Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

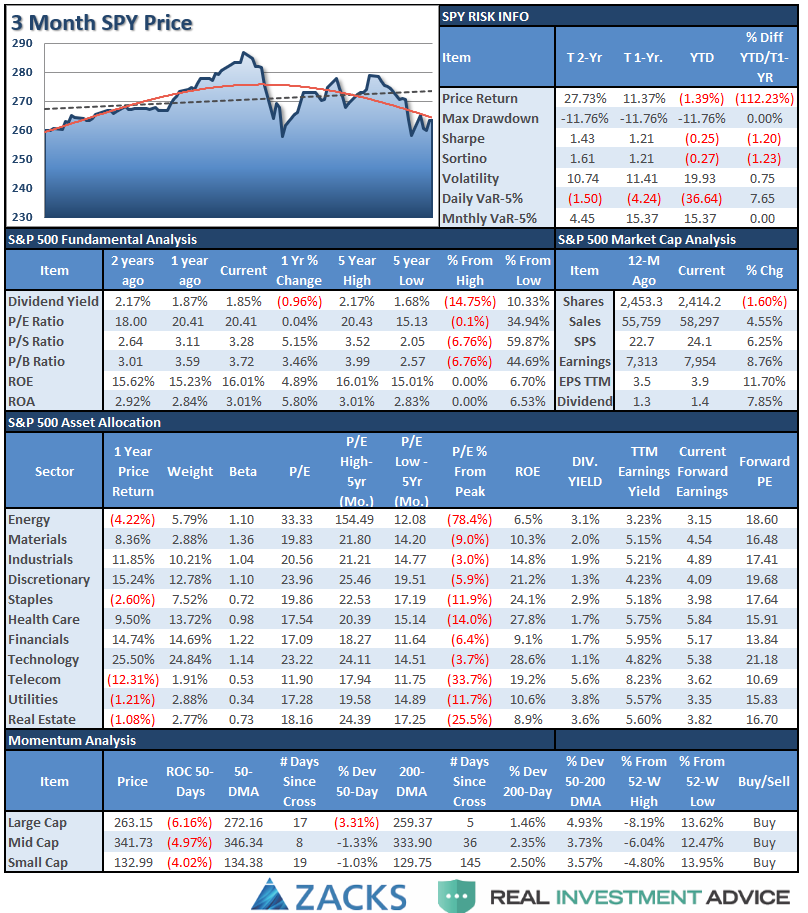

S&P 500 Tear Sheet

Performance Analysis

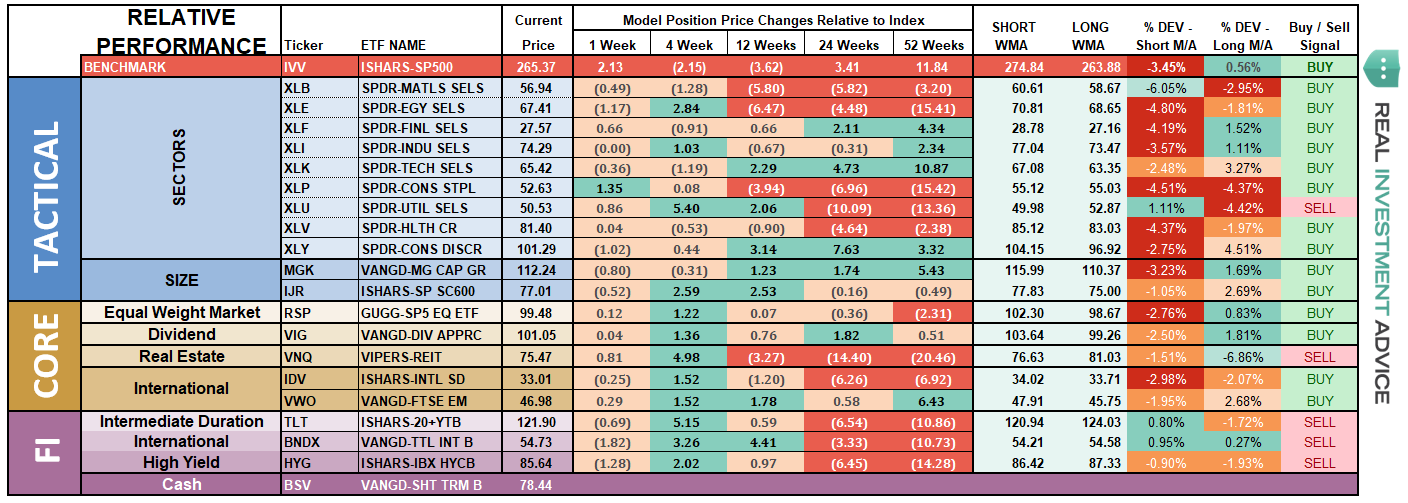

ETF Model Relative Performance Analysis

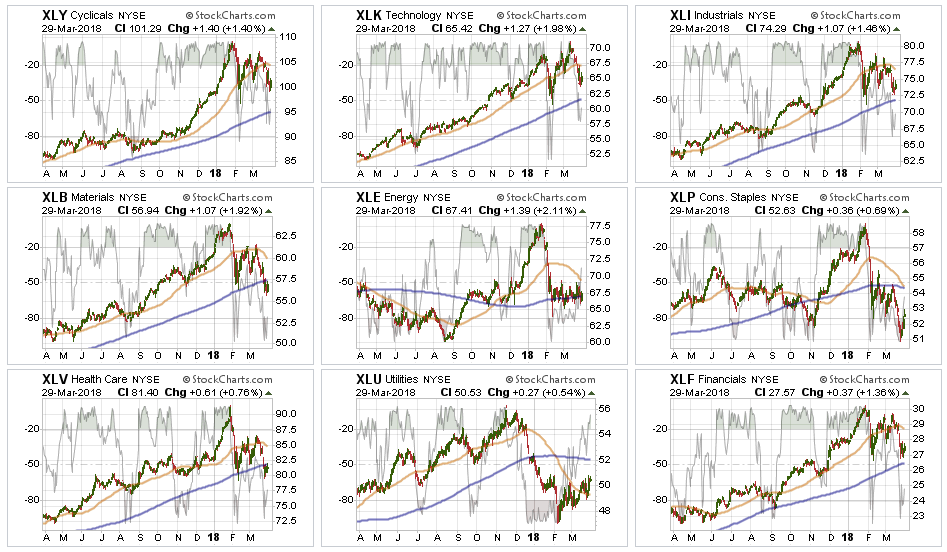

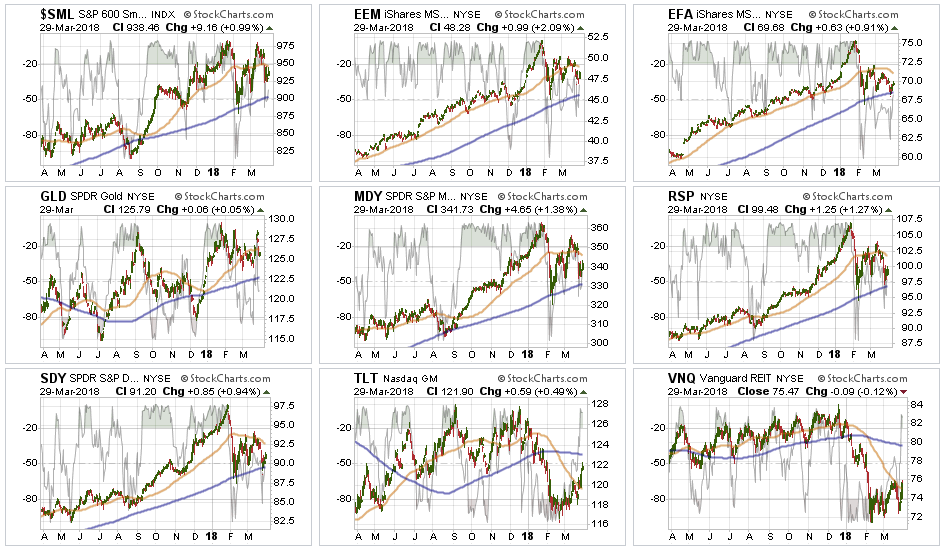

Sector & Market Analysis:

With the “sell signal” firmly in place on a short-term basis, the selling pressure has continued to suppress a rally in the market. Despite a rally last week, as we will discuss, there is little that has markedly improved since last week.

Discretionary, Technology, Industrials, and Financials all of these sectors have continued to remain below their respective 50-dma’s. But importantly, despite the drubbing of FaceBook and Amazon last week, Technology as whole remained supportive of the overall bullish trend. Furthermore, these sectors, while improving, are NOT oversold currently which provides enough room for a test of their respective 200-dma’s over the next couple of weeks. As I noted last week, it is a reasonable idea to take profits and reduce weightings accordingly.

Health Care, Materials, and Energy – we were stopped out of our small additional Energy trade with the previous break below the 200-dma, and continue to recommend under-weighting the sector for now. The push higher in oil prices is likely not sustainable and energy stock prices are likely reflecting the same. We also closed out our Materials and Industrials trade on “tariff” risks. Health Care has now also broken the 200-dma suggesting reducing weights there as well.

Staples – our stop level was triggered on Staples and we will be eliminating exposure to the sector on this rally. The sector is dangerously close to a moving average crossover which could pressure prices lower. Utilities have continued to under-perform in recent weeks, but have been improving as of late with a break back above the 50-dma. We are not recommending adding to the position yet, but we are watching to see what happens next. Stops are set at recent lows.

Small Cap, Mid Cap, Emerging Markets, International, Equal Weight, and Dividend indices all broke back down through their 50-dma with international stocks testing its 200-dma. Two weeks ago, we removed international and emerging market exposure due to the likely impact to economic growth from “tariffs” on those markets. That reduction helped hedge risk this past week. Dividends and Equal weight continue to hold their 200-dma and performed better than the S&P index as a whole as money rotated to Utilities in the “flight to safety” rotation.

Gold continues its volatile back-and-forth trade but remains confined to a downtrend currently. As of this past week, Gold is once again testing recent highs which IF gold can break out of this consolidation would be very bullish. We currently do not have exposure to gold, but if you are already long the metal, we previously recommended that while the backdrop overall remains bullish, the correctional phase continues so taking profits on rallies remains prudent.

Bonds and REITs over the last couple of weeks, these two sectors looked to have bottomed and initiated early “buy” signals. Hold positions for now as interest rates have started to recognize the economic weakness that has shown up in the data as of late.

Sector Recommendations:

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio/Client Update:

As I addressed at length this week, I still suspect an oversold rally to ensue over the next week or two. While we want to honor the current “bullish trend,” we are also well aware of the rising risks and still, for now, believe it is prudent to reduce equity-related risk on this rally.

If we reduce equity allocations, and the market repairs all of the technical damage and re-establishes the previous bullish trend, we will reallocate accordingly and increase equity exposure back to target levels. Our bigger concern, currently, remains the relative risk to capital if the 9-year old bull market begins a more meaningful correction process. As I noted, there is plenty of evidence to support the latter case.

With the rally this past week, we are going to give the market a bit more “running room” this coming week. As always, we prefer the market to “tell us” what it wants to do versus us “guessing” at it. “Guessing” generally never works out as well as planned.

It is crucially important the market maintains support at current levels and continues to rally next week. After having reduced exposure to “tariff” related areas a couple of weeks ago (materials, emerging and international markets), we will use any rally in the next week or so to further reduce equity risk exposure in portfolios. We will also look to add additional hedges to the portfolio on any rally that fails at overhead resistance.

We remain keenly aware of the intermediate “sell signal“ which has now been “confirmed” by the recent market breakdown. We will continue to take actions to hedge risks and protect capital until those signals are reversed.