Written by Lance Roberts, Clarity Financial

— this post authored by John Coumarianos

Recently financial advisor Ben Carlson wrote about why bonds are still useful for many investors. The argument comes down to psychology and volatility. After all, high-quality bonds tend to hold up when stocks hiccup.

Please share this article – Go to very top of page, right hand side, for social media buttons.

And although inflation can hurt them, accepting that risk has been a reasonable price to pay for the downside protection bonds provide during economic slowdowns, times of fear, and episodes of stock market retreats from over-valuation. Everyone needs a shock absorber in a portfolio, and bonds have served that role reasonably well. If having a lower volatility portfolio prevents you from selling stocks after big declines, then bonds have done their job.

The “spreadsheet answer” on how to allocate capital, according to Carlson, differs from the psychological answer. The spreadsheet answer says young investors should simply own stocks. Since 1926, Carlson notes, stocks have outperformed bonds more than 85% of the time on all rolling 15-year periods calculated on a monthly basis. But, because most people can’t tolerate the volatility of a pure stock portfolio, some bonds are required even for young, aggressive investors.

Beyond The Psychological And Spreadsheet Answers

The problem with both the psychological and spreadsheet answers to the allocation question is that neither of them take valuation and prospective returns into consideration. Are stocks always poised to outperform bonds over long periods? And just how long is long? A decade? Two decades? Carlson is perhaps too sure of answers to these questions. Most investors don’t have, say, five decades.

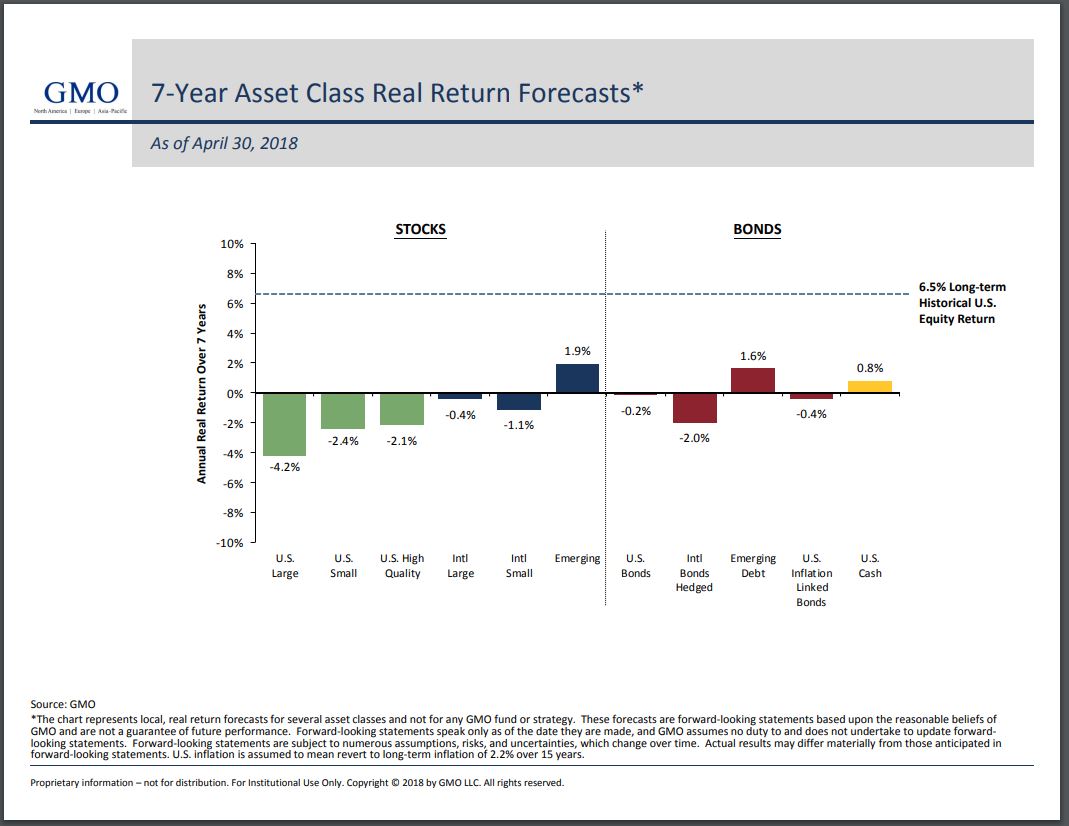

Recently, Boston-based asset management firm, Grantham, Mayo, van Oterloo (GMO), forecasted that over the next 7 years U.S. bonds (both nominal and inflation-protected) would outperform stocks around the world, save those from emerging markets. Prospective bond returns aren’t exciting, with plain U.S. bonds poised to lose .020% to inflation annually and inflation-linked bonds set to lose 0.40% annually to inflation. But, by GMO’s lights, U.S. bonds and U.S. inflation-linked bonds could outstrip U.S. large cap stocks by 4 and 3.8 percentage points, respectively, on an annualized basis.

No forecast is perfect. While nominal bond returns are usually close to bond yield-to-maturity, inflation is unknown. Regarding stocks, future real returns are even harder to forecast. Not only is inflation unknown, but so are future earnings-per-share growth and multiples. It’s possible to combine the market’s current 2% dividend yield with historical 4%-5% earnings-per-share growth to arrive at a 6%-7% annualized nominal return forecast. But will stocks trade at a 30+ CAPE ratio in 7 years, as they do now? It’s not impossible, but it’s unlikely given that the two previous times in history the CAPE has displayed such high readings have been in the runups to the 1929 and 2000 peaks. So, overall, it looks like stocks are priced to lag bonds over the next 7-year period.

And although bonds might deliver higher returns than stocks over the next decade, that’s not necessarily an argument to fill your portfolio with them. There’s very little difference in yield right now between short-term bonds (two-year maturities or less) and longer-term bonds. It’s possible that rates will come back down, making longer-term bonds a better deal. But if you think rates are on their way up – or at least not going back down in a meaningful way – -then short-term bonds, which are almost cash equivalents are better. That’s how GMO has arranged the portfolio of the Wells Fargo Absolute Return fund (WARAX), for example, which has more than 20% of its assets in U.S. Treasuries of 3-year maturities or less.

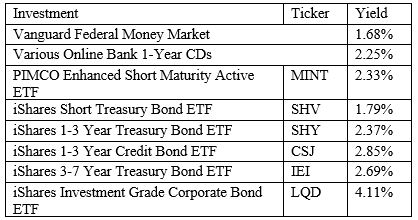

All of this means that bonds still have a place in most people’s portfolios. In fact, as interest rates have been rising, bonds are looking more attractive. The starting yield-to-maturity often indicates an investor’s return from bonds. Below is a list of some money market funds, bond funds (mostly shorter term to intermediate term), savings accounts and their yields. The yields aren’t mouth-watering yet, but they represent some relief from the nearly decade-long income drought for yield-starved investors.