Written by Lance Roberts, Clarity Financial

“With the market correction barely a month in the rear-view mirror, investors have jumped back into stocks in record numbers.

Stock-focused funds took in $43.3 billion in fresh cash over the past week, a new peak that reverses much of the angst over the past several weeks, according to Bank of America Merrill Lynch.”

Please share this article – Go to very top of page, right hand side, for social media buttons.

Despite the fact that market remains in a consolidation/correction process, as noted above, the media has already decided the “correction” is over and investors have bought it “hook, line, and sinker.”

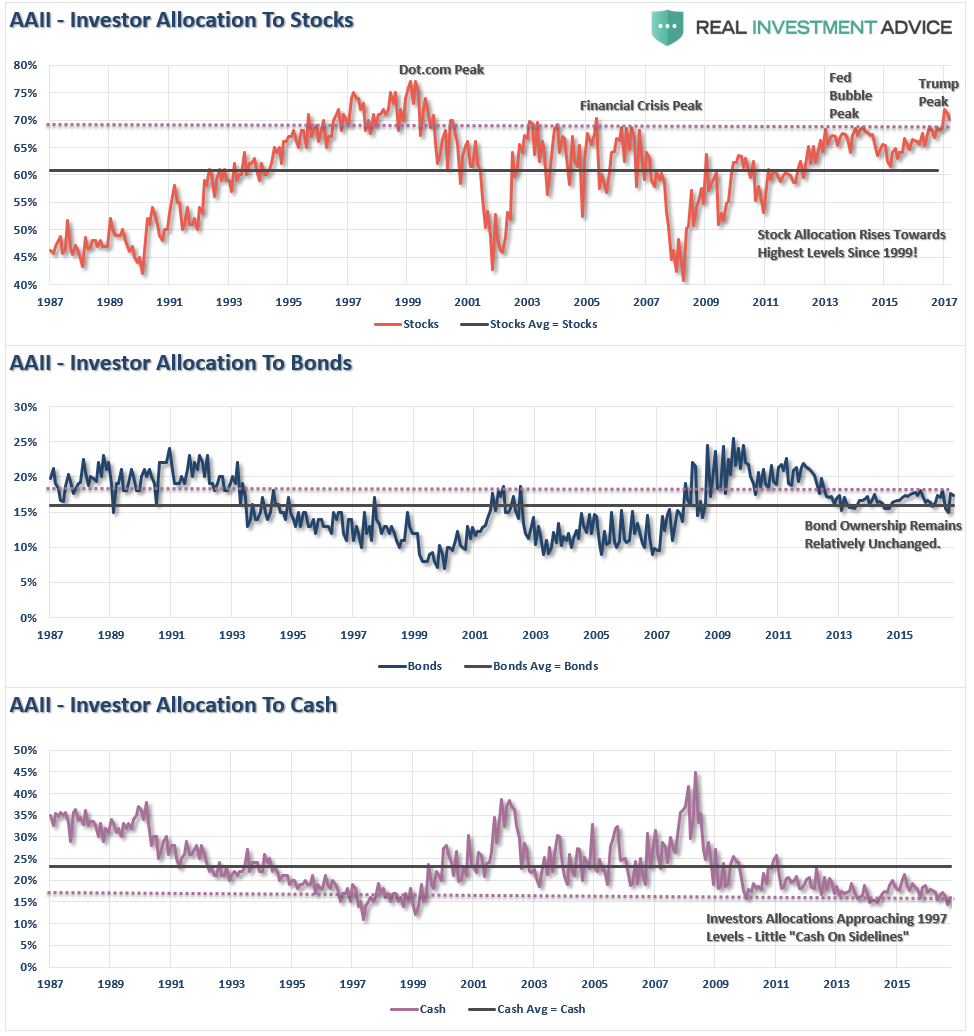

But then again, since the media’s “business” is to sell advertising, the best way to keep fund managers “paying” for ads is to make sure investors keep buying. Not surprisingly, since investors have been repeatedly “taught” to “buy the dip” over the last 9-years, it is not surprising to see they did just that. In fact, currently, investors are more long stocks today, and have the least amount of cash, since 1999.

“For the year, stock-based ETFs have pulled in $82.7 billion while bond funds have seen $11.7 billion in inflows, according to FactSet.”

But the media is always good at spinning a story. Read the following sentence carefully:

“Pessimism fell to its lowest level since the first week of 2018, at 21.3 percent a drop of 7.1 percentage points, according to this week’s reading from the American Association of Individual Investors Sentiment Survey.”

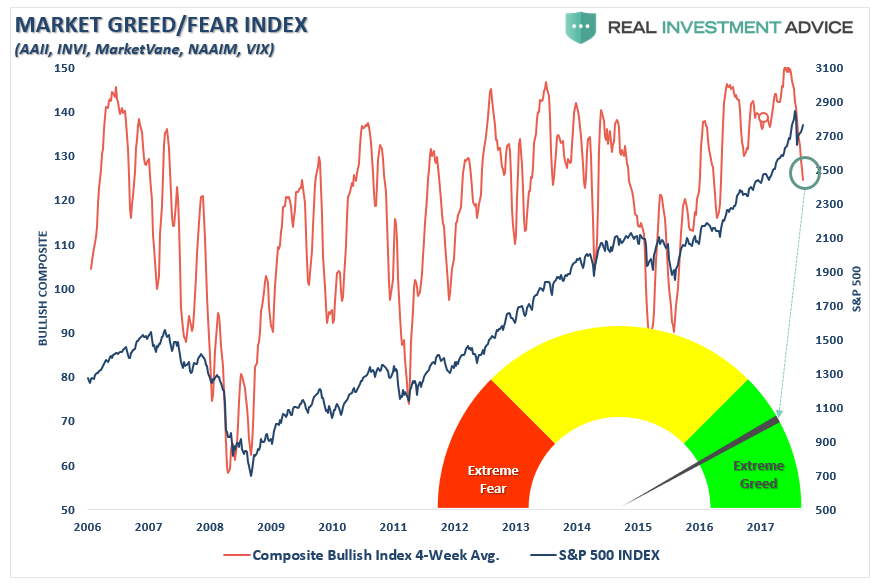

At first read, it sounds as if investors got markedly “bearish” on the markets during the correction. Actually, as shown below, bullish sentiment has only dipped from “extremely bullish” to just merely “excessively bullish.”

(The following chart is a composite index of various bullish sentiment indicators and the inverse of the VIX index)

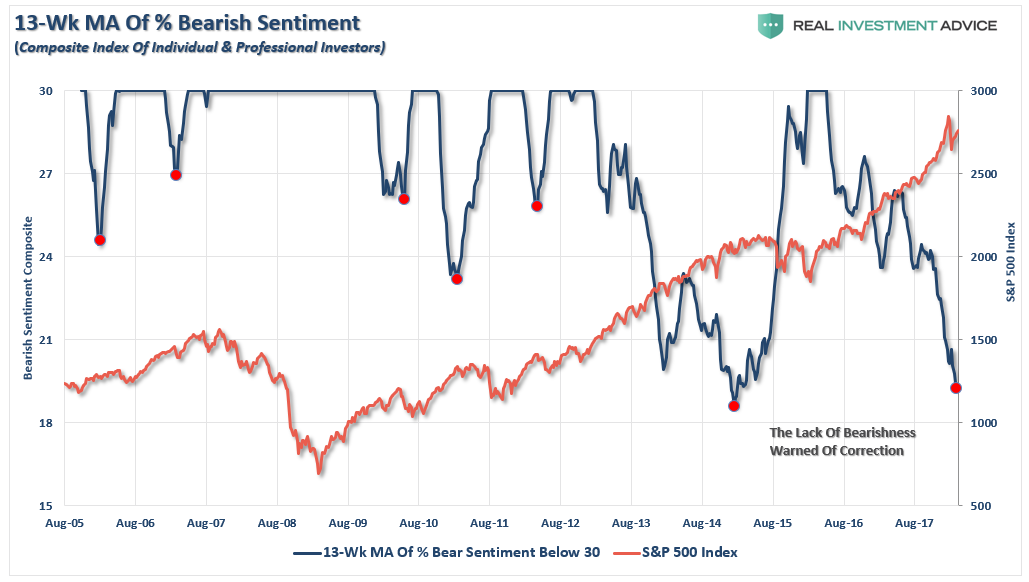

In fact, if we smooth the volatility by using a 13-week moving average, we find that we are once again near the lowest levels on record for a “lack of pessimism.”

But what is there to fear?

After all, every dip since 2009 has been a terrific buying opportunity. Why should this time be different?

Let me repeat something from this past Tuesday’s blog “Chart Of The Year,” in case you missed it:

“Yet the time of this unprecedented monetary experiment is coming to an end as we are finally nearing the point where due to a growing shortage of eligible collateral, the central bank support wheels will soon come off, resulting in gravity finally regaining control over the market’s surreal trendline.

Appropriately, this central bank handoff is also the topic of the latest presentation by Matt King, in which the Citi credit strategist once again repeats that ‘it’s the flow, not the stock that matters’, a point we’ve made since 2012, and underscores it by warning – yet again – that ‘both the world’s leading marginal buyers are in retreat.’ He is referring to central banks and China, the world’s two biggest market manipulators and sources of capital misallocations.”

With markets heavily leveraged, global growth beginning to show signs of deterioration, breakeven inflation rates falling, and liquidity support being removed – the markets have yet to recognize the change.

But when they do, the consequences to complacent investors have been nothing short of brutal.

Be sure to “look before you leap.”