Written by Lance Roberts, Clarity Financial

It was interesting to note last week the number of emails I received, as the market rallied higher, all asking one primary question:

“Is the bear market over?”

Please share this article – Go to very top of page, right hand side, for social media buttons.

The question is interesting from a couple of perspectives.

First, the recent downward slide in markets was only a “correction” and not a “bear market.” Both in terms of the percentage decline as well as the lack of reversion in investor psychology.

If the recent decline had been a “bear market,” the primary question would be “should I sell now,” rather than “should I buy?” What the recent correction failed to do was instill any significant level of “real fear” back into the market. High yield spreads remain compressed, the rise in the volatility index was quickly reversed, and investor attitudes were not changed from “greed” to “fear.”

From an investment perspective, those three ingredients are critical for determining longer-term entry points for taking on more aggressive investment postures. “Buy fear, sell greed.”

However, while the market rallied nicely early last week, as noted above, the rally has yet to reverse the current negative trend in the market. This was also noted by Phil’s Stock World earlier this week:

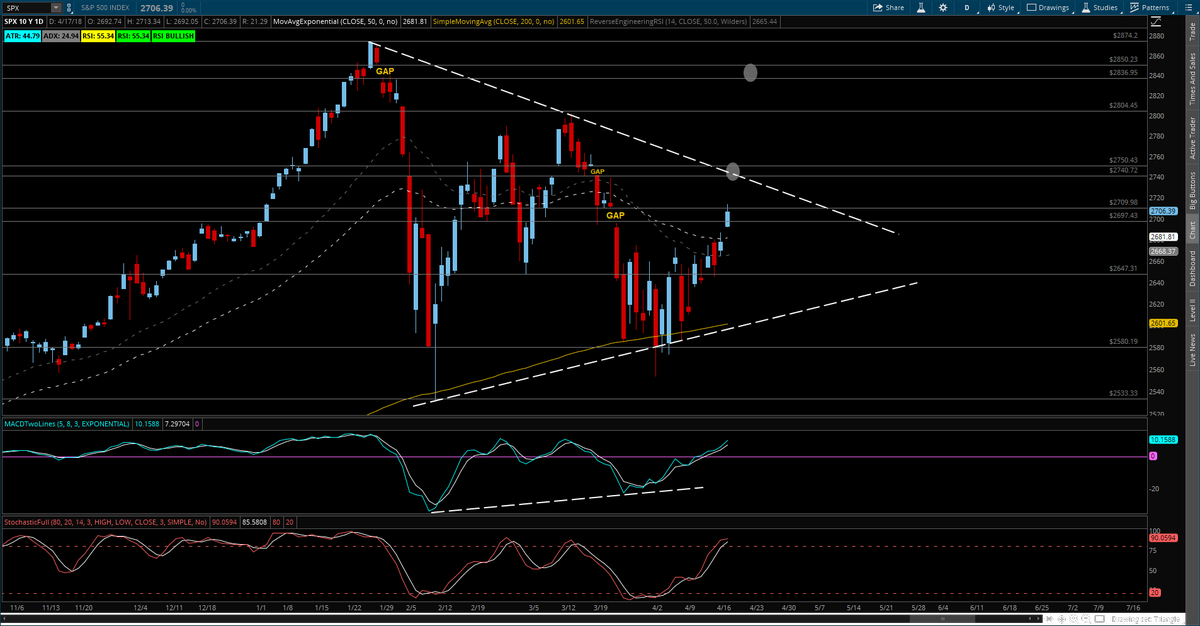

“As you can see from the chart we’re still making one of those triangle squeezy thingy patterns but the top of the down wedge is still at our 2,740 line and it will be three more weeks of this nonsense (while earnings pour in) until it resolves itself but, with the nose of the triangle lower than where we are now (2,717) – the odds favor the short bet on /ES Futures.“

As Phil correctly notes, the market is being currently supported by excitement over “tax cut” driven earnings growth. However, while the bottom line is being boosted by tax cuts, revenue remains another issue. More importantly, investors should keep in mind the “tax cut” benefit is only good for this year as starting in 2019 we will be to comparing normalized year-over-year earnings growth.

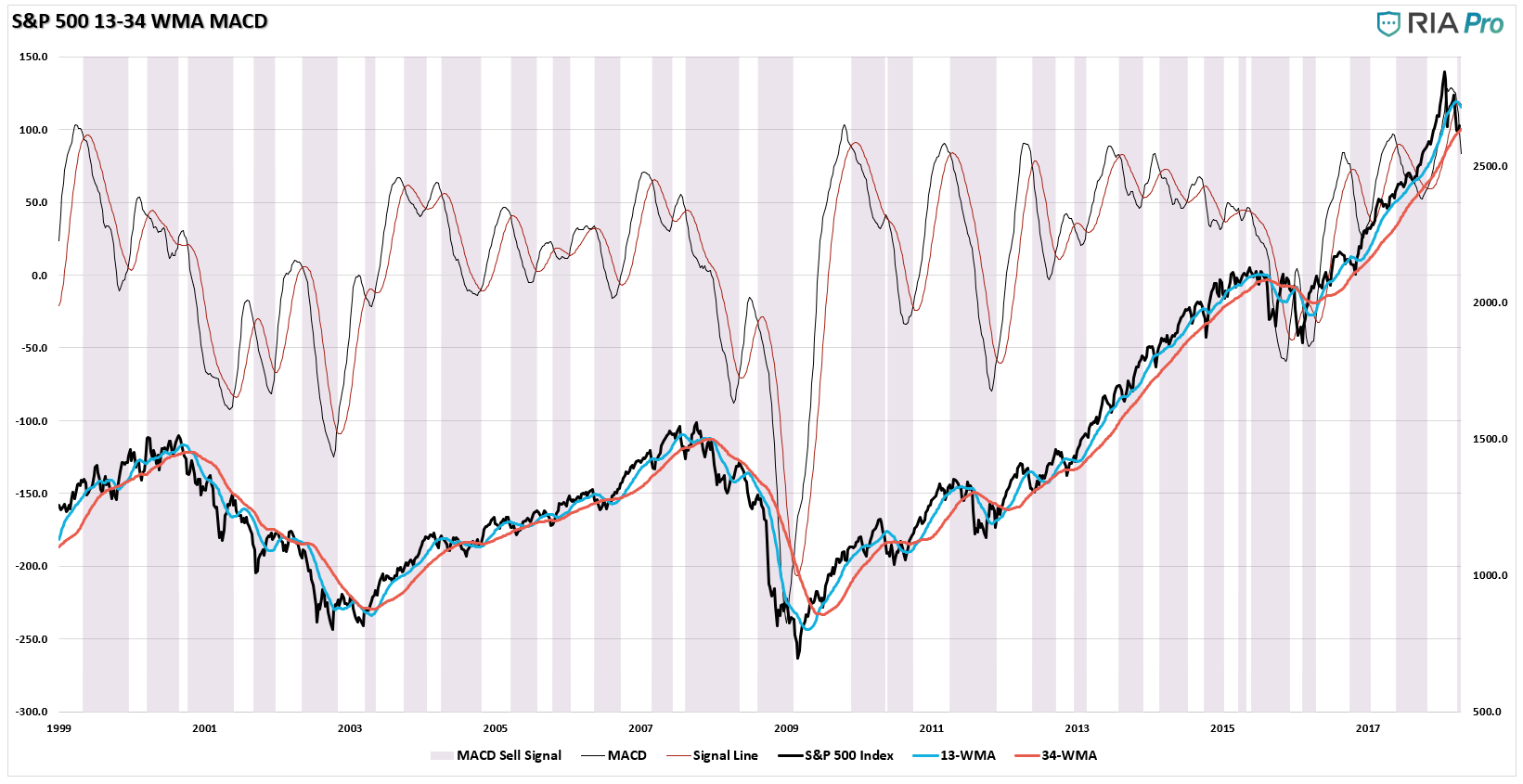

More importantly, the market currently remains on both a short and intermediate term “sell” signal. While those signals could certainly be reversed in the days and weeks ahead, historically, it has often paid to adhere to what those signals are suggesting. (The purple bars are when the MACD line is negative confirming a “sell signal”)

(I penned an article recently on the 200-day moving average and the primary question was “when do you get back in?” So, just to clarify, a “sell signal” suggests reducing risk to equities, when the signal reverses you increase risk to equities. Notice – it is not an “all out” or “all in” thing.)

As noted above, we remain a heavier in cash than normal until the market breaks out of the current downtrend and begins to reverse those signals. If the market breaks below the 200-dma, we will raise more cash and institute further hedges as well.

While holding cash will certainly weigh on short-term performance if the market rallies, I will gladly exchange that for longer-term outperformance by protecting investment capital.

More importantly, the real “bear market” is still coming.