Written by Lance Roberts, Clarity Financial

— this post authored by Michael Liebowitz

In Bond Bears: Why Rates Won’t Rise Lance Roberts recently forecasted stable to lower bond yields in the months ahead. His argument is partially based upon a continuation of weak economic growth trends.

Please share this article – Go to very top of page, right hand side, for social media buttons.

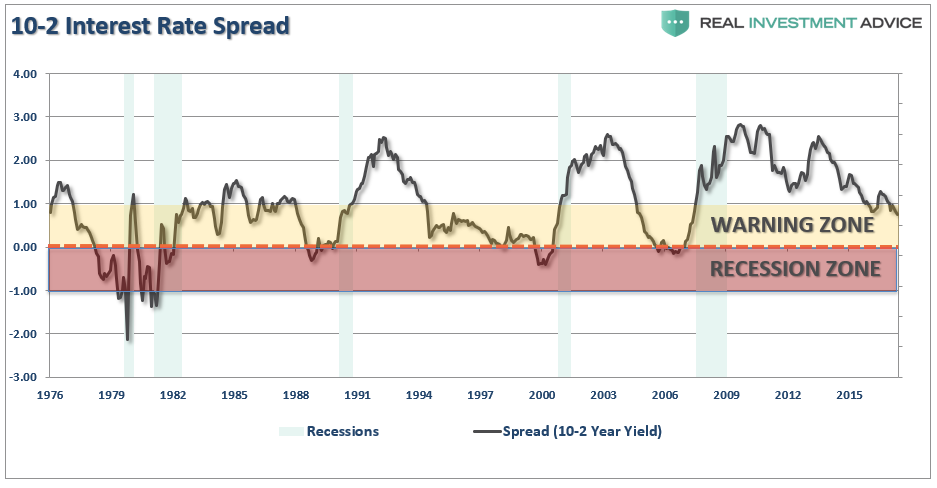

To support the forecast he presented a graph of the 2s-10s yield curve, or the difference between 2-Year U.S. Treasury yields and 10-year U.S. Treasury yields. As shown below the yield curve tends to flatten and ultimately invert (10yr-yields become less than 2yr-yields thus the curve goes below zero) as economic activity wanes and recession becomes imminent.

Currently, the 2s-10s curve sits in the “warning zone” and is at the lowest level since the financial crisis of 2008. This is possibly a sign that bond traders are concerned about future economic activity and if it continues to flatten, one that could spell trouble for the equity markets.

It is said stocks take the stairs up and the elevator down. That is a nice way of saying that when a market peaks it tends to fall much more impulsively than it rose. Prior to the last market correction (2008), the S&P 500 rose steadily for over five years. Those gains and more were erased in less than two years with the majority of losses coming between September and November 2008, when 41% of the index was wiped out.

Junk Debt

If we assume the next sell-off in stocks, like the previous few, will not be a gradual decline but a sharp drop lower, we must remain alert to signals that precede trend changes. The importance today is every bit as important as in 1999 and 2007, given that valuations stand at or near all-time highs and the risks of significant losses are potentially on par with loses in those periods. The yield curve is one such signal we should follow as recession tends to accompany lower stock prices.

Another such warning worth watching closely is the recent divergence between high yield debt and the S&P 500.

High yield debt, also known as junk bonds, are the publicly traded debt of companies rated as below investment grade (BB+/Ba1 or below). Simply, they have a higher level of default risk than investment grade bonds. It is because of this credit risk that some investors consider them a hybrid between equity and bonds. The higher yields offered by junk-rated companies and their tendency for greater price volatility makes their total returns more similar with equity returns than Investment-grade corporate debt and U.S. Treasuries. Investors of junk debt tend to do similar fundamental analysis as equity investors.

**Throughout this article the terms “junk” and “high yield” are used interchangeably. Both refer to below investment grade debt.

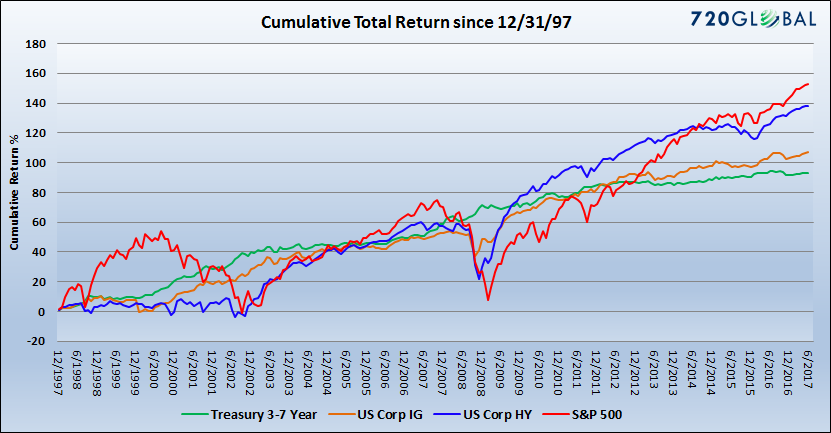

The graph below highlights the strong correlation between high yield bond and stock returns. Further explaining why investors think of high yield debt as having equity-like return traits. As shown the returns of high yield (blue) more closely resemble those of the equity market (red) than the returns of U.S. Treasury (green) or Investment grade corporate (orange) bonds.

Divergence

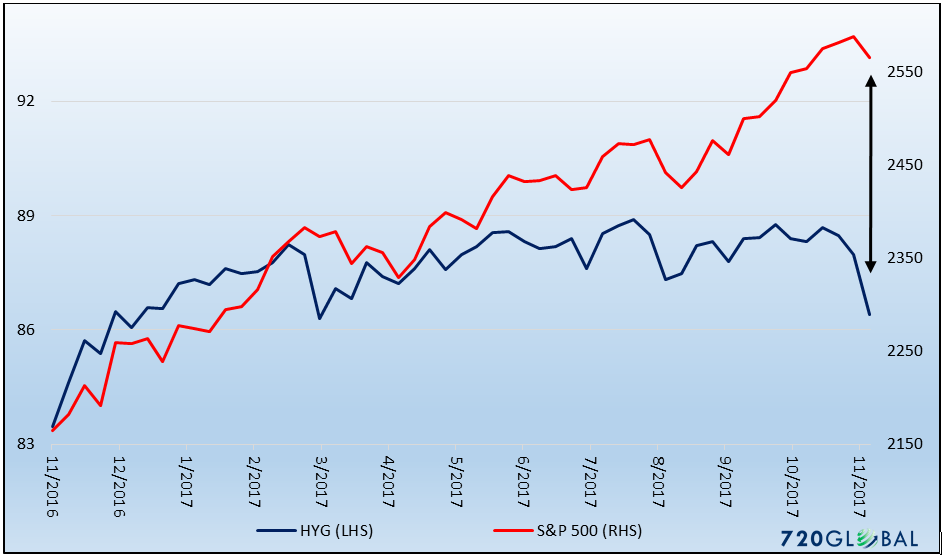

Over the past year, there has been a growing divergence between the price of the two most popular high yield ETF’s (JNK and HYG) and the S&P 500. Since January of 2010, the price changes of JNK and HYG have been approximately 65% correlated to the price change of the S&P 500. Recently the relationship is fraying. Over the past six months, the correlation has dropped in half to 32%. The lack of correlation is not only evident in the graph below but also in year to date returns. Thus far in 2017, the S&P 500 is up over 13% while the two junk ETF’s are down slightly.

Recent poor performance of the high yield ETF’s is the result of spread widening between the Barclay Junk Index and the U.S. ten year Treasury note. When this spread widens, the yield on the junk index rises by more than the yield on the Treasury note. This occurs when investor concerns about economic weakness and ultimately credit risk elevate. The current spread of the Barclay Index to ten-year Treasury yields is 3.36% which is well within recent ranges and low on a longer-term basis. In fact, it is sitting on top of the year to date average spread. While a longer-term chart would not cause much alarm, it is worth noting that the spread has increased 40 basis points (or 0.40%) over the last four weeks.

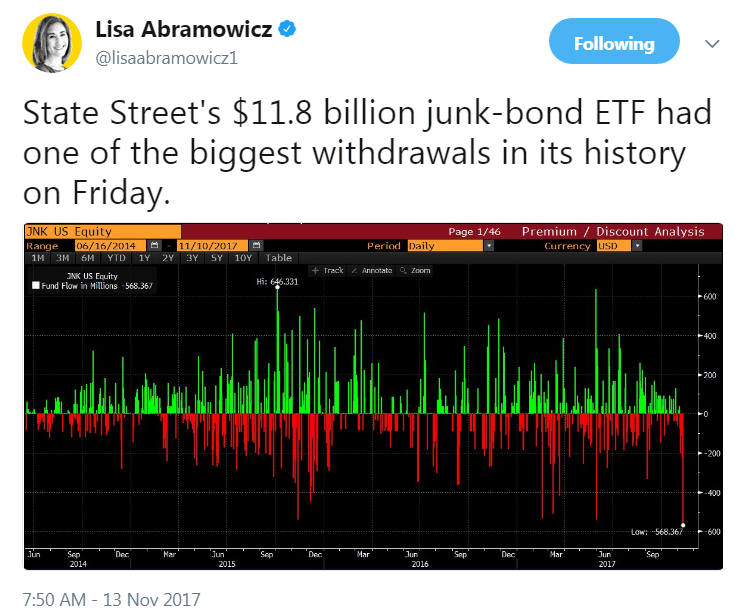

Of further concern is the following tweet and graph from Lisa Abramowicz of Bloomberg:

Summary

Historically bond traders have been more in tune with economic turning points than equity traders. It, therefore, goes without saying that equity investors should look for clues in the fixed income markets. Unless one thinks it is different this time, fixed income tends to lead equities.

The yield curve chart and relative weakness in the high yield sector are benign signals at the moment. While neither is flashing red, they certainly should be followed. We will continue to track these and many other fixed income and equity technical indicators for increased signs of a potential reversal in the equity markets. As they say “Stay Tuned.”