Written by Lance Roberts, Clarity Financial

Last week, we discussed the flare-up in the “trade war” rhetoric as the current Administration doubled down with China. To wit:

“On Monday, we woke to the “sound of distant drums” beating out the warning of a pending trade war as China vowed to retaliate to the $50 billion in tariffs imposed by the Administration on Friday. On Tuesday, U.S. futures plunged lower after President Trump called for $200 Billion more in Chinese tariffs and China vowed to ‘hit back.’”

Please share this article – Go to very top of page, right hand side, for social media buttons.

Given all the rhetoric it was not surprising to see the market pullback this past week. However, sharply lower opens were repeatedly bought Dana Lyonsas noted by :

“As a matter of fact, in some ways, the bulls resilience over the past 3 days has been unprecedented. Consider this – in each of the 3 days from June 15-June 19, the S&P 500:

- Was down at least 0.75% at some point during the day and

- Rallied to close in the upper 85% of its daily range

How noteworthy is this 3-day feat? As the Chart Of The Day indicates, it is actually the first time the index has ever accomplished it in its nearly 70-year history.”

While it certainly seemed as if the “bulls are bulletproof,” it is worth noting that much of the action not only surrounded a few number of participants but also money was chasing the most shorted of stocks. As noted by Zerohedge:

“And it got even more squeezy today…”

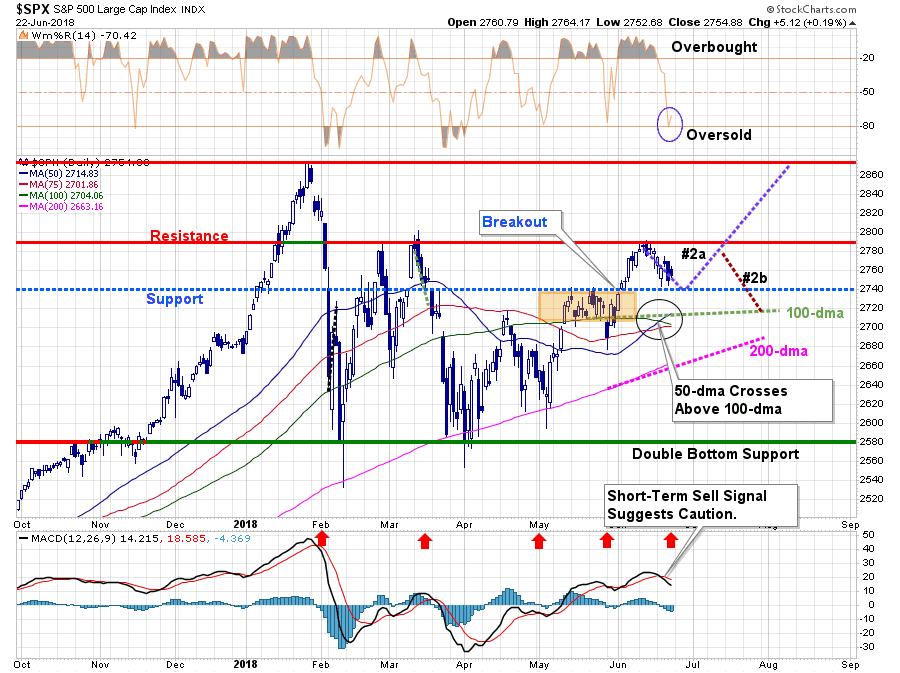

Nonetheless, in the very short-term, bulls do remain in charge and our investment discipline requires us to “follow the action” regardless of how we “feel” about it. Currently, that action remains bullish, and we must look to modestly increase equity exposure as noted last week:

“More importantly, the market is sitting at the critical juncture of either a continuation of pathway #1 toward all-time highs, or a correction of some sort to retest support and confirm this past week’s breakout. A corrective retest that provides a better entry point to increase exposure is the most preferable of outcomes.”

That is what we got this past week as the market retested the most recent breakout above the Fibonacci 61.8% retracement level twice.

We went on to note:

“The market has continued to remain within its bullish trend channel from the 2015 lows which is why we only mildly reduced our overall equity exposure in February of this year. On a very short-term basis, the market is overbought so we will look for weakness next week to add further exposure to portfolios.”

“This is particularly the case given the weekly ‘buy signal’ is close to triggering and any further market strength, or consolidation, will likely trigger that signal by the end of next week. In accordance with our discipline, such a trigger will require opportunistically increasing equity exposure back to target levels.”

While the weekly “buy signal” did NOT trigger this week, keeping our allocation model at 75%, we have been adding exposure over the last few weeks as the market continued to break out of consolidations. As we stated previously, we were looking for the following setup to add equity exposure to portfolios.

- A retracement back to previous support that did not violate it

- An oversold condition on a short-term basis.

- An opportunistic setup for a continuation of our investment pathway #2a

As shown in the chart below, all three requirements were fulfilled this week. Therefore, on Thursday and Friday, we did increase equity exposure and will look to add more on any weakness in the markets early next week.

There is risk to the outlook, however. With the short-term sell signal triggered last week, it does keep us cautious. However, as we have seen previously, such a signal can be reversed quickly. Also, with the 50-dma crossing above 100-dma, further support for a continued bullish advance is back in place.

Importantly, while we are indeed more “bullishly inclined” at the moment, and are willing to give the bulls a bit of “running room,” we have moved stops up. We are also keeping our tolerance for losses restricted as downside risk continues to outweigh reward over the intermediate term.

We still remain slightly overweight in cash, and underweight equities, as the late-cycle risk and trade issues remain heavily prevalent. As noted on Tuesday:

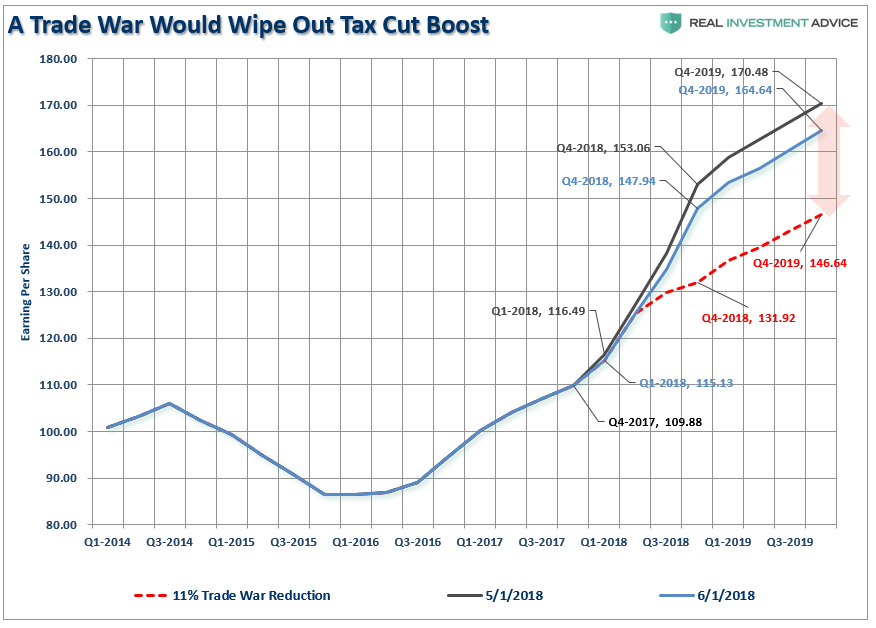

“Wall Street is ignoring the impact of tariffs on the companies which comprise the stock market. Between May 1st and June 1st of this year, the estimated reported earnings for the S&P 500 have already started to be revised lower (so we can play the ‘beat the estimate game’). For the end of 2019, forward reported estimates have declined by roughly $6.00 per share.”

“However, the red dashed line denotes an 11% reduction to those estimates due to a “trade war” as noted by Barclays Bank

‘In a nutshell, the bank calculated that an across-the-board tariff of 10% on all US imports and exports would lower 2018 EPS for S&P 500 companies by ~11% and, thus, completely offset the positive fiscal stimulus from tax reform.’”

As I have often stated in this missive over the last several weeks, we remain invested currently but constantly monitor the risks of what can, and eventually will, go wrong.