Written by Lance Roberts, Clarity Financial

On Friday, I discussed the market surge on Wednesday following comments from Fed Chair Jerome Powell:

Please share this article – Go to very top of page, right hand side, for social media buttons.

“All it took was two 10% stock market corrections in a single year and some heavy ‘browbeating’ from President Trump to reverse Jerome Powell’s hawkish stance on hiking interest rates.

On Wednesday, Powell took to the microphone to give the markets what they have been longing for – the ‘Powell Put.’ During his speech, Powell took to a different tone than seen previously and specifically when he stated that current rates are ‘just below’ the range of estimates for a ‘neutral rate.’ This is a sharply different tone than seen previously when he suggested that a ‘neutral rate was still a long way off.’

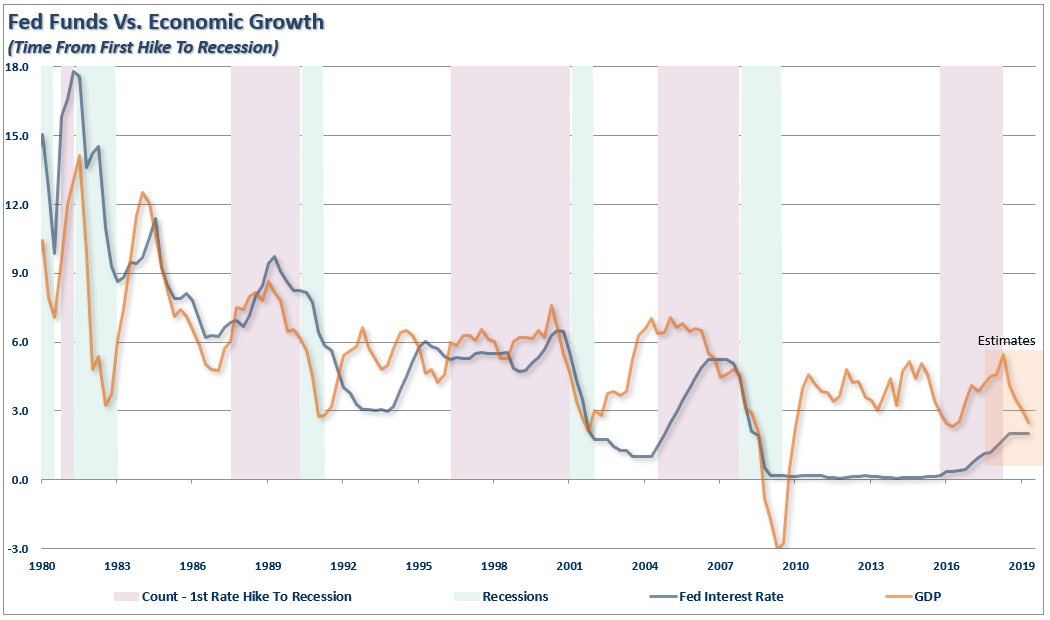

Importantly, while the market surged higher after the comments on the suggestion the Fed was close to ‘being done’ hiking rates, it also suggests the outlook for inflation and economic growth has fallen. With the Fed Funds rate running at near 2%, if the Fed now believes such is close to a ‘neutral rate,’ it would suggest that expectations of economic growth will slow in the quarters ahead from nearly 6.0% in Q2 of 2018 to roughly 2.5% in 2019.”

This weekend, Presidents Trump and Xi are going to the table to discuss trade and tariffs. While I don’t expect much to actually come from the meeting, I would expect some smiles and handshaking between the two with some positive overtones on “progress being made.”

Regardless of the fact the outcome will have “no teeth” to it, and will ultimately wind up back in a trade dispute over “technology rights” before long, it should be enough to rally the bulls in the short-term.

However, I agree with Goldman Sachs assessment on Friday via Zerohedge:

“Goldman writes that it sees three basic scenarios for what happens after this weekend.

- The first and in Goldman’s view most likely outcome is continuing on the current path of ‘escalation’ – tariff rates rise to 25% on all imports currently under tariff, and tariffs are extended to remaining Chinese imports.

- A close second is a ‘pause’, where existing tariffs remain in place but the two sides agree to keep talking with escalation put on hold.

- A ‘deal’, which Goldman thinks is unlikely in the near term, would involve complete rollback of the current tariffs.

The reason why Goldman is surprisingly pessimistic on the outcome is because there has been a growing sense among US policymakers that China has benefited disproportionately from the bilateral economic relationship, effectively supporting a hard-line stance against Beijing.”

While Goldman is leaning more towards an “escalation,” President Trump has staked his entire Presidential career to the stock market as a measure of his success and failure.

If President Trump was heading into the meeting this weekend with the market at record highs, I think a “hard-line” stance on China would indeed be the outcome. However, after a bruising couple of months, it is quite possible China will see an opportunity to take advantage of a beleaguered Trump to keep negotiations moving forward.

This is also particularly the case since the House was lost to the Democrats in the mid-term. This is an issue not lost on China’s leadership either. With the President in a much weaker position, and his second tax cut now “DOA,” there is little likelihood of any major policy victories over the next two years. Therefore, the risk to the Trump Administration is continuing to fight a “trade war” he can’t win anyway at the risk of crippling the economy and losing the next election.

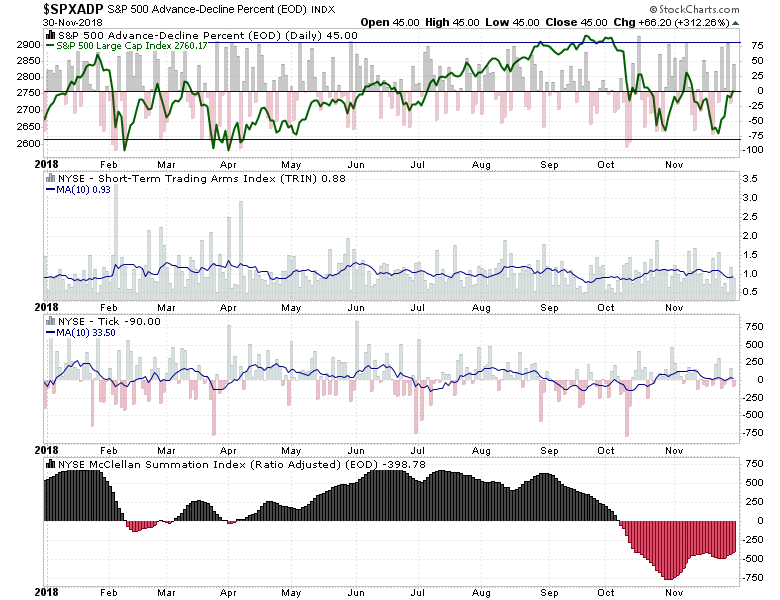

But moving to the technical picture, other than the “one day” super rally, much like we saw immediately following the elections in November, the underlying breadth and technical backdrop has not improved much. The chart below shows the Advance-Decline Percent, TRIN, TICK and McClellan Summation Index all of which have failed to show the improvement needed to establish a bottom has been put into place.

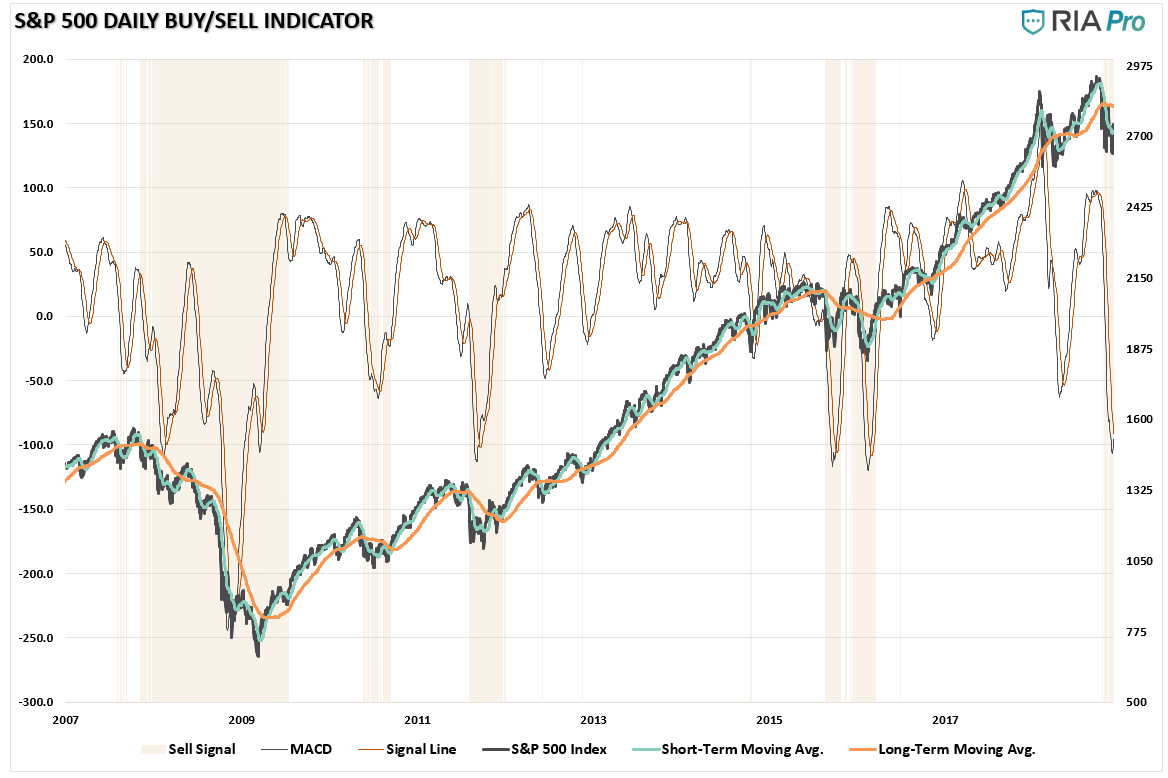

However, with that said, the market did reach extremely oversold levels during the October/November correction which provided the necessary “fuel” for a short-term rally. However, as shown below, the impending “resistance” from both the 50- and 200-dma will likely prove to be a fairly formidable obstacle for the markets to breach in the near-term.

However, notice that in 2015 the market did briefly break above the 50-dma just before the crossover occurred which dragged prices back down with it. The trend of the market is still negative currently, so risk remains to the downside for now. As Victor Dergunov penned last week, the headwinds to the market continue to mount.

- Former leaders are now laggards and are overwhelmingly in deep bear market territory.

- Many sectors are approaching bear market declines.

- Defensive sectors such as consumer staples, healthcare, real estate, and others are outperforming.

- Utility, staples, and real estate stocks are experiencing heavy demand and are behaving much differently than in the prior correction.

- Valuations are still extremely high.

- SPY would need to decline by 33% just to reduce valuations to long-term historical median average.

- Corporate earnings may peak as soon as early to mid-next year.

- Debt levels are extreme and are becoming increasingly difficult to manage and service.

- Future credit is becoming more expensive and more difficult to come by, which is slowing ,economic growth.

- The Fed’s unsupportive policy is putting enormous pressure on asset prices, threatening to deflate multiple bubbles.

- Stocks don’t necessarily need a recession to go into a bear market. Nevertheless, bear markets almost always precede peak earnings and recessionary environments.

With the Fed out of the way until mid-December, the focus for the markets will be any hint of a “roll back” on Trump’s positioning with respect to China, trade, and tariffs.

After having reduced equity risk a couple of weeks ago, we are looking for opportunities as they present themselves. However, for the most part, our bond positions have continued to carry the bulk of the load as of late.

Daily View

The rally over the past few days has virtually exhausted a bulk of the “oversold” condition which previously existed. While such doesn’t mean the market can’t move higher, it simply suggests that most of the “fuel” available for a rally has been utilized. With the markets still on a “sell signal” currently, and below major points of resistance, remaining a bit cautious until the underlying technical backdrop improves seems prudent.

Action: After reducing exposure in portfolios previously, and portfolios much heavier in cash currently, we will sit with our winners and core positions and allow the markets time to figure out what it wants to do next.

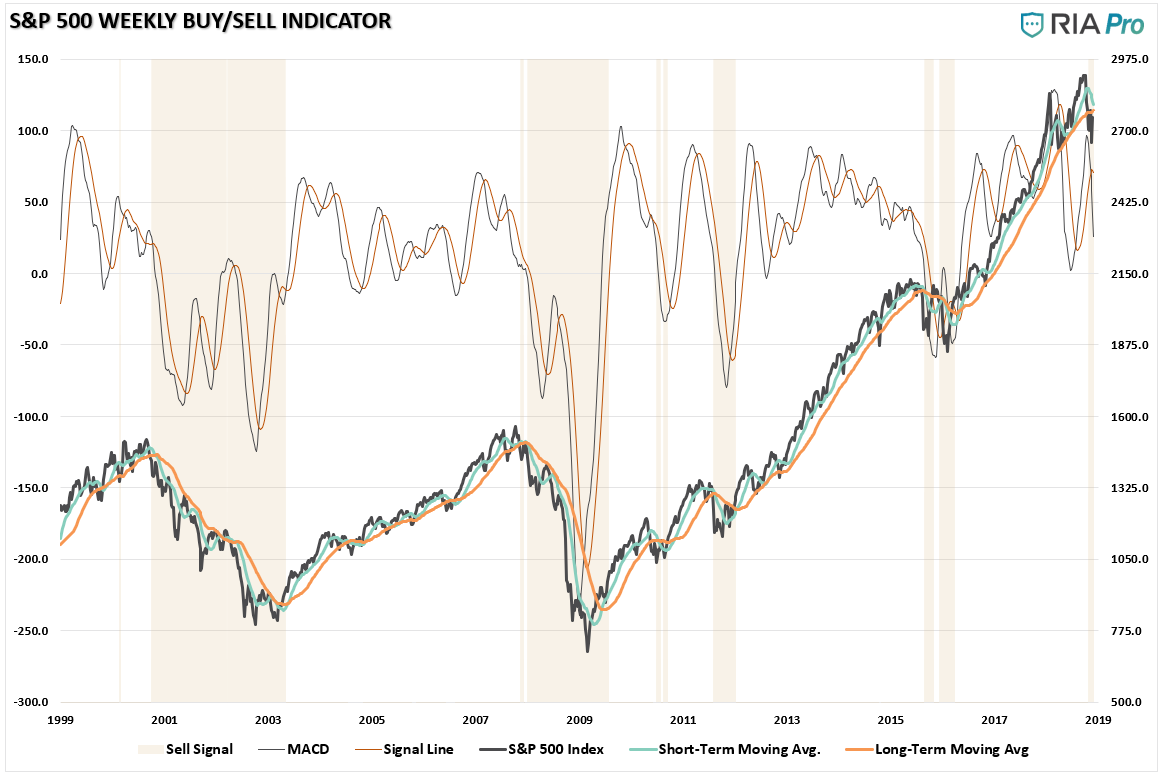

Weekly View

On a weekly basis, the story remains much the same. With a sell signal registered for only the 7th time in the past two decades, we will just allow the markets to figure out what they want to do before getting more aggressive. The recent violations of long-term moving averages suggest a change in market conditions that should not be dismissed. However, should the market improve, and ultimately reverse the relative “sell signals,” we will gladly increase exposure back to target weights.

Action: Hold higher levels of cash and rebalance risk as necessary on this rally.

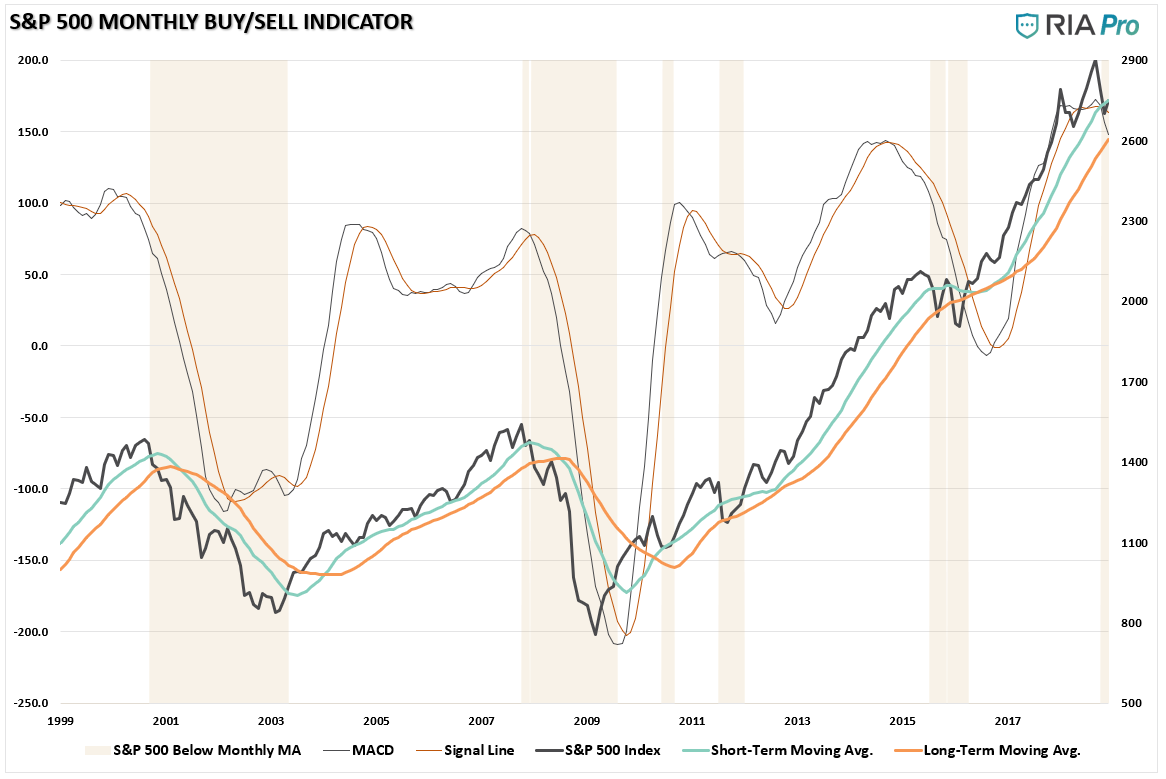

Monthly View

Like the daily and weekly analysis above, the market has confirmed a “sell signal” on a monthly basis as well. The good news here is that the long-term moving average, which is a critical level of bullish trend support, has NOT been violated as of yet. This suggests the longer-term bullish trend remains intact and we should not get overly conservative just yet.

Nonetheless, the deterioration in the markets is extremely concerning, and while the official “bull market” is not dead as of yet, there are more than enough warnings which suggest erring to the side of caution, for now, is warranted.

Action: Use the current rally to reduce risk and rebalance portfolios accordingly.

As always, we will keep you apprised of what we are thinking.

You can also follow our actual portfolio models and positioning at RIA PRO.

See you next week.