on Garth.”

With our near term buy signals in place, we continue to let our equity holdings ride the wave of the market and are looking to opportunistically take on opportunities as they present themselves. With earnings season now underway there will be bid under stocks as companies “beat” drastically lowered “expectations.”

So, for now, we are patient.

- New clients: We continue to onboard clients and move into specified models accordingly.

- Equity Model: We rebalanced all positions in the portfolio, with the exception of Boeing (BA), reducing overweight positions and adding to underweight positions.

- ETF Model: No changes. – Reviewing for rebalancing as needed.

Note for new clients:

It is important to understand that when we add to our equity allocations, ALL purchases are initially “trades” that can, and will, be closed out quickly if they fail to work as anticipated. This is why we “step” into positions initially. Once a “trade” begins to work as anticipated, it is then brought to the appropriate portfolio weight and becomes a long-term investment. We will unwind these actions either by reducing, selling, or hedging, if the market environment changes for the worse.