by Lee Adler, Wall Street Examiner

The Primary Dealers are the trading and market making behemoths who are tasked and privileged by the Fed with being the Fed’s sole counterparty in conducting monetary policy operations. They are also the Primary Dealers for the US Treasury when the Treasury sells debt to the public, which it does almost every day now. Today those debt sales average more than $100 billion in new money per month.

Please share this article – Go to very top of page, right hand side, for social media buttons.

It can be a big source of profits for the dealers. It can also be a doomsday machine. Here’s how.

Dealers Trade for Their Own Accounts, and They Are Sometimes Wrong

The dealers act on behalf of investors, and sometimes other central banks. They also accumulate long and short positions for their own trading purposes. Obviously the purpose of building and holding those inventories is to make profits by buying low and selling high, or selling short high and covering low.

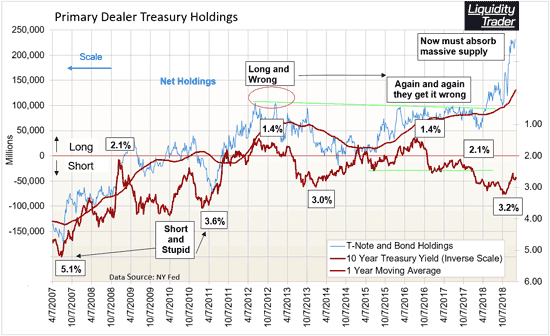

In July and August of 2007, the Primary Dealers had built up the largest short position in Treasury notes and bonds in their history. Notes and bonds are the Federal Governments debt securities of more than one year and up to 30 years duration. The dealers were making a huge one way bet that the price of the Treasuries would fall, and that yields would rise, and that they could cover their inventory of bonds sold short at a profit.

They were wrong. From that very moment, July 2007, bond prices rose, and yields fell relentlessly. The 10 year Treasury yield fell from 5.1% to 2.1% over the next 17 months. The dealers suffered massive losses and were repeatedly in the position of being unable to maintain orderly markets in both stocks and bonds. They weren’t just on the ropes, they were down for the count.

It all culminated in a stock market crash and bond market meltup in September and October of 2008. The whole financial world was melting down, and virtually every investor on earth wanted to hold US Treasury securities as a safe haven.

When Dealers Are Wrong The Markets, and YOU, Pay the Price

While the financial media and economists blame something called the Lehman Moment for the crash, there almost certainly would have been no crash were the dealers not so badly mispositioned. The Fed would not have needed to bail out the dealers with QE. There would have been no buying panic in the Treasury market because much of that panic was fueled by the dealers covering their shorts. It was probably the greatest short squeeze in history.

The dealers were dead meat. The markets were in turmoil, until in March 2009, the Fed finally stopped fiddling around with alphabet soup rescue programs that didn’t work. It realized that it would need to massively infuse cash into the dealers through the purchases of hundreds of billions of Treasuries with the dealers as intermediaries. In effect, the Fed finally woke up to the fact that to save the markets, it needed to rescue the entire Primary Dealer system.

These Masters of the Universe, the smartest of the smart money, were so smart they essentially destroyed any semblance of free financial markets for good. The rescue of the dealers through QE has become a permanent Fed put that insures that they will never again be faced with going broke, and ostensibly guarantees that there will never again be a panic that threatens to bring down the system.

Any thought that Chairman Powell was willing to reintroduce the concept of risk to the market was delusional thinking on my part.

But does the permanent Fed put really succeed in removing risk from the system? Not based on what we see in the positions of the Primary Dealers today.

The dealers historically had always carried a small net short position in Treasuries to facilitate trading of “when-issued” bonds. But since 2011, they have been building an ever-growing net long position. The size of those positions has soared into the stratosphere over the past 3 months as Treasury issuance has gone through the roof. If ever there was a time when the term “off the charts,” applied, this is it.

It appears to be a kind of forced march under the onslaught of the massive supply increase. But maybe it’s a forced march of the willing, making another massive one way bet on the market. It’s a bet that could be wrong. I think that it’s likely to be wrong, as it already has been.

Dealers Are Positioned Wrong Again So History Could Repeat

As the dealers built these long positions, since June 2016 when the 10 year yield hit 1.4%, the bond market has relentlessly trended against them. Early last year I warned my Liquidity Trader subscribers that Primary Dealer trading losses would pressure big bank profits. That came to pass year as the 10 year yield soared past 3% from April to October. The bank stocks went into a bear market for most of the year, until reaching a bottom of sorts in December. It was far worse than what the broader market was experiencing through 2018.

Only in the past 3 months as dealer buying soared, have the dealers gotten a reprieve, with rising bond prices and falling yields. But if supply and demand matter, this reprieve will prove short lived.

The selloff in stocks in the fourth quarter triggered and helped to fund a buying panic in bonds, as some capital rotated from stocks to bonds. But as stocks rallied after Christmas, the bond rally stalled.

If bonds now begin to sell off, this massive inventory could become a massive problem for the dealers and hence for the markets. Yes, they are largely hedged, but they hedges are not perfect. In my current Liquidity Trader report, I calculated that the dealers held $188 billion in net long positions.

That’s a time bomb, and it could have a short fuse. With ever more Treasury supply in the pipeline, the dealers will never be able to materially reduce the size of these positions. Nor will they be able to lay off all the risk by hedging with futures. Furthermore, these Treasury purchases have been financed with debt. Lots and lots of debt.

Unlike the “old days” under QE, the Fed isn’t backstopping these purchases by financing them indirectly with MBS purchases, or buying them outright the following week. The dealers have borrowed the money to buy this paper. They are backed by a kind of debt financing called “repo” that is similar to what you would know as margin. But it’s not 50% margin. It’s far higher, as much as 90%.

This is an accident waiting to happen.

In short, the dealers are getting longer and longer when the fundamentals of supply and demand suggest that bond yields will rise and prices will fall. Supply will remain extremely heavy as far as the eye can see under the weight of gigantic Federal Budget deficits that aren’t going away any time soon.

And demand is weakened the Fed draining money from the banking system under its balance sheet normalization program. While the Fed is talking about setting a schedule to end the program, that’s a long way from them restarting the QE that underpinned the final years of the bond bull. Once they stopped QE, the bond bull market also stopped.

Primary Dealer mispositioning is a huge risk. It was the lynchpin of the 2008 crash. This current lopsided long position is far bigger than the short position was in 2008 when the market went against them.

This could once again lead to a catastrophic unwinding that would render the dealers unable to maintain orderly markets in bonds and stocks, just as in 2008.

The kind of leverage that the dealers use to finance these positions kills quickly when the market goes against your positions. When dealers are highly leveraged and mispositioned, it has the potential to kill not just the dealers holding those leveraged positions, but the financial markets in general. If the bond market goes the wrong way, the dealers will simply be unable to make markets. At that point the question will become how quickly the Fed reacts, whether it will react in sufficient size to make a difference, and finally whether market participants will have sufficient confidence in those actions to start buying in size.

We Face a Binary Choice

The market faces a binary choice and consequently, so do we. Bond yields must fall and bond prices must rise for dealers to remain profitable and able to maintain orderly markets. If bond prices start falling and yields start rising, we face a disorderly denouement.

We must wonder if the Big Three central banks are up to the task of rescuing the dealers one more time, and moreover, if the market will respond as the central banks want. I think that we are on the road to finding out. That’s why I continue to recommend holding only short term T-bills until it becomes clear that these risks have been mitigated successfully.

Meanwhile, there are solutions for profiting from these treacherous markets.

.