Written by Lance Roberts, Clarity Financial

“Sex is like a fish out of water, there is a lot of flopping around and gasping for air.” – Gary Shandling

Please share this article – Go to very top of page, right hand side, for social media buttons.

The markets were much like Shandling’s view of sex during this holiday-shortened week. There was a lot of flopping around to eventually wind up back where we started. We starting out trading this week with a break of the 100-dma on concerns of Italy and an Italian bank debt crisis. On Wednesday, such was no longer a concern as Fed rate hike odds for June plunged keeping rates “lower for longer.” But Thursday saw another plunge as the current Administration revived concerns over international “trade wars.” Then Friday came with a stronger than expected employment report which was reason enough to rally traders once again.

I’m worn out just writing about it.

The good news is that we did gain a VERY small bit of ground over Friday’s close, but not much.

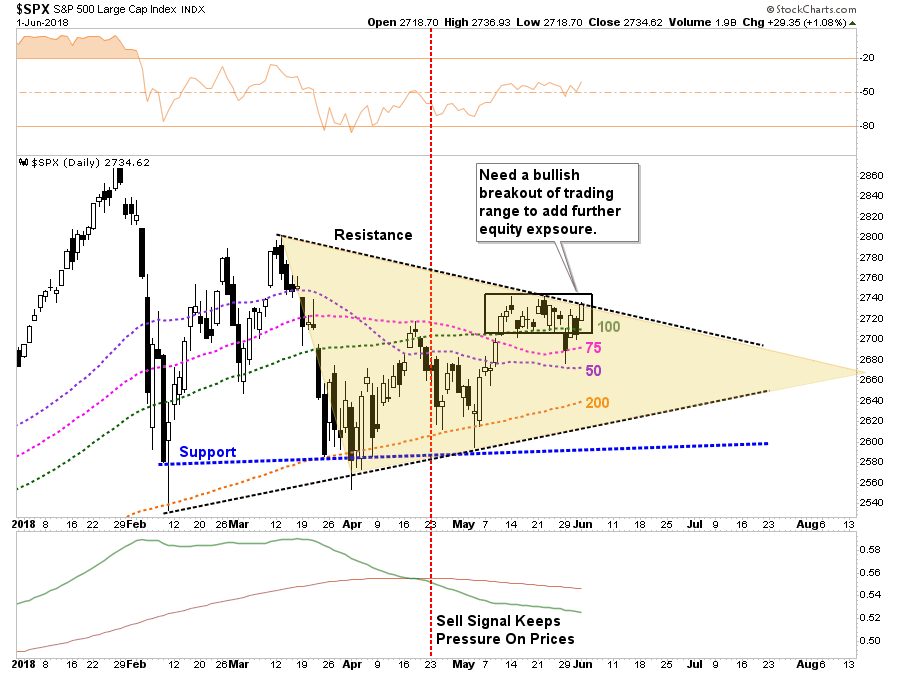

There wasn’t any “bad news,” so to speak, so the “mediocre” news is that despite the solid rise in the markets from Tuesday’s low, we remain very range bound between the 100-dma and the closing highs over the last couple of weeks as shown below. The tan shaded area is the current consolidation process from the March highs.

The daily “sell signal” continues to keep us more cautious on the market currently. More importantly, we are watching the erosion of the gap between the 50-dma and the 200-dma very closely. A negative cross of those two averages has historically been indicative of more extended difficulties for the market.

Importantly, our current equity exposure remains under strict guidelines:

- Overweight cash in portfolios as the “risk” of a failure has not been absolved as of yet,

- Positions are carrying a “tighter than normal” stop-loss level, and;

- We will quickly add negative hedges as necessary on any failure of support.

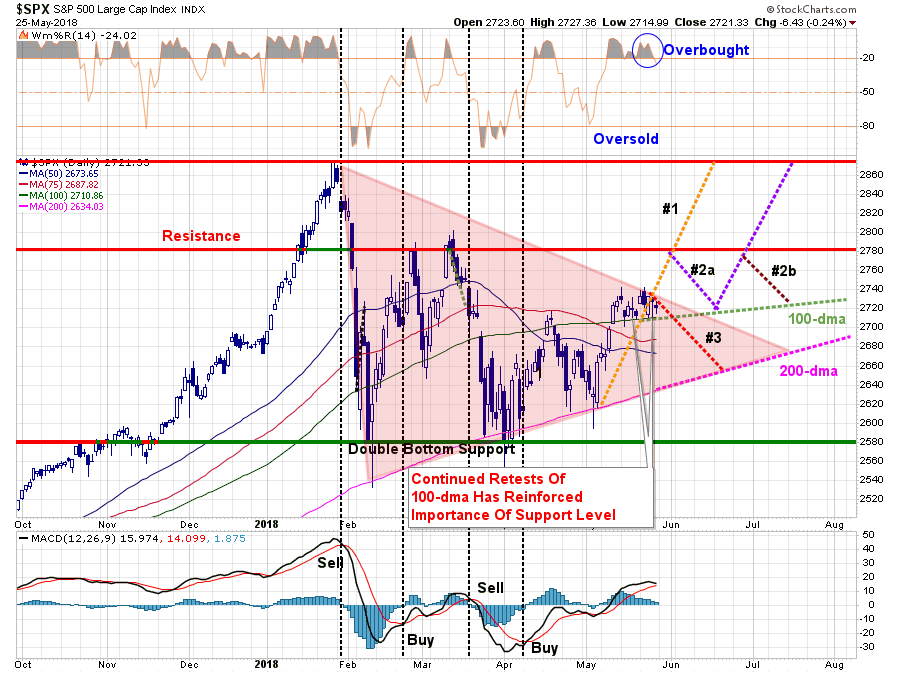

In last week’s missive I updated our “pathway analysis” for the current changes to date.

“As shown by the reddish triangle, the ongoing consolidation process continues. Eventually, this will end with either a bullish or bearish conclusion. There is no “middle ground” to be had here.

- Pathway #1 – a breakout to the upside on heavy volume that pushes the market through resistance at 2780 and back to old highs. (Probability 20%)

- Pathway #2a and #2b – a breakout to the upside which fails resistance at 2780. The market then either a) retests the 100-dma and then is able to push to old highs, or, b) fails at 2780 a second time and continues the consolidation process through the summer. (Probability 50%)

- Pathway #3 – the market breaks down next week on continued geopolitical worries, economic data or some unexpected catalyst and retests the 200-dma. (Probability 30%)

I have increased the more “bearish” probability from 20% last week to 30% this week given the potential triggering of a short-term “sell-signal.” (Lower panel) If the market struggles next week, a triggering of that signal will increase the downward pressure on equity prices.

We will continue to hold our cash position until the market makes some determination as to its direction.”

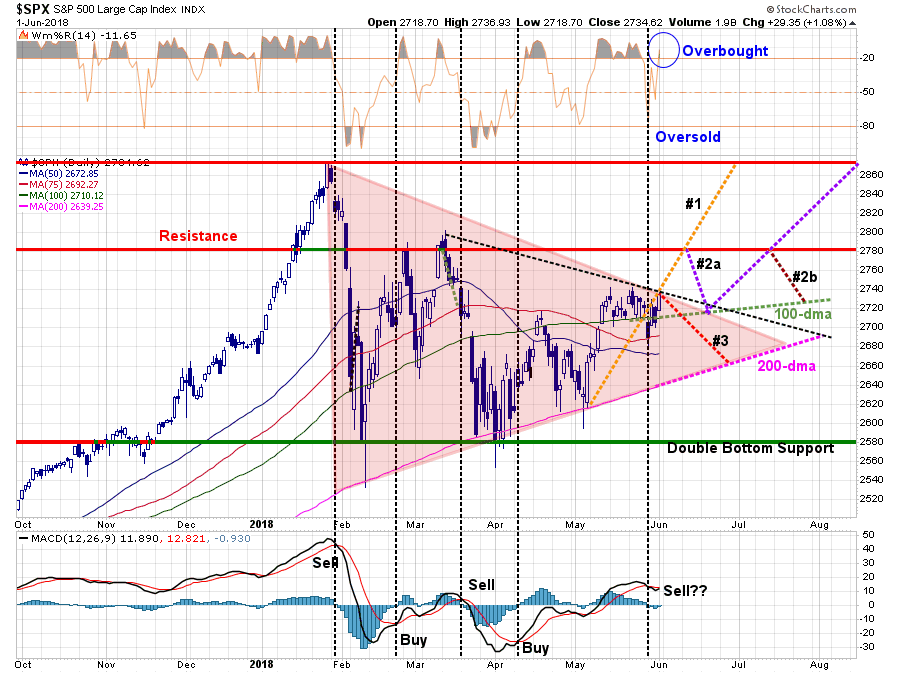

While nothing has changed from last week in terms of “risk versus reward,” the sideways action last week continues to elongate our pathways within the current consolidation process. As shown below the pathways are being pushed further out which coincides with a late summer conclusion and the end of the “seasonally weak” period.

The analysis of the pathways remains the same this week, in terms of the probabilities for the next potential move, I have added the blacked dashed line from the March highs which provided resistance to the market’s advance on Friday.

Despite the improvement of the markets on Friday, there has been little done to solve the issues that plagued the market this week.

- Italy is still a problem

- The elected officials in both Spain and Italy are not particularly “EU” friendly with both recent appointments primarily anti-establishment officials.

- The “Trade War” is just starting to heat up with tariffs begin levied on multiple countries and products.

- China is still a “wild card” in the current negotiations.

- Deutsche Bank, as discussed below, is a major issue of concern.

- Fed continues to tighten monetary policy despite signs rates are already becoming problematic.

I suspect these issues will likely bubble to the surface again over the next several weeks.

With the daily short-term “sell signal” registered on Thursday, and remaining so on Friday, it keeps our allocations on hold until next week. While we have removed a bulk of our hedges, for now, we will be quick to add them back should the market begin to show signs of further deterioration.

As noted above, we are still giving a 70% weighting to a more bullish outcome for our holdings. While there are those who wish to focus on the other 30% and proclaim we are bearish, I assure you we are not.

However, when it comes to investing, and the financial markets, nothing is a certainty. Disregarding the potential for a negative outcome layers excessive risk into portfolios which can damage long-term returns. As I penned previously:

“It should be obvious that an honest assessment of uncertainty leads to better decisions, but the benefits of Rubin’s approach, and mine, goes beyond that. For starters, although it may seem contradictory, embracing uncertainty reduces risk while denial increases it. Another benefit of acknowledged uncertainty is it keeps you honest.

‘A healthy respect for uncertainty and focus on probability drives you never to be satisfied with your conclusions. It keeps you moving forward to seek out more information, to question conventional thinking and to continually refine your judgments and understanding that difference between certainty and likelihood can make all the difference.’

We must be able to recognize, and be responsive to, changes in underlying market dynamics if they change for the worse and be aware of the risks that are inherent in portfolio allocation models. The reality is that we can’t control outcomes. The most we can do is influence the probability of certain outcomes which is why the day to day management of risks and investing based on probabilities, rather than possibilities, is important not only to capital preservation but to investment success over time.

As I have stated before, as a portfolio manager, I am neither bullish or bearish. I simply view the world through the lens of statistics and probabilities. My job is to manage the inherent risk to investment capital. If I protect the investment capital in the short term – the long-term capital appreciation will take of itself.

For those that wish to remain ‘reading impaired,’ there is always “hope” as an investment strategy.”

The market continues to tread water currently. The current question is whether it can keep its head above water until it is rescued, or will fatigue finally drag it under.