Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

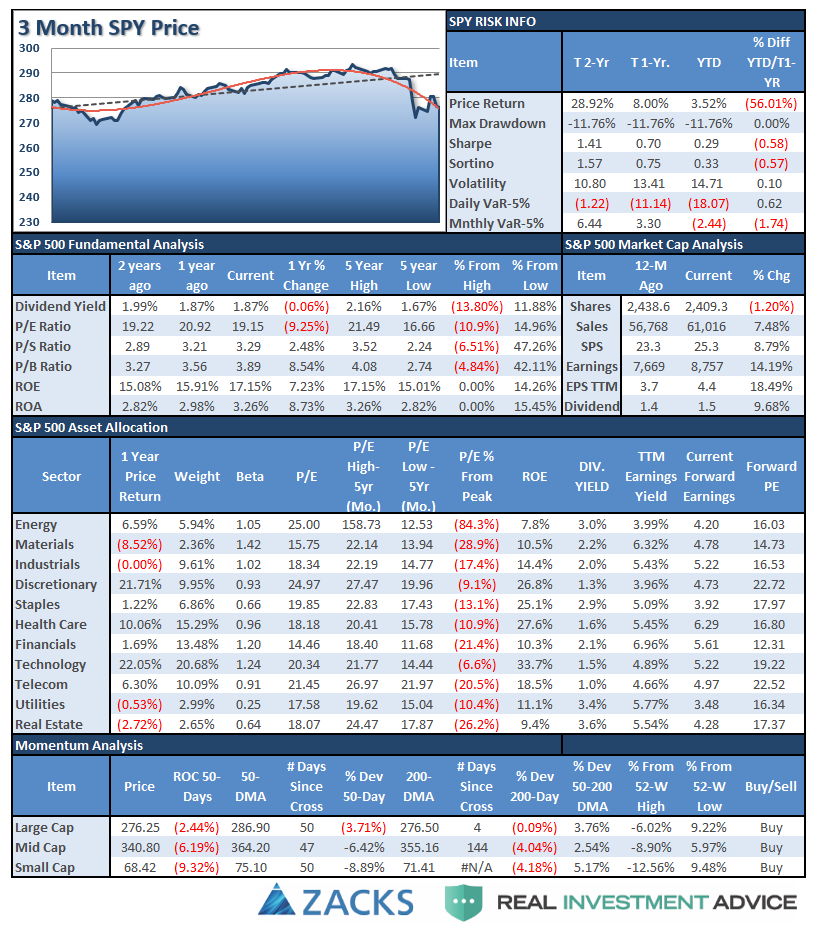

S&P 500 Tear Sheet

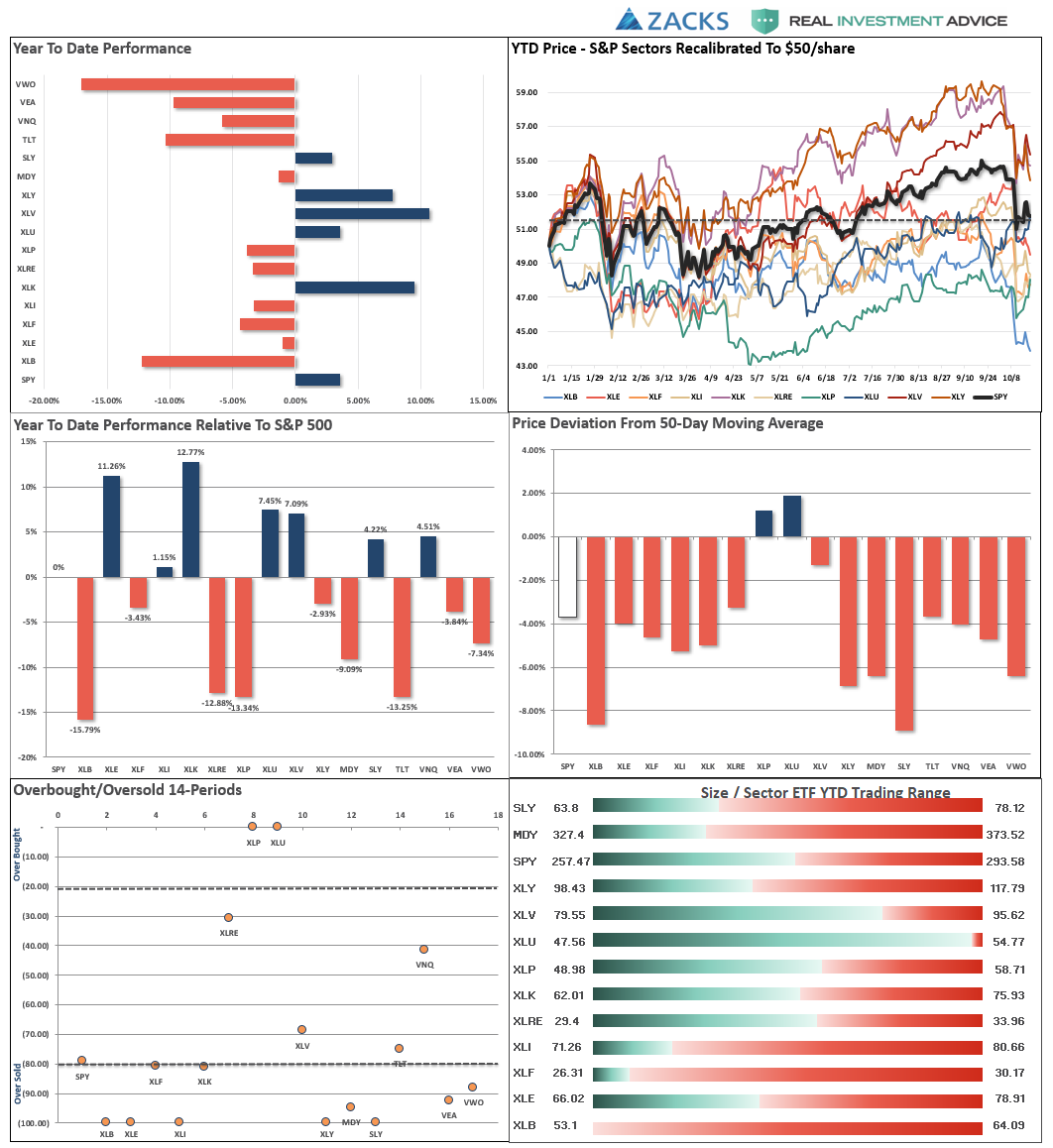

Performance Analysis

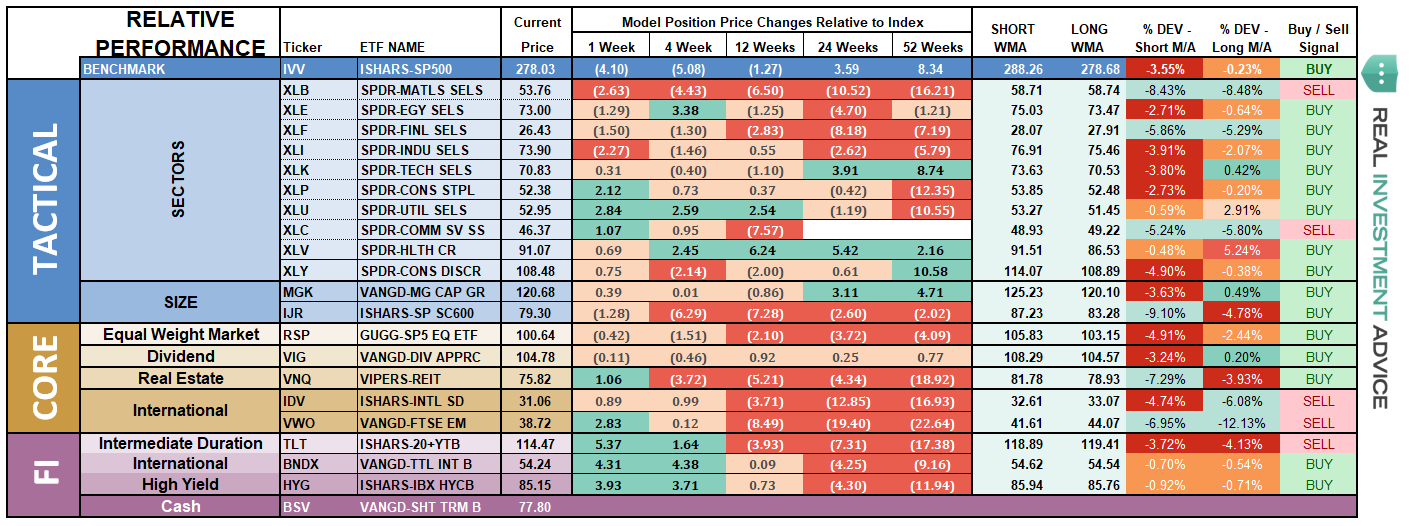

ETF Model Relative Performance Analysis

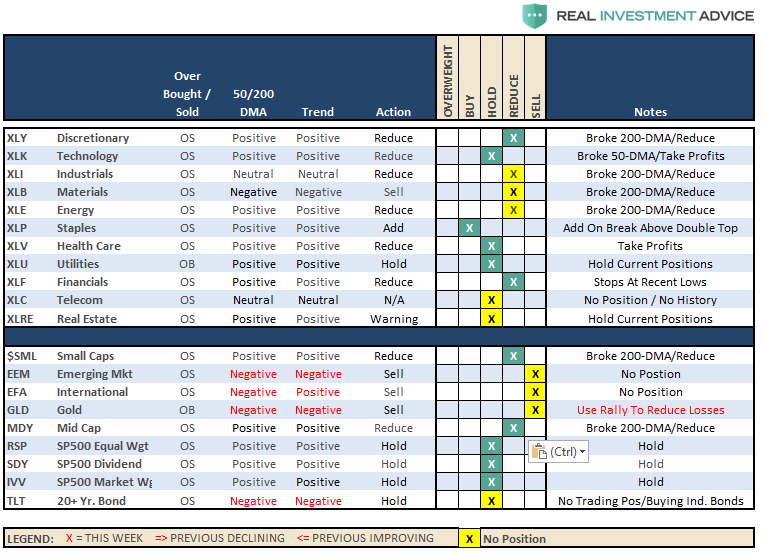

Sector & Market Analysis:

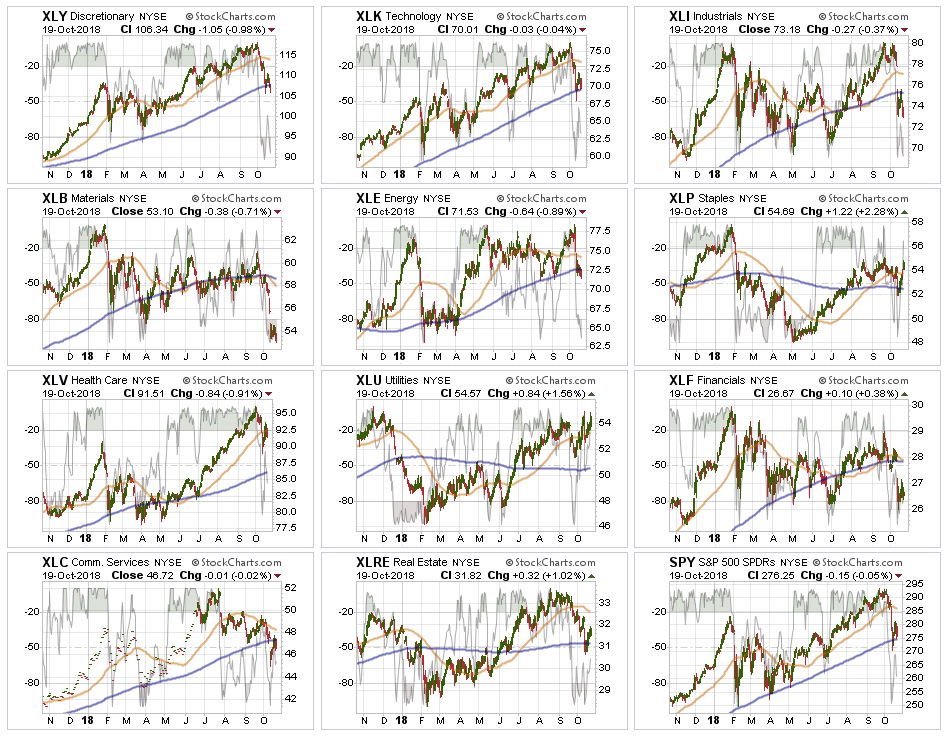

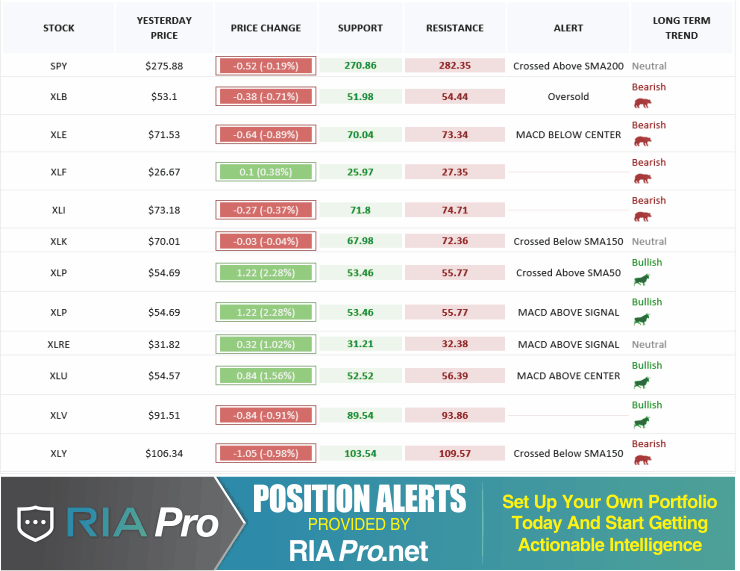

Sector-by-Sector

Discretionary, Industrials, Materials, Staples, Energy, and Financials have all violated their 200-dma and failed to recover. Financials are particularly troubling given the decent fundamental backdrop for banks currently. These sectors are now in “sell rallies” mode until there is a resumption of a more bullish trend. Basic Materials violated its April lows and all previous stop levels. This sector should be sold on any rally in the coming days. Industrials also failed a rally to its 200-dma confirming a sell for the sector. Energy is now a sell after failing at a double-top and then breaking the 200-dma.

Real Estate, Healthcare, and Technology have held their 200-dma support during the recent rout. Technology is hanging on to that support along with the overall market. Real Estate rallied last week back above the 200-dma and off of previous support, however, the downtrend is still negative at the moment. Healthcare, after recommending to take some profits, broke below its 50-dma on big volume. Continue to rebalance risk in portfolios.

Staples & Utilities – the rotation to safety trade, despite higher rates, is evident in both of these sectors. Staples, after a successful test of the 200-dma surged back above the 50-dma last week. The sector is about to test a triple-top but a break above that level will put it on a momentum buy signal for portfolios. Utilities broke out to all-time highs last week also putting the sector on a momentum buy.

Small-Cap and Mid Cap – the breakdown in small and mid-cap stocks suggest a broader change to the overall market complexion. Last week, both markets violated their 200-dma and their bullish trend lines from February of this year. Last week, both indices failed a test of the 200-dma and are threatening to break recent lows. Sell any rally and put a stop at recent lows.

Emerging and International Markets this past week, both markets retested their lows. There still remains, since we recommended selling in January of this year, no reason to be long these sectors just yet. If we start to see real improvement, versus a bounce in a downtrend, we will reconsider our weightings.

Dividends, Market, and Equal Weight – The overall market dynamic appears to have changed last week. With the markets deeply oversold short-term look for a rally to reduce risk, rebalance weightings in portfolios, and raise some cash.

Gold – as I noted last week:

“After repeated failures at the 50-dma, the metal finally found some life in the midst of the recent market meltdown. With Gold now extremely overbought short-term, use this rally to sell holdings if you are deeply underwater. From a trading perspective, IF, and this is a big if, Gold can hold the 50-dma on a pullback and turn higher, a rally to the 200-dma is feasible. Such would coincide with a much bigger sell-off in stocks.”

Bonds – broke their near-term support at $114 triggering the stop loss on trading positions. However, we are now aggressively buying individual bonds at depressed prices and increasing yield in portfolios. All trading positions are currently closed.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

The rally we were wanting to use to reduce risk into last week – last one day. This is not a good sign, and is something that has raised our “caution” levels markedly.

However, despite the volatility of last week’s action, the market DID NOT violate the 200-dma and, therefore, remains a correction within a bull market for now.

The market remains deeply oversold on a short-term basis and we continue to expect a rally this week in which we can reduce equity risk accordingly.

Please review the “Checklist Summary Of Actions To Take” in the main missive above. We will be applying this rules to our portfolios as well.

- New clients: We are holding OFF on-boarding into our portfolio models until a better risk/reward opportunity emerges.

- Equity Model: All positions are being reviewed and positions that have violated stop levels will be sold to reduce portfolio risk.

- Equity/ETF blended – Same as with the equity model.

- ETF Model: We will reduce small and mid-cap holdings on any rally back toward the 50-dma.

- Option-Wrapped Equity Model – If the market rallies back to previous resistance levels, we will add a long-dated S&P 5oo put option to portfolios to hedge risk.

As we have repeatedly stated, we are well aware of the present risk. However, these violent declines are symptomatic of the liquidity issues posed by the massive surge in passive indexing.

As we have stated previously:

“This is why we ‘step’ into positions initially. Once a ‘trade’ begins to work as anticipated, it is then brought to the appropriate portfolio weight and becomes a long-term investment. We will unwind these actions either by reducing, selling, or hedging, if the market environment changes for the worse.”

This past week, it did.