Written by Lance Roberts, Clarity Financial

The Real 401k Plan Manager – A Conservative Strategy For Long-Term Investors

Please share this article – Go to very top of page, right hand side, for social media buttons.

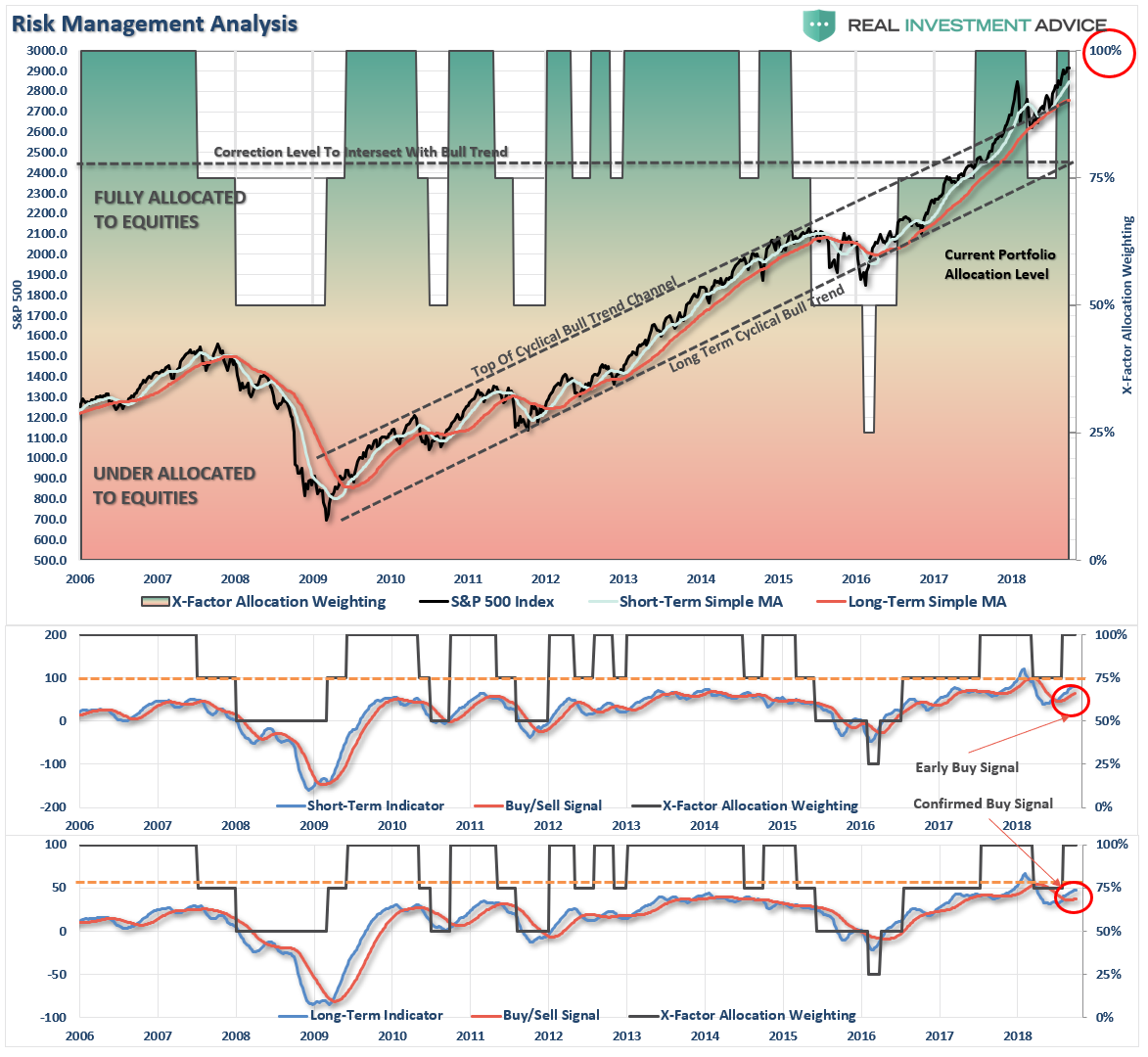

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

Market Is Really Extended

As I noted last week:

“With the move in portfolios back to full target allocations, there is not much for us to do right now except to remain on the lookout for the risks which could rapidly take away our performance.

While there are certainly plenty of resources to tell you why the market should go up from here, which is great if it does because we are allocated to the market, we only need to be concerned with what could now disrupt the bullish advance.

At the moment, we are in good shape just to sit back and ‘watch the show.'”

Such remains the case this week, but I do want to note that the market is extremely extended above its longer-term trend lines and moving averages. Historically, short-term corrective processes like we saw in February are NOT uncommon.

Make sure you rebalance your 401k plans using the following guidelines for now.

- If you are overweight equities – reduce international and emerging market exposure and add to domestic exposure if needed to bring portfolios in line to target weights.

- If you are underweight equities – just hold current positions until a pullback occurs which works off some of the overbought short-term condition. This will provide a better risk/reward opportunity to increase exposure towards domestic equity to levels where you feel comfortable. There is no need to go “all in” at one time. Step in on any weakness.

- If you are at target equity allocations currently just rebalance weights to focus on domestic holdings.

Remember, this is your “retirement money.”

This is the one account you don’t want to #$%! up. Not only do you destroy capital, you also destroy the tax deferral as well as the company match. Be more conservative with your allocations in your 401k-plan because you have less flexibility and fewer options. This is also the one account that is your “safety net” if everything else in life goes wrong.

If you need help after reading the alert; don’t hesitate to contact me.

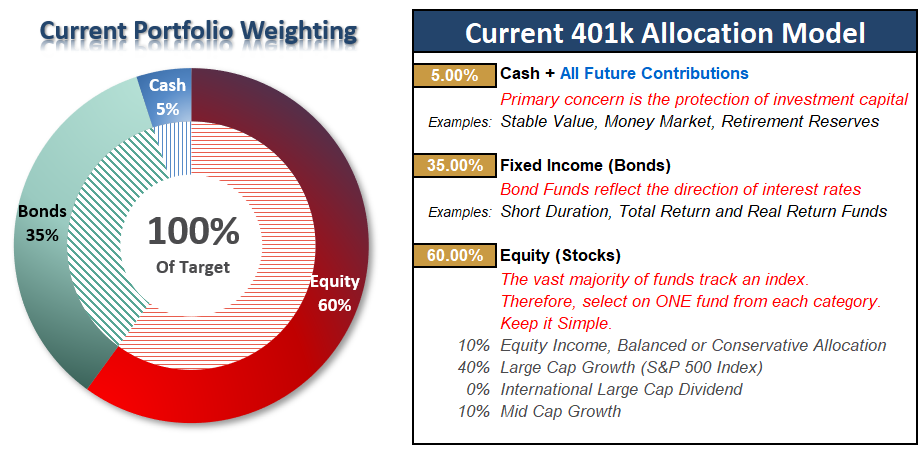

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

401k Choice Matching List

The list below shows sample 401k plan funds for each major category. In reality, the majority of funds all track their indices fairly closely. Therefore, if you don’t see your exact fund listed, look for a fund that is similar in nature.

.