Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market & Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

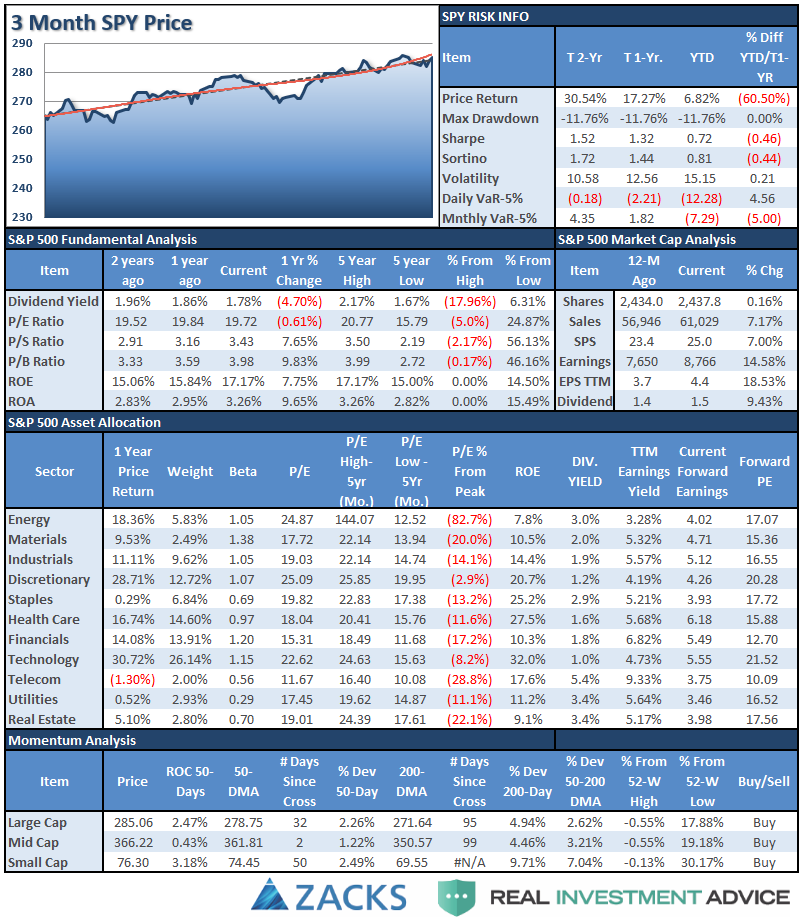

S&P 500 Tear Sheet

Performance Analysis

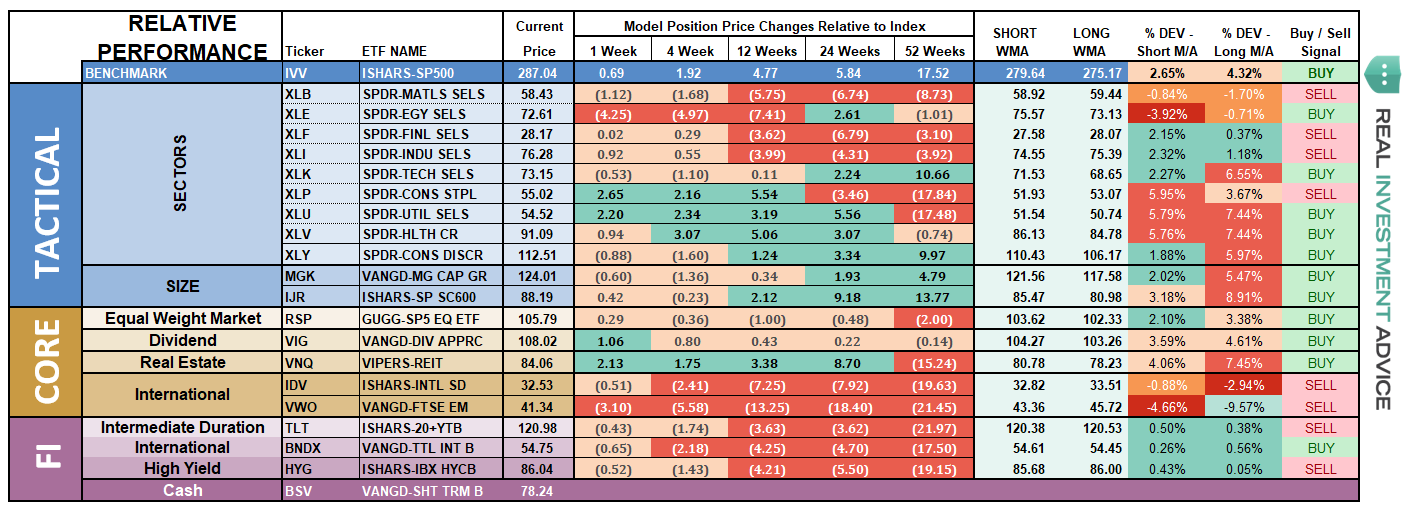

ETF Model Relative Performance Analysis

Sector & Market Analysis:

Discretionary and Technology – Last week we said that after taking profits in Technology, look for a correction back to support. The same goes for discretionary holdings as well. Both sectors started that corrective process last week. Look for a continued rotation this week into more “defensive” sectors but if these two leading sectors reach oversold conditions without violating the 50-dma, positions can be added.

Healthcare, Staples, and Utilities – As we stated last week, after the massive run in Healthcare stocks, take some profits and look for a pullback to support to add additional exposure if warranted. Likewise, Staples have been part of the sector rotation flow following a long period of underperformance. A pullback to the 50-dma will provide a decent opportunity to add exposure if needed. Utilities also continue to perform well here as money continues to rotate into previously “hated” sectors. Look for a correction back to the 50-dma as well to add exposure particularly since the 50-dma has crossed back above the 200-dma.

Financial, Energy, Industrial, and Material Industrials and Materials continue to be weighed upon by the ebbs and flows of a trade war. Industrials are performing better than materials currently, but with the 50-dma still below the 200-dma momentum in the sector remains vacant. Energy has slumped along with oil prices, and is currently testing the 200-dma which could be an entry point for positions provided it holds. Energy is currently oversold and a bounce is likely. Financials continue to languish along support but not showing much in the way of strength to support overweighting the sector currently.

Small-Cap and Mid Cap continue to perform well as of late. We noted two weeks ago, that after small and mid-caps broke out of a multi-top trading range, we needed a pull-back to add further exposure. After having previously added exposure to these markets we continue to allow these markets to perform currently.

Emerging and International Markets were removed in January from portfolios on the basis that “trade wars” and “rising rates” were not good for these groups. With the addition of the “Turkey Crisis,” ongoing tariffs, and trade wars, there is simply no reason to add “drag” to a portfolio currently. These two markets are likely to get much worse before they get better. Put stops on all positions.

Dividends and Equal weight continue to hold their own and we continue to hold our allocations to these “core holdings.” We will overweight these positions on a pullback to support that does not violate that level.

Gold – If you are still hanging onto Gold, we have been consistently providing stop loss levels and sell points since May of this year. These points have continued to decline. With gold very oversold on a short-term basis, if you are still long the metal, your stop has been lowered from $117 four weeks ago, to $111 this week. A rally sale point has also declined from the previous level of $121 to $114.

Bonds – This past week, bonds continued to rally as money looked for “safety” amid the concerns of a collapse in the Turkish Lira. The rally over the past two weeks establishes a series of rising bottoms for bonds AND we have now registered an important “BUY” signal for bonds as the 50-dma crosses back above the 200-dma. As noted previously, we remain out of trading positions currently but remain long “core” bond holdings mostly in floating rate and shorter duration exposure. However, with a “buy” signal in place we will look to add trading positions back into portfolios as necessary.

REIT’s keep bouncing off the 50-dma like clockwork. Despite rising rates, the sector has continued to catch a share of money flows and the entire backdrop is bullish for REIT’s. However, with the sector very overbought, take profits and rebalance back to weight and look for pullbacks to support to add exposure.

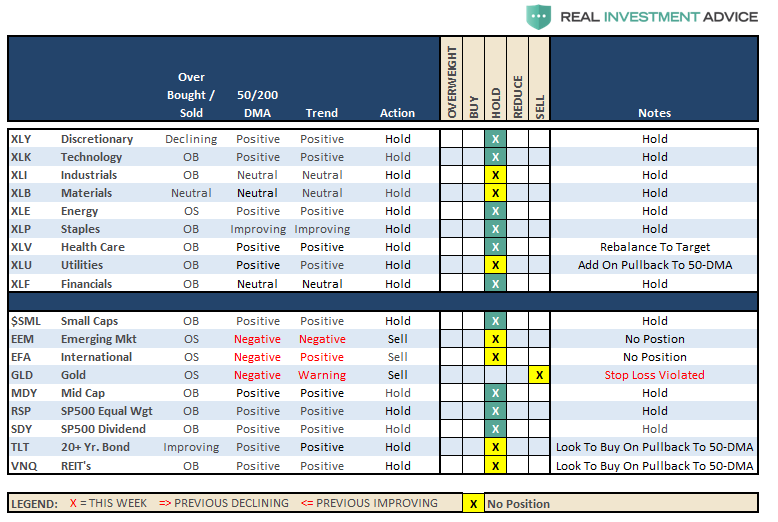

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

Three weeks ago, the market’s improvement allowed us the ability to increase equity exposure in portfolios in anticipation of registering a confirmed buy signal. However, given that August and September are historically weak months for the market, we still remain a bit more cautious regarding how and when we increase holdings in our models.

The recent corrective action was not sustained long enough to provide an opportunity to add to existing positions. However, we suspect over the next month or so that opportunity will present itself given what is happening globally. As long as the cluster of support at the 50- and 100-dma remains in place, which limits much of the downside risk currently, and pullback to support at 2800 will provide an opportunity to add further exposure and bring portfolios closer to target model weights.

Therefore, we continue to look for an opportunity to take the following actions.

- New clients: Add 50% of target equity allocations.

- Equity Model: Increase equity holdings to full weights.

- Equity/ETF blended – increase equity holdings to full weight and overweight domestic ETF “core holdings” to offset lack of international exposure.

- ETF Model: Overweight core “domestic” indices to offset lack of international exposure. Overweight outperforming sectors to offset underweights in under performing sectors.

- Option-Wrapped Equity Model bring all position to target weights and add “collars” opportunistically.

Again, we are moving cautiously. There is mounting evidence of short to intermediate-term risk of which we are very aware. However, the trend of the market remains positive, and we realize that short-term performance is just as important as long-term. It is always a challenge to marry both.

It is important to understand that when we add to our equity allocations, ALL purchases are initially “trades” that can, and will, be closed out quickly if they fail to work as anticipated. This is why we “step” into positions initially. Once a “trade” begins to work as anticipated, it is then brought to the appropriate portfolio weight and becomes a long-term investment. We will unwind these actions either by reducing, selling, or hedging, if the market environment changes for the worse.

.