Written by Investing.com Staff, Investing.com

U.S. stocks lower at close of trade; Dow Jones Industrial Average down 0.09%

U.S. stocks were lower after the close on Friday, as losses in the Oil & Gas, Consumer Services and Healthcare sectors led shares lower.

At the close in NYSE, the Dow Jones Industrial Average fell 0.09%, while the S&P 500 index declined 0.21%, and the NASDAQ Composite index fell 0.18%.

Please share this article – Go to very top of page, right hand side for social media buttons.

The best performers of the session on the Dow Jones Industrial Average wereGoldman Sachs Group Inc (NYSE:GS), which rose 1.28% or 2.47 points to trade at 195.24 at the close. Meanwhile, UnitedHealth Group Incorporated (NYSE:UNH) added 0.63% or 1.49 points to end at 237.29 and 3M Company (NYSE:MMM) was up 0.52% or 1.03 points to 200.89 in late trade.

The worst performers of the session were Exxon Mobil Corp (NYSE:XOM), which fell 1.43% or 1.15 points to trade at 79.01 at the close. Pfizer Inc (NYSE:PFE) declined 1.21% or 0.50 points to end at 40.89 and Caterpillar Inc (NYSE:CAT) was down 1.09% or 1.45 points to 131.35.

The top performers on the S&P 500 were Costco Wholesale Corporation (NASDAQ:COST) which rose 5.09% to 227.82, H&R Block Inc (NYSE:HRB) which was up 3.27% to settle at 24.95 and Seagate Technology PLC (NASDAQ:STX) which gained 2.28% to close at 46.22.

The worst performers were Chesapeake Energy Corporation (NYSE:CHK) which was down 8.08% to 2.730 in late trade, Noble Energy Inc (NYSE:NBL) which lost 5.39% to settle at 21.42 and EOG Resources Inc (NYSE:EOG) which was down 5.37% to 86.44 at the close.

The top performers on the NASDAQ Composite were AquaBounty Technologies Inc(NASDAQ:AQB) which rose 118.30% to 4.890, Pulmatrix Inc (NASDAQ:PULM) which was up 39.37% to settle at 1.770 and Alliqua BioMedical Inc (NASDAQ:ALQA) which gained 35.91% to close at 3.520.

The worst performers were Bio Path Holdings Inc (NASDAQ:BPTH) which was down 45.96% to 21.000 in late trade, CHF Solutions Inc (NASDAQ:CHFS) which lost 45.57% to settle at 4.300 and Altimmune Inc (NASDAQ:ALT) which was down 36.56% to 2.880 at the close.

Falling stocks outnumbered advancing ones on the New York Stock Exchange by 1652 to 1304 and 133 ended unchanged; on the Nasdaq Stock Exchange, 1399 fell and 1225 advanced, while 96 ended unchanged.

Shares in AquaBounty Technologies Inc (NASDAQ:AQB) rose to 52-week highs; gaining 118.30% or 2.650 to 4.890. Shares in CHF Solutions Inc (NASDAQ:CHFS) fell to 3-years lows; falling 45.57% or 3.600 to 4.300. Shares in Alliqua BioMedical Inc (NASDAQ:ALQA) rose to 52-week highs; up 35.91% or 0.930 to 3.520.

The CBOE Volatility Index, which measures the implied volatility of S&P 500 options, was up 7.65% to 16.05.

Gold Futures for April delivery was up 0.98% or 12.65 to $1298.75 a troy ounce. Elsewhere in commodities trading, Crude oil for delivery in April fell 1.11% or 0.63 to hit $56.03 a barrel, while the May Brent oil contract fell 0.92% or 0.61 to trade at $65.69 a barrel.

EUR/USD was up 0.05% to 1.1243, while USD/JPY fell 0.36% to 111.17.

The US Dollar Index Futures was down 0.31% at 97.322.

See also:

Stocks – Dow’s Late-Stage Rally Falls Short Amid Slump in U.S. Job Gains

Canada stocks lower at close of trade; S&P/TSX Composite down 0.38%

U.K. stocks lower at close of trade; Investing.com United Kingdom 100 down 0.76%

Wall Street extends losing streak after weak U.S. jobs data (Reuters)

The U.S. dollar fell against its rivals on Friday as investors digested a mixed labor market report showing a surprising slump in job gains for February.

The slump was so surprising that White House economic advisor Larry Kudlow dismissed it as “very fluky” and said no one should pay attention to it.

U.S. dollar index, which measures the green against a trade-weighted basket of six major currencies, fell by 0.34% to 97.29. The greenback, however, is set to post a weekly gain following a rally in the previous session.

Nonfarm payrolls rose by just 20,000 compared to expectations for a 181,000 gain, according to economists surveyed by Investing.com. That was the smallest gain since September 2017.

The unemployment rate fell to 3.8%, while average hourly earnings, an important number to gauge inflation, rose 3.4% year over year in February.

The plunge in job gains was largely downplayed by Wall Street, with many citing weather-related disruption as one the main headwinds.

High Frequency Economics said that the slowing may reflect “some moderation” in the trend, but much of decline was likely caused by “weather effects“.

“While the three-month average of job gains is a still-healthy 186,000, that is below what has been a 200K-plus trend. The trend likely remains more than strong enough to keep the unemployment rate trending down over time.”

On the housing front, The Commerce Department said U.S. housing starts surged 18.6% to a seasonally adjusted annual rate of 1.23 million units in January, well above the Investing.com estimate for a 15% rise above 10%.

A plunge in the pound, meanwhile, kept a lid on losses in the greenback after EU chief Brexit negotiator Michel Barnier detailed a proposal that would have allowed the U.K. to unilaterally exit the Irish backstop, as long as Northern Ireland remain inside it.

The proposal is likely to be rejected by Prime Minister Theresa May because it could potentially lead to Northern Ireland being annexed by Ireland from the U.K.

With little sign that May will be able to secure a material change to the Irish backstop issue, many expect the prime minister’s withdrawal agreement to be voted down next week.

GBP/USD fell 0.62% to $1.3004, while EUR/USD rose 0.45% to $1.1243.

USD/CAD fell 0.37% to C$1.3404, while USD/JPY lost 0.43% to Y111.11.

See also:

- Forex – U.S. Dollar Falls as Job Growth Numbers Disappoint

- U.S. net long dollars hit highest since late December: CFTC, Reuters

The naysayers had all but written off gold’s chances for a rebound. But it took just one dismal U.S. jobs report to prove them wrong.

The spot price of bullion, as well as futures of gold, breached the magical $1,300 mark on Friday after the Labor Department reported growth of just around 20,000 jobs for February versus market expectations for 181,000 new positions.

Gold futures for April delivery hit a one-week high of $1,301.25 per ounce on the Comex division of the New York Mercantile Exchange. It settled at $1,299.30, up $13.20, or 1%, on the day.

Spot gold, reflective of trades in physical bullion, also hit a one-week peak in intraday trade, reaching $1,300.80 before consolidating to $1,299.28 by 2:30 PM (19:30 GMT), up $13.65, or 1%, on the day.

U.S. jobs data aside, gold also saw a surfeit of safe-haven buying on renewed worries about economic growth in Europe and China.

European Central Bank President Mario Draghi said eurozone economies were in “a period of continued weakness and pervasive uncertainty“.

China’s dollar-denominated February exports, meanwhile, fell 21% percent from a year earlier, representing the biggest drop in three years. The world’s second-largest economy also suffered a 5.2% drop in imports last month.

Gold hit 10-month peaks just shy of 1,350 an ounce on Feb. 20, a month after getting to the $1,300 level. It fell under that critical price point last Friday after a heightened rally in the dollar index, which measures the greenback against a basket of six currencies. In the latest session, the dollar fell 0.4% to 97.28, from the previous session’s three-month highs of 97.67.

“We favor looking for bearish setups on the dollar against gold and silver, given the renewed weaknesses in government bond yields” after the U.S. jobs data and combined dreary outlooks for Europe and China, said Fawad Razaqzada, a London-based analyst for forex.com.

Palladium prices fell on Friday but retained its standing as the world’s costliest metal due to its wide premium against gold.

The spot price of palladium slid by 14.40, or 0.9%, to 1,512.80 per ounce by 2:30 PM. Spot palladium hit a record high of $1,569.40 last week on fears of short supply.

Trades in other Comex metals as of 2:30 PM ET (19:30 GMT):

Palladium futures down $13.95, or 0.1%, at $1,468.45 per ounce.

Platinum futures up $1.35 or 0.2%, at $818.45 per ounce.

Silver futures up 31 cents, or 2.1%, at $15.35 per ounce.

Copper futures down 1 cent, or 0.4%, at $2.90 per pound.

See also:

- Gold, Silver, Precious Metals Miners ETFs Climb (ETF Trends)

- Gold futures settle with a 1% gain, up a dime for the week (MarketWatch)

Squeezing the supply of a commodity can make buyers pay more for it, but not necessarily want more of it. The oil market is learning that.

Crude oil prices settled down about 1% on Friday after the European Central Bank signaled more economic troubles in the region and U.S. jobs data showed labor market growth virtually grinding to a halt in February. Combined with a Chinese economy growing at its slowest pace in nearly 30 years and unable to end trade hostilities with the U.S. after multiple talks, the prospects for new oil demand were at best restrained.

New York-traded West Texas Intermediate crude settled down 59 cents, or 1%, at $56.07 per barrel after tumbling more than 2% earlier. The U.S. crude benchmark has struggled to establish clear direction since a slide of nearly 3% last Friday, ending the current week up by just 0.5%

Brent, the global oil benchmark, was down 53 cents, or 0.8%, at $66.10 per barrel by 2:40 PM ET (19:40 GMT). For the week, it rose 1%.

Since the start of March, the rally in oil has made little headway, a stark contrast to the gains of more than 20% in WTI and Brent through February that came from hefty production cuts by the OPEC+ alliance of 25 oil producing countries.

Platts reported on Friday that Saudi Arabia pumped 10.1 million barrels per day of crude in February in yet another sign that OPEC’s largest producer and de facto leader was cutting more than pledged under the OPEC+ production deal that began in January.

Friday’s selloff was triggered by remarks from ECB President Mario Draghi, who said eurozone economies were in “a period of continued weakness and pervasive uncertainty.”

U.S. jobs data for February showed the creation of only about 20,000 jobs versus market expectations for 181,000 new positions.

Chinese economic data, meanwhile, threw up conflicting statistics.

According to reports, dollar-denominated February exports in the world’s second-largest economy fell 21% from a year earlier, representing the biggest drop in three years amid a drop of 5.2% in imports.

While oil demand in China has so far held up with crude imports staying above 10 million bpd, the slowdown in economic growth is likely to dent fuel consumption and pressure prices, reports show.

New York-based Energy Intelligence said in its weekly newsletter:

“The market remains heavily focused on macro events such as trade talks between the U.S. and China, since deteriorating ties could hurt global economic growth and have a knock-on effect on oil demand. In fact, securing a trade deal is seen as critical to supporting investor confidence across asset classes this year.”

To counter OPEC cuts, U.S. oil production is reaching new highs, with output already above 12 million bpd and racing toward the next target of 13 million bpd, according to the U.S. Energy Information Administration.

Last, but not least, Norway’s trillion-dollar sovereign wealth fund, the world’s biggest, announced on Friday it will sell stakes in oil and gas explorers and producers, adding to the dour mood across the energy sector.

See also:

- Crude Oil Forecast: 2019 Recovery at Risk as Near-Term Range Buckles (Dailyfx)

- Rig Count Slides As U.S. Oil Output Remains At All-Time High (OilPrice.com)

Natural Gas (Hellenic Shipping News)

EIA estimates that between 2014 and 2017 natural gas processing capacity and processing throughput increased by about 5% on a net basis in the Lower 48 states, even as the number of individual plants declined. Natural gas processing plant utilization rates stayed constant at 66% from 2014 to 2017, but several states experienced significant changes, largely reflecting changes in natural gas production across regions.

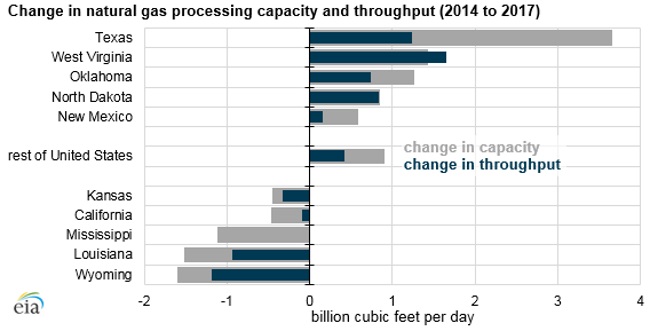

Processing plants are midstream facilities that separate natural gas liquids (NGL) from natural gas. Some natural gas processing plants remove water and other contaminants from the raw natural gas stream and separate NGL streams into component products. EIA’s triennial EIA-757 Schedule A, Natural Gas Processing Plant Survey, tracks the country’s population of natural gas plants. EIA recently published 2017 data and an accompanying analysis that provide state-level summaries of total capacity, throughput, heat content, and utilization of all processing plants in the Lower 48 states. The accompanying analysis also compares this data with 2014 levels, the last time the survey data were collected.

Source: U.S. Energy Information Administration, Form EIA-757 Schedule A, Natural Gas Processing Plant Survey

As of the end of 2017, 510 active natural gas processing plants were active in the Lower 48 states with a total processing capacity of 80.8 billion cubic feet per day (Bcf/d). On average, these plants processed about 53.3 Bcf/d, operating at about 66% of capacity. Plants operate at less than full capacity for many reasons: transportation constraints, varying production volumes and characteristics, and regional economics.

Source: U.S. Energy Information Administration, Form EIA-757 Schedule A, Natural Gas Processing Plant Survey

Regions with increased natural gas production, such as Texas (Permian, Eagle Ford), West Virginia (Marcellus, Utica), and North Dakota (Bakken), showed the largest increase in natural gas processing capacity and throughput between 2014 and 2017. In West Virgina, increases in the utilization of existing plants led to an increase in throughput from 2014 to 2017 that exceeded its increase in processing capacity.

At the national level, utilization rates remained essentially flat between 2014 and 2017, although some states showed more significant changes. In the Bakken region – Montana and North Dakota – both utilization rates and capacity increased, alongside increases in natural gas production. Similarly, Ohio and West Virginia, in the Appalachian Basin in the Northeast, also showed large increases in capacity and utilization.

However, in states such as Texas and Oklahoma, processing capacity grew more than throughput, resulting in slightly lower utilization in those states. Texas’s lower utilization rate may be partly attributed to the state’s natural gas production decline between 2014 and 2017.

Source: EIA

.