Written by Lance Roberts, Clarity Financial

Economic data has certainly surprised to the upside in the U.S. as of late with unemployment numbers hitting lows, manufacturing measures coming in “hot,” and consumer confidence at record highs.

Please share this article – Go to very top of page, right hand side, for social media buttons.

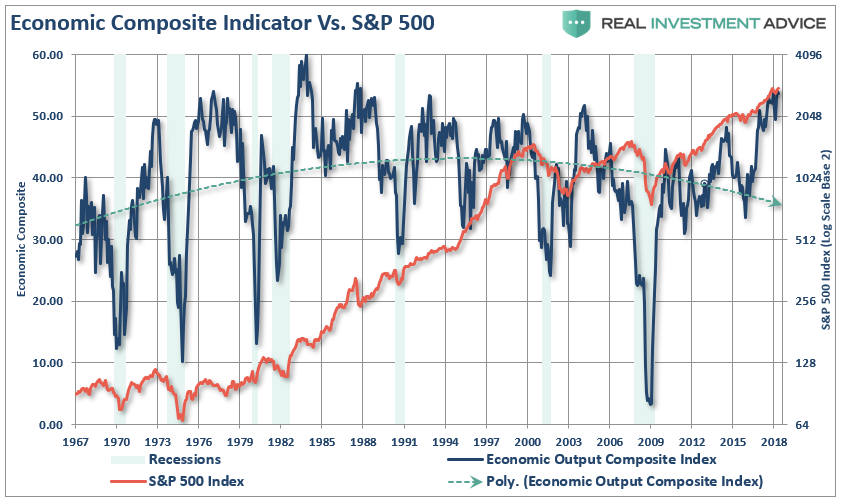

As I discussed just recently, the RIA EOCI (Economic Output Composite Index) is near its highest level on record.

(The index is comprised of the CFNAI, ISM Composite, several Fed regional surveys, Chicago PMI, Markit Composite, PMI Composite, Economic Composite, NFIB Survey, and the LEI.)

But is this recent surge part of a broader, stronger, and sustainable economic recovery?

If you notice in the chart above, these late-stage surges in economic growth are not uncommon just prior to the onset of a recession. This is due to the cycle of confidence which tends to peak at the end of cycles, rather than the beginning. (In other words, when everything is as good as it can get, that is the point everyone goes “all in.”)

However, the most recent surge in the economic data has been the collision of tax cuts, a massive surge in deficit spending, the impact of the rebuilding following several natural disasters late last year, and most importantly, the rush by manufacturers to stock up on Chinese goods ahead of the imposition of tariffs. To wit:

“By plane, train, and sea, a frenzy has begun, resulting in surging cargo traffic at US ports, booming air freight to the US, and urgent dispatch of goods from Chinese companies earlier than planned. Getting in under the wire before Trump’s tariffs bite could mean hundreds of thousands saved on single shipments.

Bloomberg describes this week that cargo rates for Pacific transport are at a four-year high as manufacturers rush to get everything from toys to car parts to bikes into American stores.

This rush, which comes on top of a typically already busy pre-holiday season, is expected to continue well after next week as the tariff will leap from 10 to 25 percent after the new year.

US importers are expected to stockpile Chinese products before the 2019 25% mark. There’s currently widespread reports of companies scrambling to pay expedited air freight fees to dodge the new tariffs, as well as move up their orders. “

This is an important point. Not only has this been the case just recently, but since the beginning of this year when the White House began this nonsensical “trade war.”

“Of course, the most likely outcome will be a return to trade at about the same level as it was just prior to the initiation of “trade wars.” However, it will be a “return to normal,” rather than an actual improvement, but it will give the White House a “win” for solving a problem it created. “

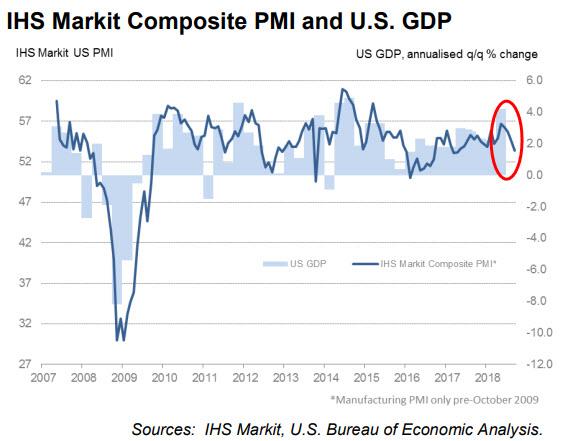

However, this is really a tale of “two economies” as the surge in the economic data is almost solely coming from the manufacturing side of the equation. As shown, the “service” side, which is more immune to the effects of tariffs, has been declining over the past several months.

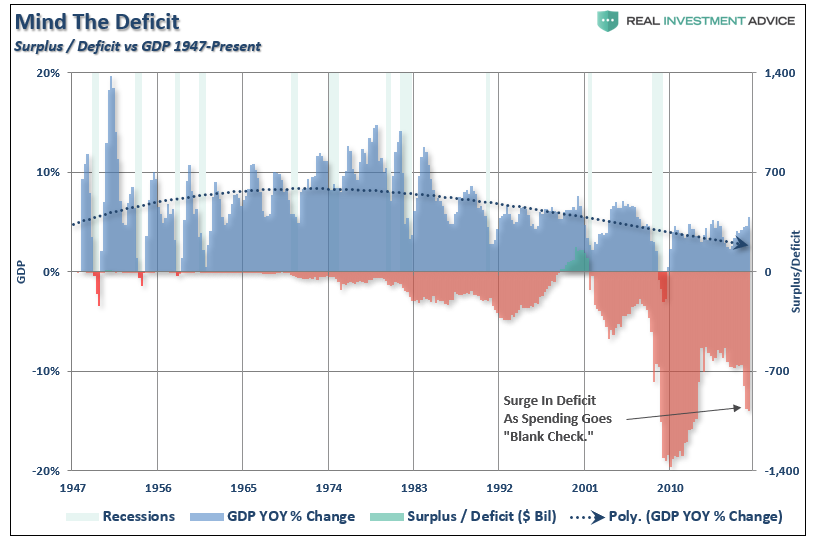

Of course, while so-called “conservative Republicans” are breaking their arms to pat themselves on the back for “getting the economy going again,” the reality is they have likely doomed the economy to another decade of sluggish growth once the short-term burst from massive deficit spending subsides. The unbridled surge in debt and deficits is set to get materially worse in the months ahead as real revenue growth is slowing.

All of this underscores the single biggest risk to your investment portfolio.

In extremely long bull market cycles, investors become “willfully blind,” to the underlying inherent risks. Or rather, it is the “hubris” of investors they are now “smarter than the market.” However, there is a growing list of ambiguities which are going unrecognized may market participants:

- Growing divergences between the U.S. and abroad

- Peak autos, peak housing, peak GDP.

- Political instability and a crucial midterm election.

- The failure of fiscal policy to ‘trickle down.’

- An important pivot towards restraint in global monetary policy.

- An unprecedented lack of coordination between super-powers.

- Short-term note yields now eclipse the S&P dividend yield.

- A record levels of private and public debt.

- Near $3 trillion of covenant light and/or sub-prime corporate debt. (eerily reminiscent of the size of the subprime mortgages outstanding in 2007)

- Narrowing leadership in the market.

Yes, At the moment, there certainly seems to be no need to worry.

The more the market rises, the more reinforced the belief “this time is different” becomes.

But therein lies the single biggest risk to the Fed and your portfolio.

“Bull markets” don’t die of pessimism – they die from excess optimism.

.