Written by Lance Roberts, Clarity Financial

While our short and intermediate-term views are more bullishly biased, we are most definitely long-term bears. Ryan’s data points above further support that view.

Please share this article – Go to very top of page, right hand side, for social media buttons.

The laws of physics apply to the markets just like everything else in life. Trying to deny those laws is akin to saying “gravity doesn’t exist.”

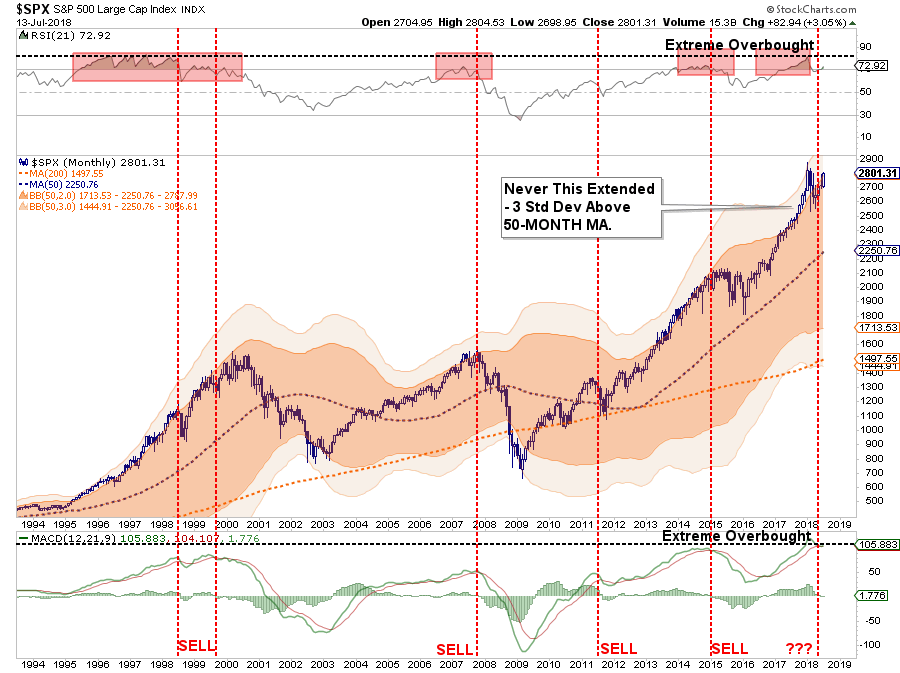

Currently, there is little doubt that we are in both the late stages of an economic cycle and a momentum-driven market. Breadth has narrowed substantially, valuations are elevated, rates and inflationary pressures are rising, and price deviations and overbought conditions are at extremes.

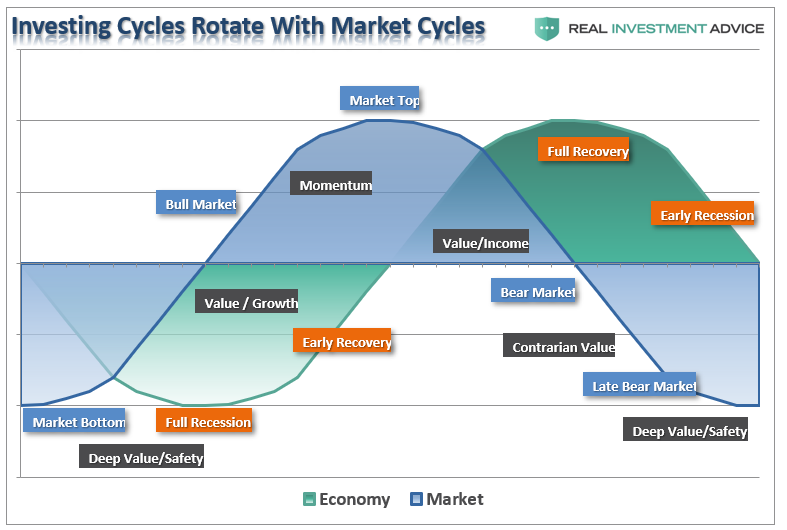

From an investment standpoint, we must maintain an investment focus which is adjusted to current market dynamics. As stated, given we are in a “momentum” market, we must adopt strategies that incorporate relative strength and momentum based measures. The chart below shows the overlay between market and economic cycles and investing strategies.

Momentum cycles are the “last phase” of an investment/market cycle. Eventually, momentum will give way to a “mean reversion” process at which point our focus will switch to a valuation-based strategy.

But this is the risk that most investors are overlooking currently as individuals chase“hot stocks.” The belief is that if they have doubled once, they will double again.

In the short-term, this is not entirely wrong. There have been many studies published that have shown that relative strength momentum strategies, in which as assets’ performance relative to its peers predicts its future relative performance, work well on both an absolute or time series basis. Historically, past returns (over the previous 12 months) have been a good predictor of future results. This is the basic application of Newton’s Law Of Inertia, that states “an object in motion tends to remain in motion unless acted upon by an unbalanced force.”

In other words, when markets begin strongly trending in one direction, that direction will continue until an “unbalanced” force stops it. Momentum strategies, which are trend following strategies by nature, have been proven to work well across extreme market environments, multiple asset classes and over historical time frames.

While there is substantial evidence that market valuations and fundamentals are not supportive of asset prices at current levels, the “momentum chase” can keep markets “irrational longer than logic would dictate.”

But, not indefinitely.

The problem for solely “fundamentally based” investors is they tend to be slow to react to new information (they anchor), which initially leads to under-reaction but eventually shifts to over-reaction during late cycle stages.

The other inherent problem of primarily data-based investors is the “herding” effect.

As prices move higher, valuation arguments lose relevance. However, the need to produce investment performance in a rising market, leads to “justifications” to explain over-valued holdings. In other words, buying begets more buying.

Lastly, as the markets turn, the “disposition” effect takes hold and winners are sold to protect gains, but losers are held in the hopes of better prices later. The end effect is not a pretty one.

Understanding these issues is why we apply momentum strategies to fundamentally derived investment portfolios. This allows the portfolio to remain allocated during rising markets while managing the inherent risk of behavioral dynamics.

While we discuss the risk of investing as it relates to the destruction of both “capital” and “time,” our portfolio models have remained “bullishly” allocated during the market’s advance. But such will change when the markets change.

Our job as investors is to make money when markets are rising during the first half of an investment cycle, and avoid potentially catastrophic losses during the second half.

For now, the markets are rising, and we need to participate until the trends change. Of course, if your current portfolio management philosophy doesn’t have a method to understand when “trends” have changed, how will you know when it is time to step away from the poker table?

To paraphrase Kenny Rogers:

“As every good investor knows…you gotta’ know when to hold’em, know when to fold’em.”