Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

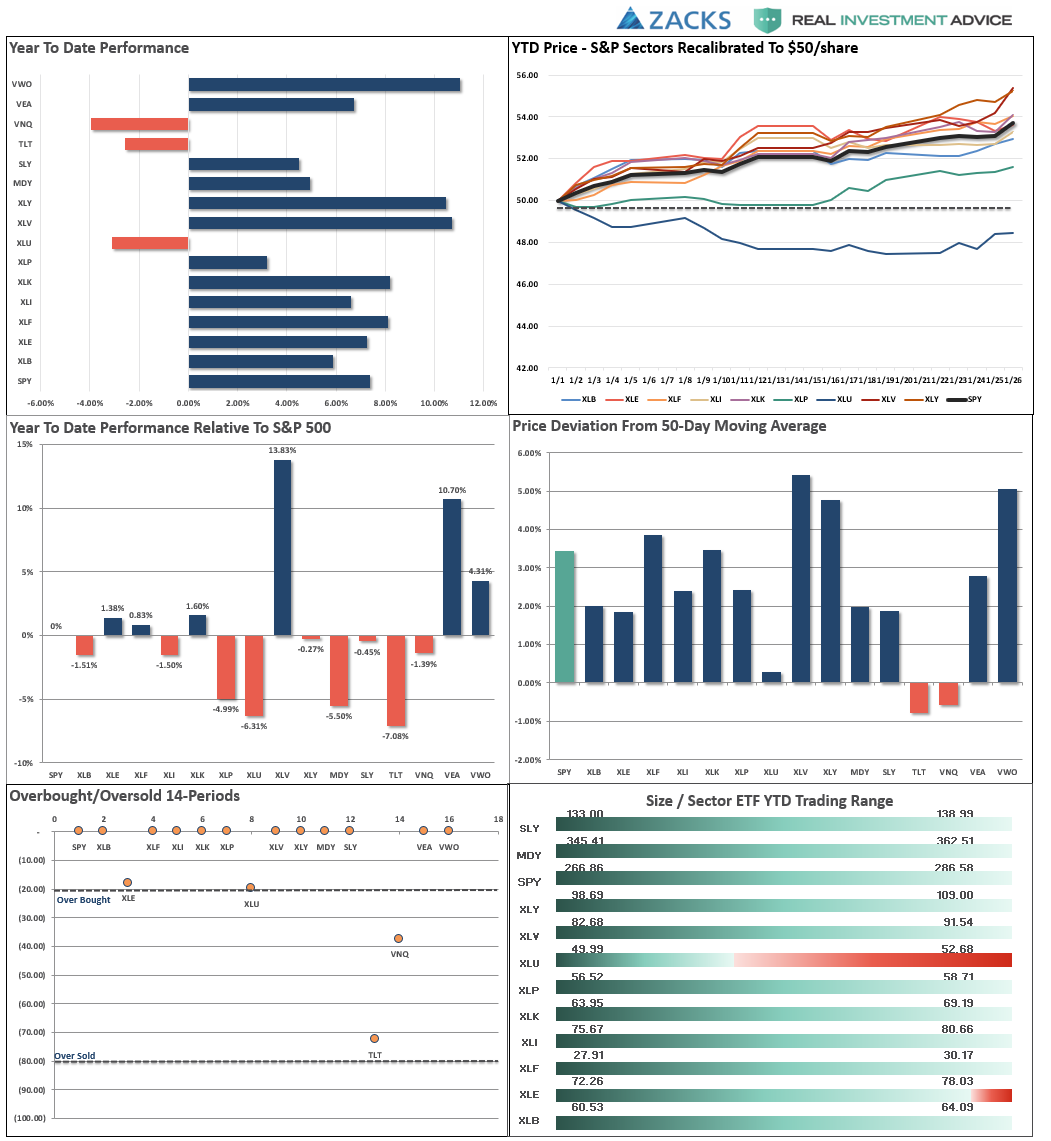

S&P 500 Tear Sheet

Performance Analysis

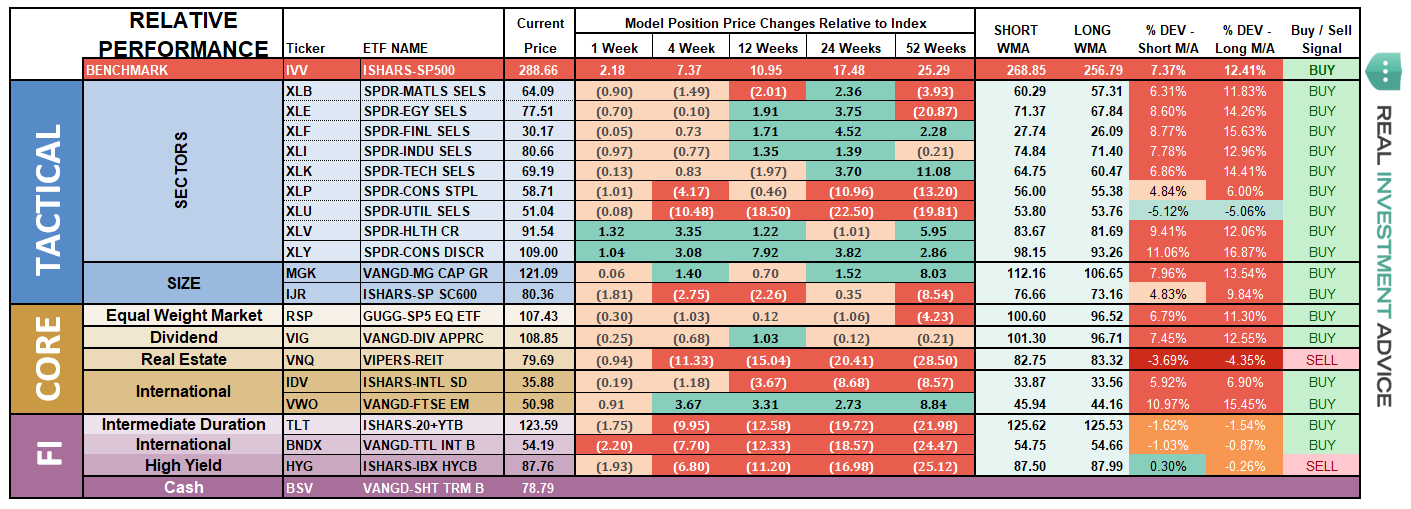

ETF Model Relative Performance Analysis

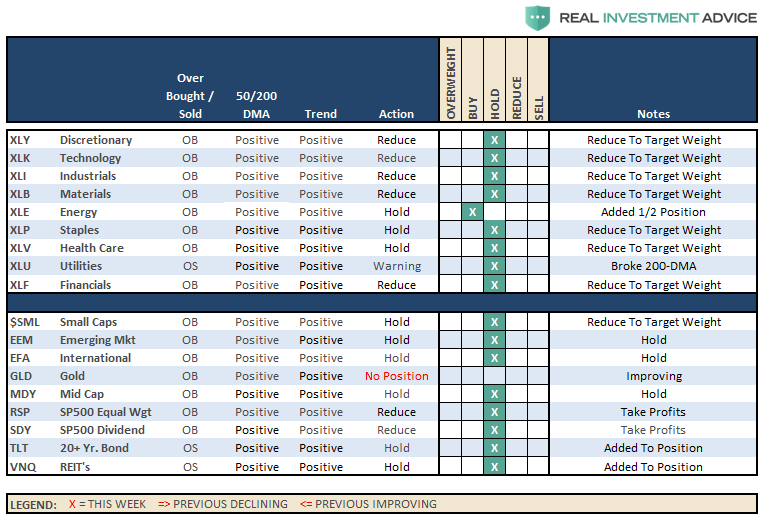

Sector & Market Analysis:

This is just getting a bit TOO extreme. Take a look at the sectors below. Every sector is pushing 2- and 3-standard deviations of longer-term moving averages.

This isn’t normal.

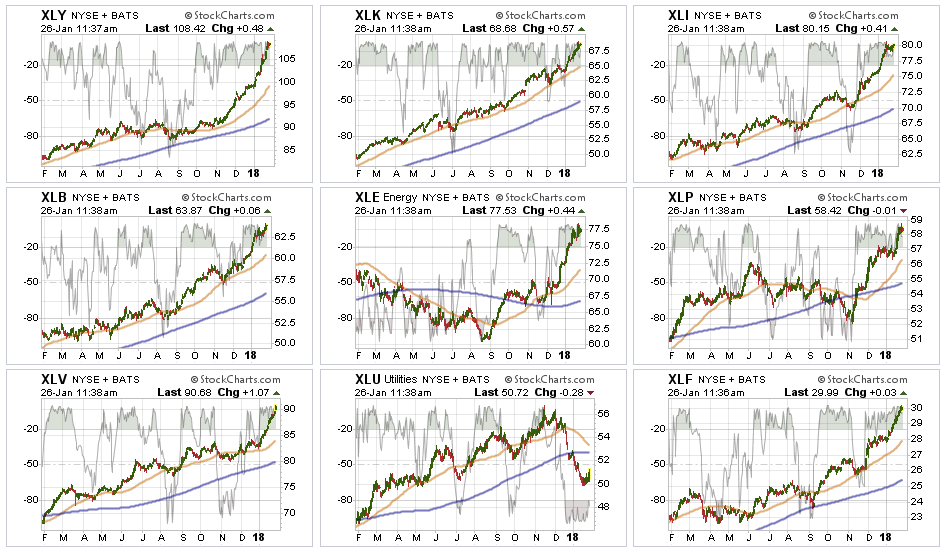

Every Sector Except Utilities – remain in full-fledged party mode again this last week with Staples catching up to the party as the chase higher continues. The massive overbought conditions in every sector, again except Utilities, needs to be reduced before a better entry opportunity will present itself. We are still long our positions but continue to hedge risk and rebalance opportunistically.

Energy – as I noted in December, the positive backdrop developed in the energy sector on a technical basis. We added one-half of a tactical trading position to portfolios last month which has paid off well. However, that trade has gotten way over-extended so look to take profits on any weakness. We are moving up our stop-loss levels as well.

Utilities, we remain long the sector for now and added some weight to the sector as a hedge against a risk-off rotation. With the sector very oversold, we did begin to see that start of an upswing this last week. We continue to look for a risk-off rotation soon to see a further pick-up in the sector.

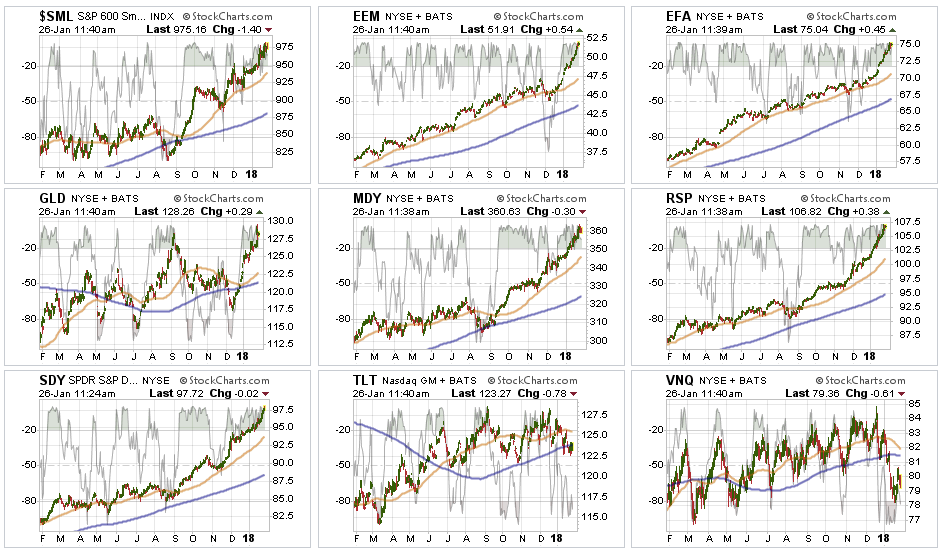

Small and Mid-Cap index trends are positive which keeps allocations in the markets but the extreme overbought conditions make adding exposure here riskier. Look for weakness to take profits and rebalance weights in portfolios.

Emerging Markets and International Stocks as noted below, we added some international exposure on the breakout following the recent pullback. The markets are extremely overbought on every front, so, as with virtually every other position, rebalancing portfolio weights and reducing some risk is prudent.

Gold – we are now fully on the lookout to add gold into portfolios on any pullback that somewhat reduces the current overbought conditions without violating important support levels. A rally in the dollar from currently extremely oversold levels will likely provide that opportunity.

S&P Equal Weight & Dividend Stocks – As noted previously, both of these positions have simply gone parabolic as money is chasing yield currently. We have moved up stops and are looking to take profits and rebalance accordingly.

Bonds and REIT’s – We remain long these sectors and did add to them recently on weakness as a hedge against a “risk off” rotation. Our conviction on these positions continues to rise, but we are still honoring our longer-term stop-loss levels.

Sector Recommendations:

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio Update:

Also, as noted four weeks ago, hedges were added to our portfolios. Given the parabolic rise in the markets, which has created massive extensions in price, we continue to maintain those hedges for now. We will add to them once a correction begins to ensue.

As far as portfolios go, we continue to maintain our current positions. As noted over the last few weeks, our most recent additions were Energy in mid-December and the Russell 2000 and Japan on recent breakouts three weeks ago.

While our hedges are under-pressure currently, they are small relative to the long-side of our portfolio. As always, we remain fully invested but are becoming highly concerned about the underlying risk. Our main goal remains capital preservation which is why we are de-risking portfolios where and when we can.