Written by Lance Roberts, Clarity Financial

Let’s pick up with where we left off last week:

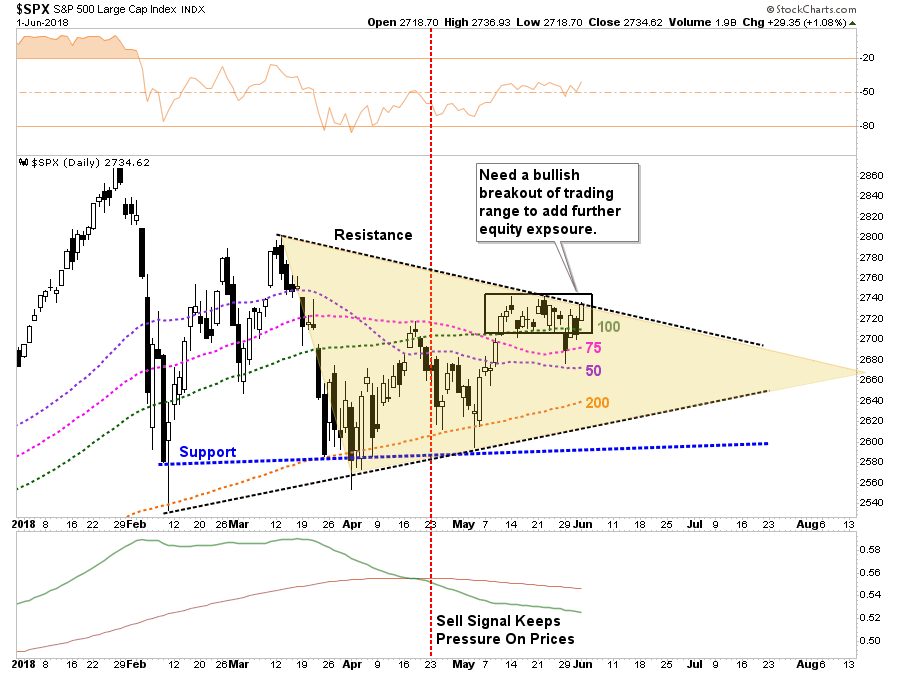

“There wasn’t any “bad news,” so to speak, so the “mediocre” news is that despite the solid rise in the markets from Tuesday’s low, we remain very range bound between the 100-dma and the closing highs over the last couple of weeks as shown below. The tan shaded area is the current consolidation process from the March highs.”

Please share this article – Go to very top of page, right hand side, for social media buttons.

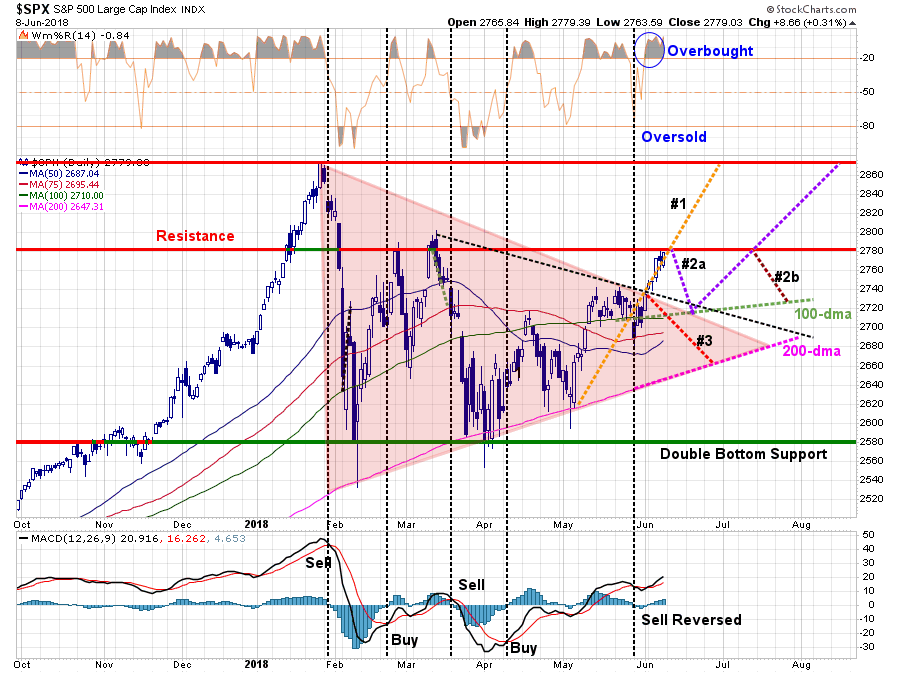

This past week, that breakout did occur and pushed prices, as expected, to the first level of resistance which resides at the late February highs.

As shown, there is a significant amount of overhead resistance between 2780 and 2800 which may present a challenge in the short-term to a further advance. However, I suspect any weakness next week will likely provide a decent opportunity to increase equity exposure modestly.

This idea aligns with the updated the“pathway analysis” from last week.

We had previously given pathway #1, #2a and #2b a 70% probability of coming to fruition. The tracking of pathway #1 also negates pathway #3 entirely for now.

More importantly, the market is sitting at the critical juncture of either a continuation of pathway #1 toward all-time highs, or a correction of some sort to retest support and confirm this past week’s breakout. A corrective retest that provides a better entry point to increase exposure is the most preferable of outcomes.

There are plenty of catalysts next week to provide the markets the necessary catalyst for a short-term sell-off.

- The Fed will hike rates next week, however, their press conference will be closely watched for more “hawkish” undertones.

- Next week, the Trump Administration will announce $50 billion in “tariffs” on Chinese products. The ongoing trade war remains a risk to the markets in the short-term.

- Any unexpected “back-of-the-napkin” policy the White House takes which surprises the market.

- Ongoing liquidity concerns with respect to Italy or Deutsche Bank.

For now, the market has “priced in” most of the “known” risks to some degree. What hasn’t been “priced in” is unexpected economic weakness, a credit related event, or a new geopolitical risk currently not on the horizon. These things happen, and while the current backdrop is very positive for stocks currently, not paying attention to the risks has very negative consequences.

Adding Exposure

As we have noted previously, it is the “end of the week” data which drives our portfolio allocation models and strategy. Using weekly data reduces the “volatility” of the day-to-day price movements and reduces both emotional mistakes and portfolio turnover. As longer-term investors, we are more interested in overall market trends rather than short-term trading victories.

This past week the market cleared the 61.8% Fibonacci retracement from the recent lows which removes a major barrier in reaching previous market highs.

Also, the market held to its accelerated “bullish trend line” from the 2015 lows. Despite the recent corrective action, nothing “bearish” has occurred which is why we only mildly reduced our overall equity exposure. The break above resistance this past week, now allows us to additional increase exposure in portfolios further.

A Word Of Caution

There are only a couple of issues at the moment which keep us mildly heavier in cash. The sharp rise in asset prices this past week, as shown above, was due to a massive “short squeeze” in equities. It was particularly seen on Friday in the most beaten down sectors of retail and staple stocks that have roared back to life. The rally could well be short-lived given the underlying fundamentals that plague these sectors currently has not changed.

Secondly, the weekly “sell signal” has not been reversed as of yet. While the signal will likely be reversed in the next week or so, if the markets continue to advance, it is worth giving the signal the “benefit of the doubt” currently. If you go back and look at the 2015-2016 correction process, which was ended by massive globally coordinated Central Bank interventions, the weekly signal turned positive for a few months before failing into the next correction.

Currently, we do not have globally coordinated Central Bank interventions occurring, rather they are withdrawing their support. The Fed is about to ramp up their balance sheet reductions from $30 to $40 billion a month pulling further liquidity from the markets. The ECB and Japan have also started tapering back.

Also, as Zerohedge discussed on Friday:

“Over the past month, US Investment Grade credit has steadily underperformed its corresponding equities, punctuated by a significant credit widening yesterday. Despite CDX IG 5Y widening 3bps yesterday afternoon to 67bps, there was little SPX reaction and only a modest rise in the VIX. “

Benchmarking the divergence:

“We estimate the equities corresponding to the names in the CDX IG Series 30 are up 3.5% in the past month while a risk equivalent investment in CDX IG 5Y is down 2.8% (selling protection at 12x hedge ratio).

Relative to volatility over the past year, credit has underperformed equity by 3.1 standard deviations over the past 2, 4, 6 and 8 weeks when compared to these same rolling periods over the past year.

This compares to a 2.7 standard deviation dislocation when we last wrote about a similar divergence in January.”

What might this mean for forward equity returns?

“Over the past year, when credit has underperformed equity by an average of 1 standard deviation over a 2, 4, 6 and 8 week period (12% of observations), equity was down an average of -2.3% over the subsequent month. When credit OUTperformed equity by more than 1 standard deviation over a 2, 4, 6 and 8 week period on average (8% of observations), equity was up an average of 2.4% over the subsequent month.”

Goldman’s suggestion:

“We see this difference as significant and leads us to favor de-risking strategies in equities.”

I don’t disagree with Goldman’s analysis, which begs the question “why increase equity exposure further?”

It’s a good question.

The answer is simple, because our strategy, discipline, and models require us too.

There is a more than reasonable risk the markets could well rally to all-time highs only to fail once again.

While the “bulls” will be quick to suggest the markets are set to run indefinitely higher, the reality is that we remain very late in the current cycle, rates are rising, liquidity is being extracted and valuations are elevated. While any one of those issues has proved problematic for stocks in the past, the combination of all of them are a toxic brew longer-term. This is particularly the case with a market that is at extremes rarely seen in market history.

While we will begin slowly increasing our exposure to equities back to target allocations starting next week, we do so with a risk-management process in place.

We encourage you to do the same.

If you don’t have one, it might be time to develop one.