Written by Lance Roberts, Clarity Financial

“The Maginot Line, named after the French Minister of War André Maginot, was a line of concrete fortifications, obstacles, and weapon installations built by France in the 1930s to deter invasion by Germany and force them to move around the fortifications. The Maginot Line was impervious to most forms of attack, including aerial bombings and tank fire, and had underground railways as a backup.” – Wikipedia

Please share this article – Go to very top of page, right hand side, for social media buttons.

For the market, the bulls are currently testing the respective “Maginot Line” going back to February of this year.

While the longer-term sell signal remains intact currently, the market has now risen enough to test the last line of resistance standing between the “bulls” and a charge to this year’s highs. With the Nasdaq hitting all-time highs on Thursday, it is now quite likely traders will try to also push the S&P 500 to new highs as well.

However, as of now, the market stands at a critical juncture. As we laid out a couple of week’s ago, it continues to be a “battle of wills” between the bulls and bears. A break above current resistance will bring Pathway #1 into focus as a push to previous highs becomes a very high probability event. If, however, the market fails to move higher, then Pathway #2 will suggest a retest of recent support at the 50-dma which has now also turned positive. The cluster of support which has gathered around the 100-dma reduces, but doesn’t eliminate, the probabilities of a larger drawdown in the short-term.

As I stated previously, these “pathways” are not predictions. The analysis is used to make some “assumptions” about where the markets will likely head given the various risks we are currently weighing in our portfolio allocation models.

Those risks include:

- Trade risk

- Yield curve

- Tweets from the White House (who would have ever thought such would be a risk)

- Interest Rates

- Monetary Policy

- Earnings

- Geopolitical

- Corporate Guidance

You get the idea.

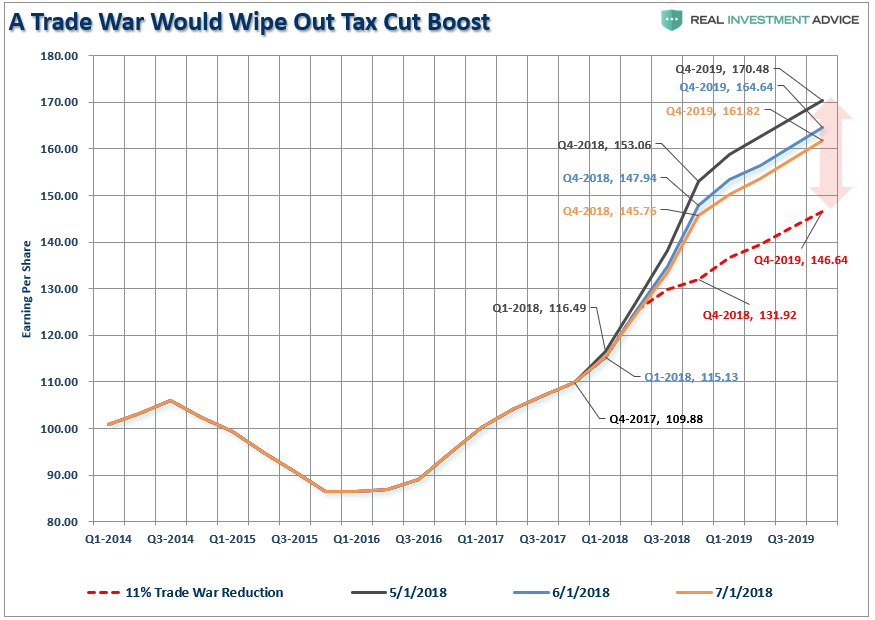

For now, the risk of a bigger correction has been somewhat mitigated particularly as we move deeper into earnings season. Earnings should be somewhat supportive to the bulls as once again, miraculously, there will be a high “beat rate” of earnings estimates. Of course, this is always the case as estimates are lowered prior to entering earnings season so the bar is set low enough to achieve “beat rates.”

In just the last two months, estimates have been lowered sharply. The reality is that if analysts were required to stick to their initial estimates; 1) roughly all companies would fail to exceed their goals, and; 2) Wall Street would be much more prudent, and honest, about their estimates.

But, while that is a philosophical argument, the reality is that we must also “play the game,” and lowered earnings estimates will make “earnings season” more supportive for the bulls.

The “risk” will be the “forward guidance” as companies start talking about the risk to higher commodity prices, a strong dollar, and tariffs. The chart makes an adjustment to account for the risk of a trade war which could effectively eliminate the benefit of the “tax cut” boost entirely.

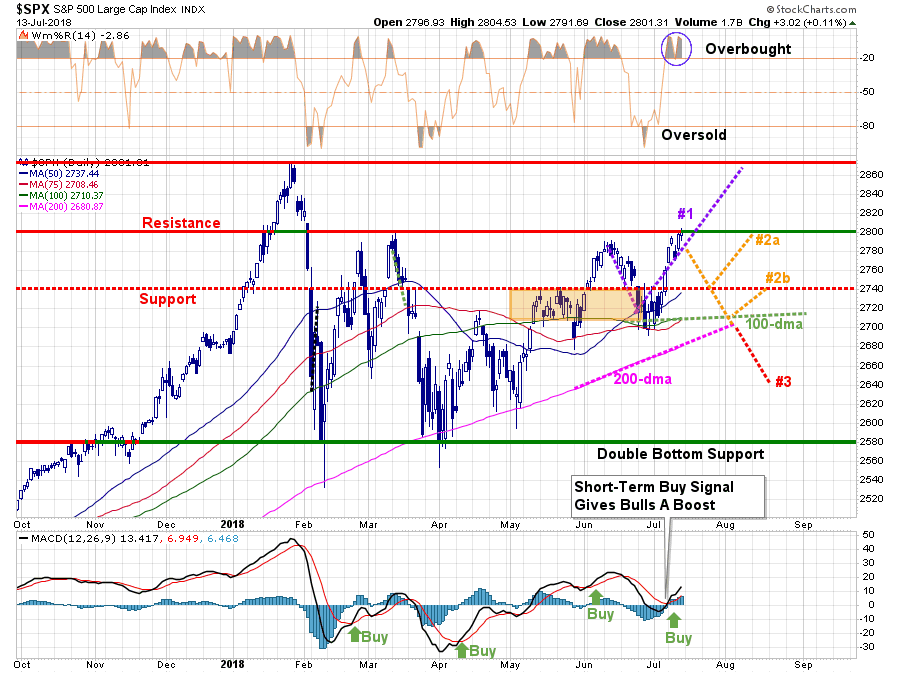

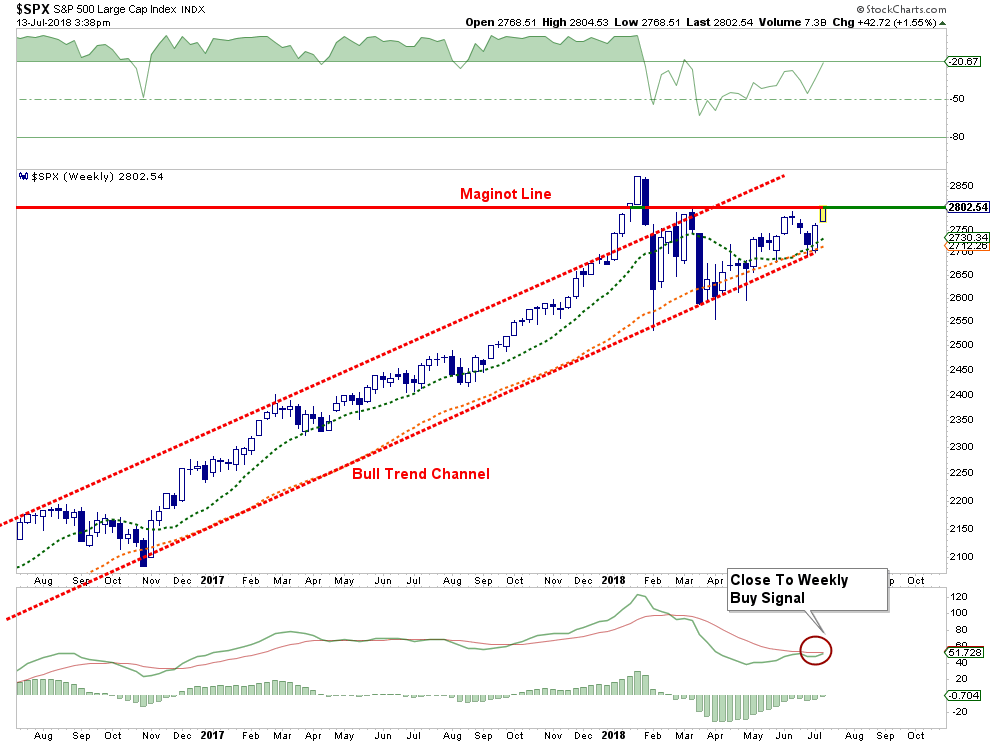

On a weekly basis, the bull’s “Maginot line” becomes clearer.

A couple of weeks ago, I “jumped the gun” and assumed that a weekly “buy” signal was about to be triggered. I quickly relearned my lesson to wit:

“I made a mistake. It happens.

While we strictly adhere to our discipline, sometimes we have to relearn lessons the hard way.

‘Last week, I wrote:

However, if you are so inclined, the pullback to support last week does provide an opportunity to increase exposure modestly. (I said modestly, not ‘jump in with both feet.’)’

That was a mistake as I was ‘anticipating’ a reversal of the ‘sell signal.’ ‘Anticipation’ is an emotion and has no place in portfolio management.

Lesson learned, once again.”

Of course, it is hard to believe that just a few weeks ago we were sitting basically where we are today. With the markets rallying, bullish optimism rising, and the market close to registering a “buy signal,” this time looks a whole lot like “last time.” However, the question is now whether the bulls can succeed where they failed previously.

Next week, either the bulls will breach the “Maginot Line” and claim “victory,” or they will be repelled back to defensive positions.

Currently, based on the very short-term risk/reward analysis, we find the bulls have the edge. With our portfolios are already mostly exposed to equity risk, there isn’t much for us to do expect to wait for a confirmed break higher to begin moving portfolios back to full target allocation weightings.