Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

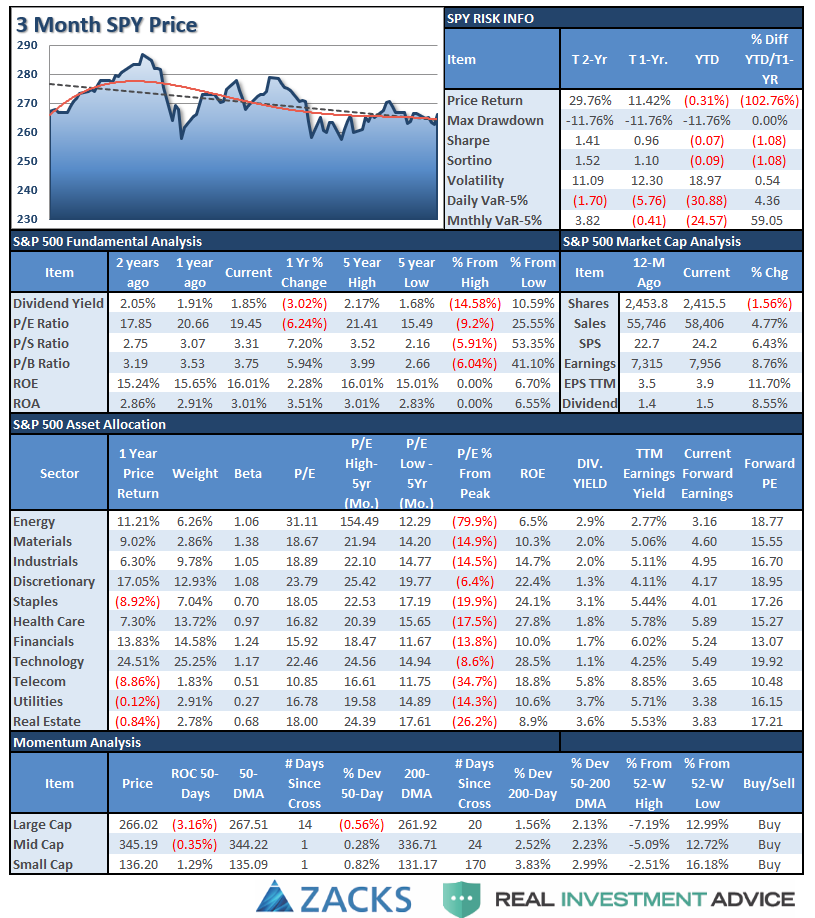

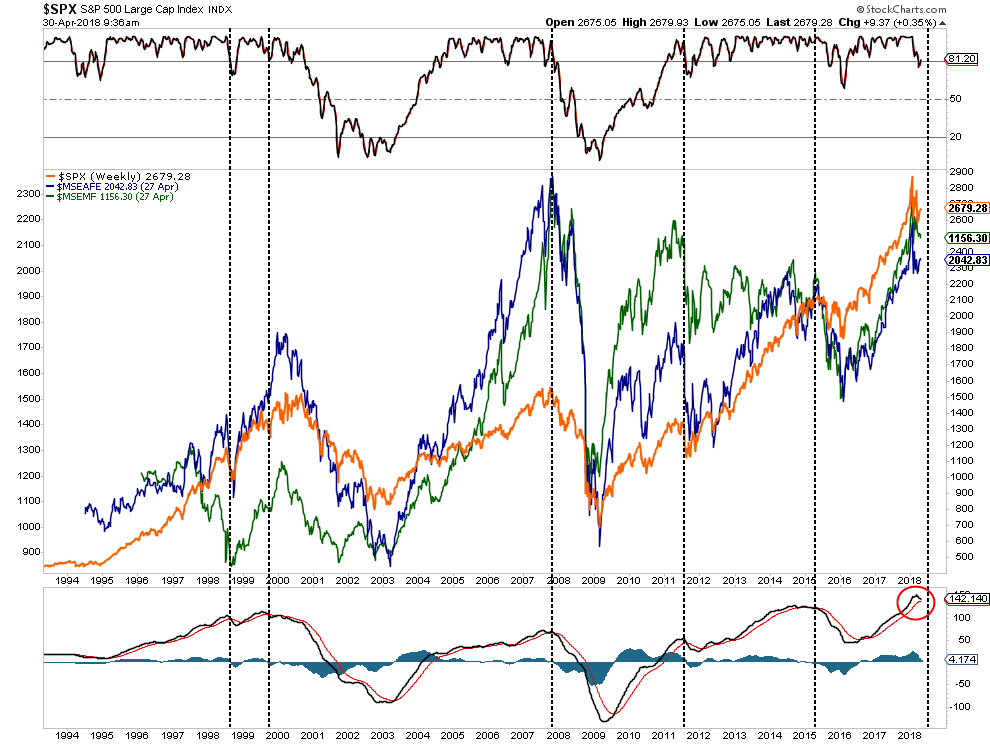

S&P 500 Tear Sheet

Performance Analysis

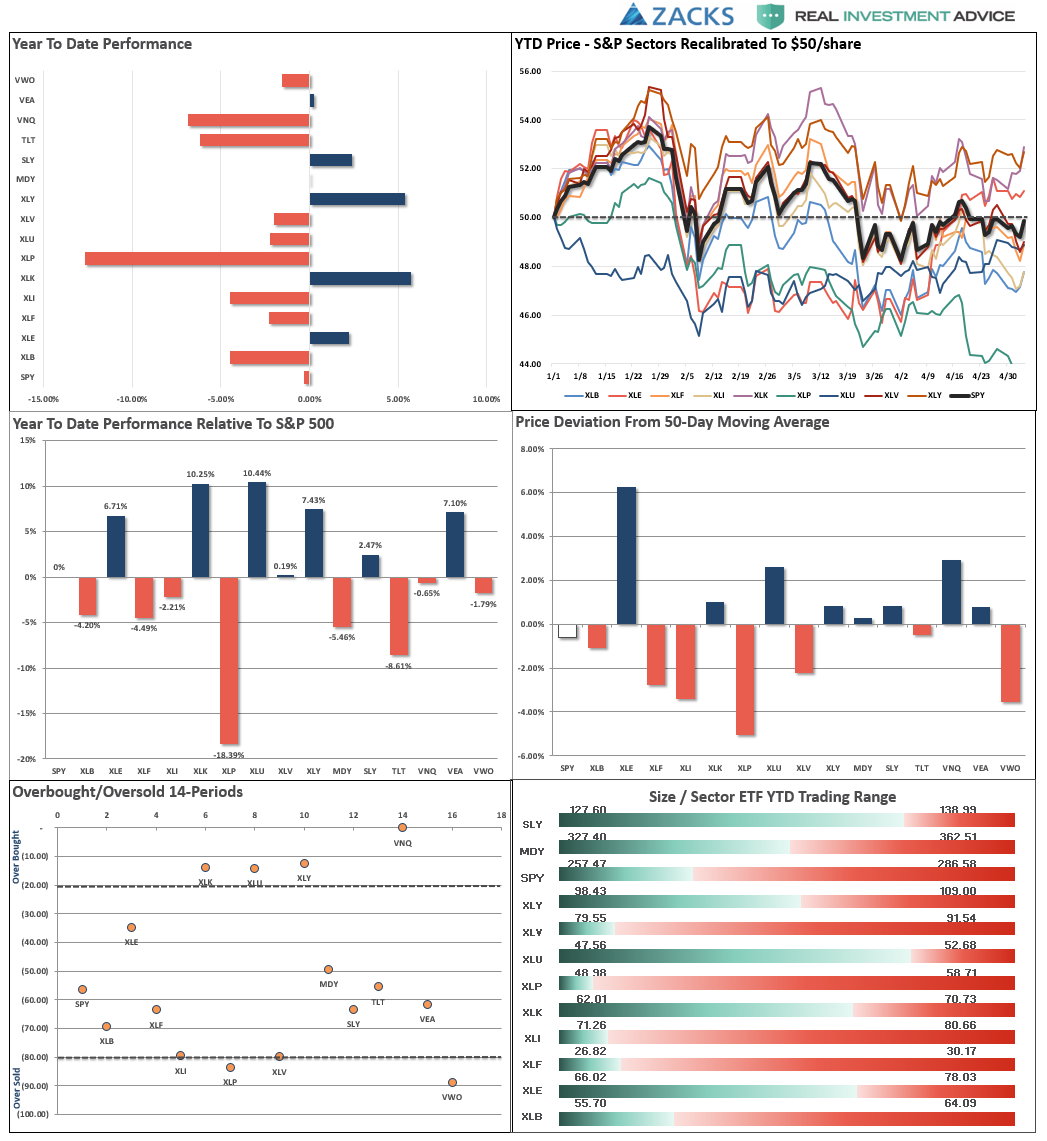

ETF Model Relative Performance Analysis

Sector & Market Analysis:

The action this past week has turned the very short-term trading “buy” signal almost to a “sell” had it not been for the sharp rebound on Friday. However, with the market still on longer-term “sell” signals, remaining below important resistance and still contained in a downtrend, any rally next should continue to be used for raising cash and reducing portfolio risk.

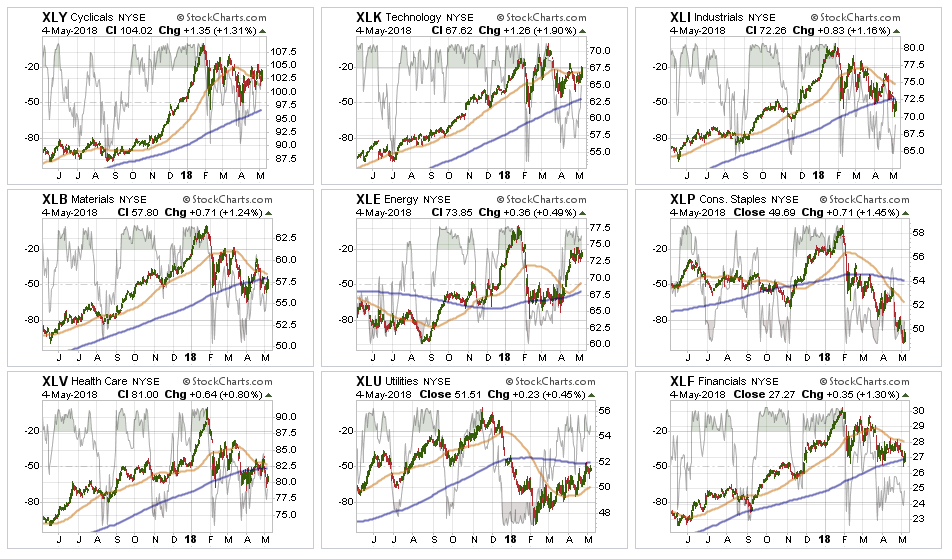

Discretionary, Technology, Energy are the only three sectors actually above their respective 50-dma currently., but just barely. Overall action in these sectors, while they are leading, has been very weak. As stated last week, the parabolic surge higher in Energy stocks faded and the advice to take profits remains this week as well.

Materials, and Industrials – we closed out of our positions in these two sectors earlier this year as “trade war” talk begin to gain momentum. With that threat still present, plus higher borrowing and energy costs, there is more downside risk currently. We remain watchful for a potential entry point, but with both sectors below their 200-dma we will sit on the sidelines and watch for now.

Financials and Health Care continue to lag on a relative performance basis and both sectors are threatening a break of their consolidation support. We are moving stops up to recent lows and remain cautious and underweight relative to normal positioning.

Staples – after completely falling apart after a rally back to the 50-dma, the rotation from “risk” back into “safety” late last week gave the sector a bounce. There is likely an opportunity being formed currently, but it will take some more time to develop first. More importantly, the sector speaks much more broadly about the real health of the economy. Pay attention to the message.

Utilities have significantly picked up performance in recent weeks and have broken back above the 50-dma. We are not recommending adding to the position yet as the moving-average crossover remains negative and the sector remains below its 200-dma. However, performance is improving. Like Staples, the rotation from “risk” to “safety” last week is much more indicative of concerns about overall market risk.

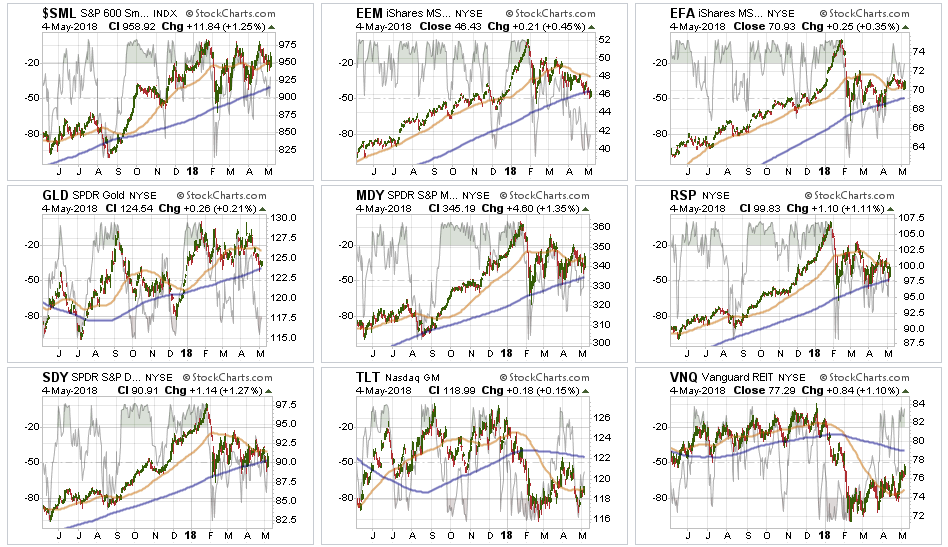

Small Cap, Mid Cap, and International indices all pushed back above their 50-dma but continue to struggle with multiple tops. This is particularly the case with Small-caps which have put in a triple top, Mid-cap is continuing to build a downtrend as well as International. Remain patient at the moment.

Emerging Markets continue to struggle and broke below its 200-dma this past week. The index is also beginning to flirt with important support, a break of which will lead to more significant declines. Despite all of the “poor analysis” of how “emerging markets are cheap relative to the U.S.,” as I penned last week, they are simply a reflexion of U.S. consumption and economic trends. “If the U.S. gets a cold, emerging markets gets the flu.”

We previously removed our holdings in this sector and remain flat currently. We will continue to monitor performance for opportunity if it presents itself.

Dividends and Equal weight continue to hold their 200-dma. We continue to hold our allocations to these “core holdings,” but are closely monitoring performance. The continued development of a downtrend channel is concerning.

Gold continues its volatile back-and-forth trade but remains confined below a massive level of multi-top resistance. Last week, I noted that Gold not only failed another test of recent highs but broke back below its 50-dma. Gold is now flirting with its 200-dma as actually inflationary pressures remain elusive at best. We currently do not have exposure to gold, and have been out for a long-time, but if you are already long the metal hold for now. $123 on GLD is a hard stop.

Bonds and REITs – last week interest rates peaked over 3% for just a brief moment before plummeting back to earth. With a continued string of weak economic reports look for rates to continue to slide lower. The sharp whipsaw in bond prices proved profitable after adding to bond exposure last week. The 50-dma is flattening out which suggests the current sell-off may be near its end. REIT’s, on the other hand, continue to build an uptrend after finding support at the 50-dma. While the sector is very overbought, a correction that maintains the bullish trend will be buyable and we will be looking to add exposure.

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

There is no change from last week’s update.

Over the last several weeks we have continued to maintain higher levels of cash than normal as market volatility has markedly increased. This past week, we tested the 200-dma once again and held support but continue to remain confined to a downtrend overall. This keeps us cautious at the moment and we continue to use rallies to sell “out of model” positions so portfolios can be positioned to enter into our models as the opportunity presents itself.

While we continue to honor the current “bullish trend,” we remain very aware of the rising risks and continue to look for opportunities to derisk and re-hedge portfolios while “sell signals” remain firmly intact.

In our equity/option wrap model, we continue to just let options mature/expire and allow that process to derisk portfolios automatically. That model will be rebuilt as premiums in options in our selected equity screens rebalance to more profitable levels.

As noted last week, the rally has been extremely weak and lacked real conviction. However, if the market can break above the current downtrend channel on heavy volume, confirming a breakout, we will reallocate and rebuild portfolio models accordingly.

For the moment, we are just letting the markets determine the best course of action and we continue to raise cash on technical breakdowns. Our bigger concern, remains the relative risk to capital if the 9-year old bull market is ending. If the current correction expands into a more meaningful reversionary process, we will become much more aggressively risk adverse. There is plenty of evidence to support the latter case.

It is crucially important the market maintains the current uptrend from the recent lows. After having reduced exposure a couple of weeks ago, we remain on alert for the next opportunities.

We remain keenly aware of the intermediate “sell signal“ which has now been “confirmed” by the recent market breakdown. We will continue to take actions to hedge risks and protect capital until those signals are reversed.