Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

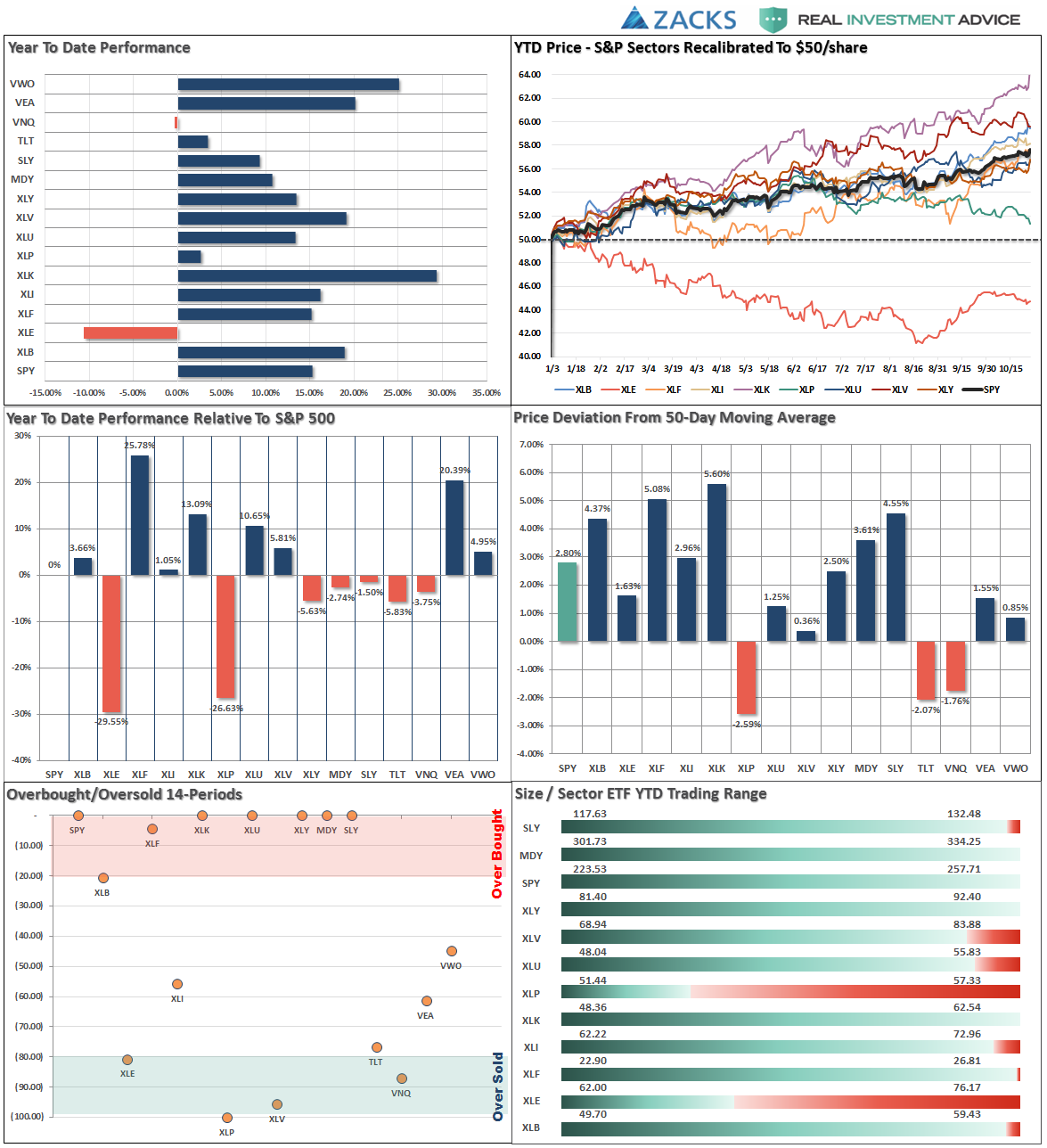

S&P 500 Tear Sheet

Performance Analysis

ETF Model Relative Performance Analysis

Sector & Market Analysis:

This past week, the bull market continued its advance, although a bit more wobbly as volatility picked up last week. With bullish sentiment still pushing extremes, there seems to be little of concern of investment risks currently as the year-end approaches and the “seasonally strong” period of the year goes into full swing.

Technology and Discretionary – surged higher on Friday as money chased the few stocks that grossly overweight these sectors (FB, AMZN, GOOG, MSFT) as noted above. However, despite the relatively narrow lead, the sectors did push to new highs keeping money allocated accordingly. However, some profit taking is warranted to rebalance risk.

Staples reiterating last week’s comment:

“Staples are showing significant weakness. Reduce exposure with the break of the 200-dma for now.”

Basic Materials, Financials, and Industrials stagnated last week but remain exceedingly overbought with valuations stretched. Rebalance risks and allocations accordingly.

Healthcare has slipped back to its 50-day moving average an bounced off that support on Friday. The trend remains positive currently, but watch for a violation of the support to signal a potential shift in portfolio weightings. Move stops up to the September lows for now.

Energy as I noted last week:

“While the underlying technicals are beginning to improve, the sector must stay above the 200-dma while working off the extremely overbought condition that currently exists.”

On Friday, the sector bounced off of the 200-dma as oil prices finally broke above $52/bbl. With the 50-dma now having turned back up, and approaching a cross of the 200-dma, we are becoming much more interested in adding energy back into portfolios after having been out of the sector since 2014.

Utilities, we remain long the sector and have moved stops up to the 50-dma. Trends remain positive and interest rates have likely peaked for the current advance.

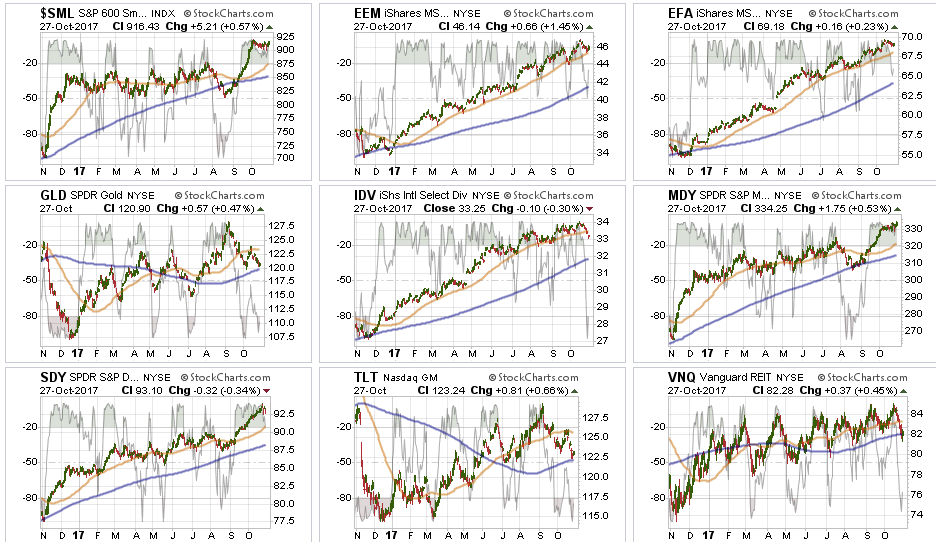

Small and Mid-Cap stocks have stalled over the last couple of weeks and remain extremely overbought. Stops should be moved up accordingly. We previously took some gains out of these sectors but remain long for now.

Emerging Markets and International Stocks have shown some weakness as of late but remain in a bullish trend overall. We remain long these markets for now but have moved up stops accordingly.

Gold – I noted previously the failure of precious metals to break back above the 50-dma. With the complete absence of FEAR of a potential crash, gold has temporarily “lost its luster” as a safe haven. We continue to watch the commodity currently, but remain on the sidelines for now.

S&P Dividend Stocks, after adding some additional exposure recently the index managed an extremely strong advance which ended last week as market participation narrowed sharply. We are holding our positions for now with stops moved up to $92. Take some profits and rebalance accordingly. Dividend stocks have gotten WAY ahead of themselves currently as the yield chase continues.

Bonds and REIT’s took a hit this week as “tax reform” moved forward and the expectations for higher inflation, wages, and economic growth pushed rates higher. While the economic benefit from tax reform is “WAY OVERSTATED,” we will continue to add more exposure if rates push towards 2.5-2.6% which is our target for this reversal. Both of these sectors are VERY oversold.

Sector Recommendations:

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio Update:

No changes this past week.

We used the pop in interest rates to move cash management accounts, and larger cash holdings, into our cash allocation strategy providing for better yields. We also added some new bond exposure to accounts and are looking for additional opportunities if rates push higher over the next couple of weeks. As noted our target for the current advance, based on tax reform “hopes,” is the 2.5-2.6% range.

We remain extremely vigilant of the risk that we are undertaking by chasing markets at such extended levels, but our job is to make money as opportunities present themselves. Importantly, each week we raise trailing stop levels and continue to look for ways to “de-risk” portfolios at this late stage of a bull market advance.

As always, we remain invested but are becoming highly concerned about the underlying risk. Our main goal remains capital preservation.