Written by Lance Roberts, Clarity Financial

— this post authored by John Coumarianos

Financial Advisor Larry Swedroe recently wrote an essay called “The Four Horsemen of the Retirement Apocalypse” that should be required reading for anyone embarking on retirement and all advisors helping retirees.

Please share this article – Go to very top of page, right hand side, for social media buttons.

Basically, retirees, whether they and their advisors realize it or not, are staring four problems squarely in the face: historically high stock valuations, low bond yields, increased longevity, and increasingly expensive health care.

Low prospective returns, big prospective expenses

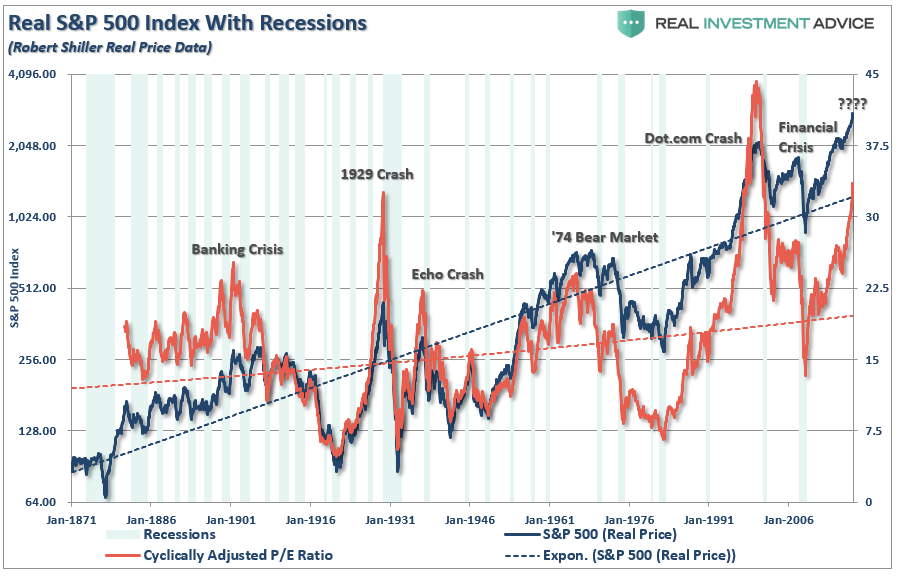

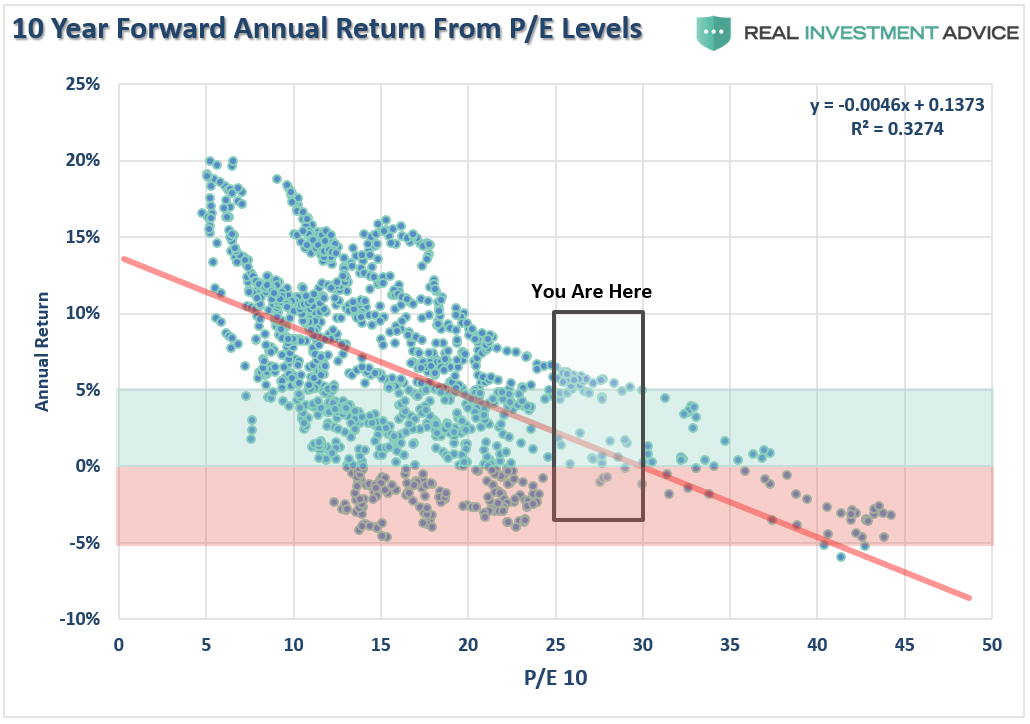

First stock valuations are high. The best gauge of the stock market’s valuation is the Shiller PE – current price relative to the past decade’s worth of real, average earnings. This is also called the “CAPE” or cyclically adjusted PE since it relies on a full decade’s, or what should be an economic cycle’s, worth of earnings. Its long-term average is under 17, and it’s currently over 30.

It has admittedly been over 20 for most of the past quarter-century, which means the average may be creeping up. After all, the today’s economy is different from the one in, say, the late 1920’s when electric utilities were the hot technology stocks. But, if there is a new normal, it’s likely not over 20.

A low-30s CAPE means a likely future real return of around 3% or a nominal return of around 5% from U.S. stocks. That’s decidedly subpar, or below, the 10% many advisors quote to their clients. Stocks have returned 10% or so over the last century, but they have endured periods of low returns such as from the mid-1960s to the early 1980s. Given the current valuation, it’s difficult to envision a stellar period for stock returns.

Let’s move from Swedroe to Jack Bogle for a moment. Bogle has another way of looking at stocks. Take the current dividend yield – around 2% – and add historical earnings-per-share growth – 4%-5%. That gets you to 6% or 7%. But then Bogle demands a speculative component to the valuation, which consists of estimating the future P/E ratio. Bogle thinks it’s wiser for investors to assume it will be meaningfully lower than it is today. All of this means stocks will likely produce a 4% real return, according to Bogle – only slightly higher than Swedroe’s 3% estimate.

Any way you look at stocks, it’s difficult to get anywhere near their long-term historical 6%-7% real return or 10% nominal return for the next decade. Only heroic growth and/or valuation assumptions get you there. Stocks can stay at a Shiller PE of above 30; anything is possible. But nobody should be baking that into their retirement assumptions.

Finally, foreign stocks are priced for better returns – but not much. Basically, stock investors don’t have anywhere to turn for the returns they’ve come to expect.

Let’s return to Swedroe and bonds. The 10-year U.S. Treasury is yielding a little less than 2.9% as I write. And Swedroe clearly takes the current yield-to-maturity of bonds to be a good approximation of their return. The iShares Investment Grade Corporate Bond ETF LQD is yielding 3.67%. Investors can’t get to 4% from here. Neither can they with foreign bonds.

Junk bonds are yielding a little more than 5%, but when historical loss rates (defaults and recoveries) are baked in, investors will be lucky to make more than they would on a 10-Year U.S. Treasury on them. And that means junk bonds are likely the worst bet in the bond world right now. Advisors pushing them on clients are arguably committing a kind of malpractice. (That’s my opinion, not Swedroe’s more diplomatic one, though he clearly also doesn’t think junk’s reward is worth its risk.)

Similarly, advisors baking in 7%-8% returns on a balanced portfolio are giving their clients faulty retirement plans. A financial planner who can’t make adjustments to 100-year return figures to fit the current moment, isn’t really a planner.

Next, Swedroe moves to longevity. Our current situation is much different than it was decades ago when people often used to collect social security for only a few years before dying. Now, as Swedroe says, “for a healthy couple, both 65, there is a 50% chance one spouse will live beyond 92 and a 25% chance one spouse will live beyond 97.” Here Swedroe praises deferred income annuities or what he calls “longevity annuities,” though it’s true that someone buying them now locks in a low rate of return.

The fourth horseman of the retirement apocalypse is increasing healthcare costs, especially those associated with dementia, the likelihood of which doubles every five years after 65. According to Swedroe, “the average out-of-pocket medical expenses a 65-year-old couple can expect to incur during retirement is estimated to be in the mid-$200,000 range to somewhere in the mid-$400,000 range. And that’s the average. Obviously, some will incur far greater expenses.”

Stop extrapolating historical returns, and consider some alternatives

After a statement about a possible fifth apocalypse – the viability of Social Security and Medicare – Swedroe gives some advice to financial planners. First, don’t extrapolate century-long historical returns. Instead, understand where valuations and yields are now on securities. Second, get some foreign stock exposure. When considering how much, start from the observation that the U.S. stock market is about 50% of the global stock market. Third, consider a deferred annuity. .Fourth, explore long-term care insurance, and make sure you’re taking proper account of longevity risk. Last, Swedroe recommends an alternative bond portfolio consisting of four funds in strategies previously available only to institutional investors to boost yield for those investors who simply need the extra yield. He thinks they are superior to junk bonds, and we’re inclined to agree that almost anything is.

We’ll be examining these funds in future posts. For now, investors and advisors should consider Swedroe’s remarks about low returns and high expenses in retirement carefully.