Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

S&P 500 Tear Sheet

Performance Analysis

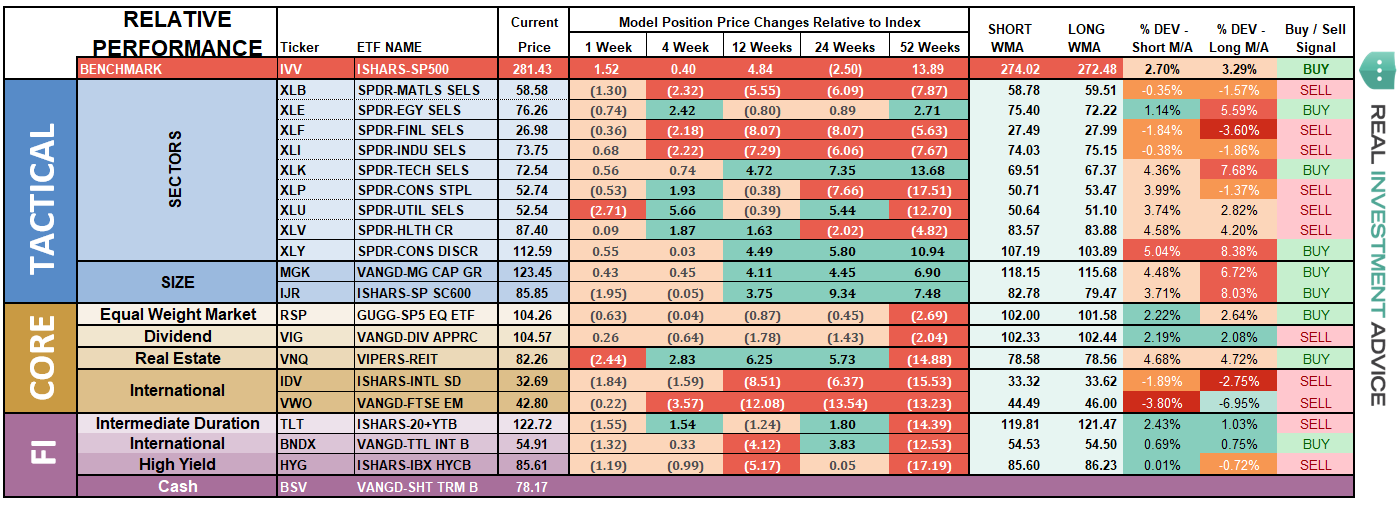

ETF Model Relative Performance Analysis

Sector & Market Analysis:

Last week, the market recovered from the pre-holiday sell-off to effectively get back to where they started. Overall, the breadth of rally has remained more substantially narrow as momentum chasing continues to funnel money into fewer names.

Discretionary and Technology stocks continue to lead the charge and with profit taking already completed in these sectors for now, there is little to do except watch and wait for what happens next. The successful retests of support for both sectors keep us allocated accordingly.

Healthcare, Staples, and Utilities continued their performance recently as money has chased very beaten up sectors in a sector rotation move. After adding Staples to our portfolios previously, we are now looking for pullbacks to support that hold to further add to these holdings. Healthcare also remains at target weights for now but is getting very overbought.

Financial, Energy, Industrial, and Material stocks, after a brief spurt of excitement, have all slipped backward. While the trend for Energy remains in place, for now, we remain underweight holdings due to lack of relative performance. We currently have no weighting in Industrial or Materials as the “trade war” continues to negatively impact the companies in the sectors. The decline of the “yield curve” continues to weigh on major banks and, so far, early earnings reports from the sector have been disappointing. We continue to remain underweight the sector as well.

Small-Cap and Mid Cap continue to lead performance overall. We noted last week, that after small and mid-caps broke out of a multi-top trading range, we needed a pull-back to add further exposure. We recently added small-cap exposure to portfolios and are maintaining stops at the 50-dma. Any further weakness in the markets that hold supports and we will likely increase exposure further. Note: small and mid-caps are purely the manifestation of the “momentum” chase. They are highly sensitive to changes in economic growth and tariffs so maintain stops accordingly.

Emerging and International Markets were removed in January from portfolios on the basis that “trade wars” and “rising rates” were not good for these groups. Furthermore, we noted that global economic growth was slowing which provided substantial risk. That recommendation to focus on domestic holdings in allocations has paid off well in recent months. With emerging markets and international markets continuing to languish, there is no reason to ad exposure at this time. Remain domestically focused to reduce the drag on overall portfolio performance.

Dividends and Equal weight continue to hold their own and we continue to hold our allocations to these “core holdings.”

Gold – we haven’t owned Gold since early 2013. However, we suggested over a month ago to close out existing positions due to a violation of critical stop levels. We then recommended that again given the cross of the 50-dma back below the 200-dma. Then two weeks ago I stated:

“With the 50-dma now back below the 200-dma there is still no reason to own gold currently. If you are long in the metal currently, gold is extremely oversold and a bounce is likely. Use that bounce to reduce holdings for now.”

That bounce came and went. With gold sitting on very short-term support, if you are still long the metal, set your stop to $117. Look to sell on any rally to $121.

Bonds and REITs – Bonds have continued to improve performance despite a continued bullish backdrop to equities. These two things do not generally coincide for long periods, so either, the “bulls” are wrong on stocks or the “bears” are wrong on bonds. I would bet on the latter.

We remain out of trading positions currently but remain long “core” bond holdings mostly in floating rate and shorter duration exposure. REIT’s are much more interesting now with a break back above their 200-dma and now the 50-dma crossing back above the 200-dma. The sector is extremely overbought, so on a pullback that does violate support, you can increase REIT exposure.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

The improvement last week has given us the ability to start slowly adding additional equity exposure to portfolios. A confirmed break above the “Maginot Line,” as discussed above, will be short-term supportive of additions. The cluster of support at the 50- and 100-dma remains in place and we are currently evaluating market conditions for small step ups in equity exposure to add to current holdings. Depending on how the market behaves next week, we are still looking to take the following actions across our portfolio models.

- New clients: Will will look to buy 50% of target equity allocations for new clients.

- Equity Model: We previously added 50% of target allocations. Those positions will be “dollar cost averaged” and 1/2 weight of new holdings will be added opportunistically.

- Equity/ETF blended models will be brought closer to target allocations. We will add to “core holdings” and add 1/2 weight to new holdings and bring existing holdings up to target model weights.

- Option-Wrapped Equity Model will be brought closer to target allocations and collars implemented.

Again, we are moving cautiously, and opportunistically, as we continue to work toward minimizing risk as much as possible. While market action has improved on a short-term basis, we remain very aware of the long-term risks associated with rising rates, excessive valuations and extended cycles.

It is important to understand that when we add to our equity allocations, ALL purchases are initially “trades” that can, and will, be closed out quickly if they fail to work as anticipated. This is why we “step” into positions initially. Once a “trade” begins to work as anticipated, it is then brought to the appropriate portfolio weight and becomes a long-term investment. We will unwind these action either by reducing, selling, or hedging, if the market environment changes for the worse.