by Lance Roberts, Clarity Financial

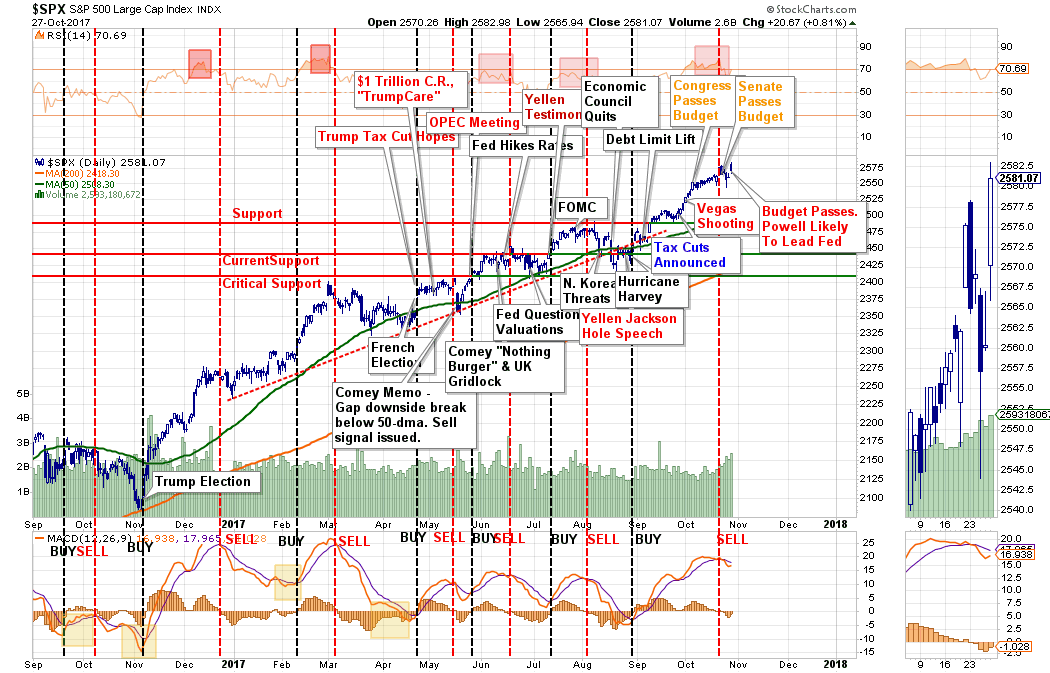

In last week’s missive, I discussed the “seemingly impervious advance” being driven by the advancement towards “tax reform and tax cuts.”

“The last leg higher has been directly responsive to the ramp up in the political “marketing surge” surrounding “tax cuts and tax reform“.”

Please share this article – Go to very top of page, right hand side, for social media buttons.

“With the House having already passed their respective budget resolutions, late Thursday, the Senate passed a budget blueprint for the next fiscal year. With both of the ‘budget resolutions’ in place, it was seen as clearing a hurdle to the goal of overhauling the tax code.

This is not new, of course, as the entire rally for the markets since the election has been driven by hopes of lower taxes, despite disaster, floods, fires and Central Bank threats of liquidity extraction.”

The passage of the budget by the House Of Representatives this past Thursday clears the deck for the advancement of tax cuts and reform. While getting a bill written will be difficult, there is a high degree of motivation to get the bill passed by Christmas especially with 50-Republicans up for re-election next November.

Or, it could be the next Fed Chairman as my partner, Michael Lebowitz, in another article to be published this week by GEI.

Or, you can just say it was earnings driven.

Whatever reason you want to subscribe to the advance this past week is fine. The reality is the bulls are clearly in charge which keeps us allocated to towards equity risk currently.

It is worth noting, that just as we saw during the run-up in the markets in 2014 and into 2015, the participation rate, as measured by the number of stocks trading above their respective 50 and 200 day moving averages, were declining which signaled a deterioration in participation. That deterioration eventually led to the decline in late 2015 and early 2016.

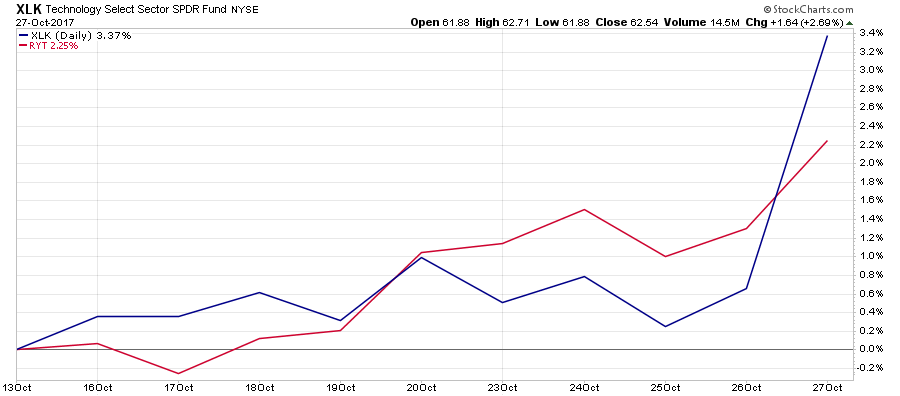

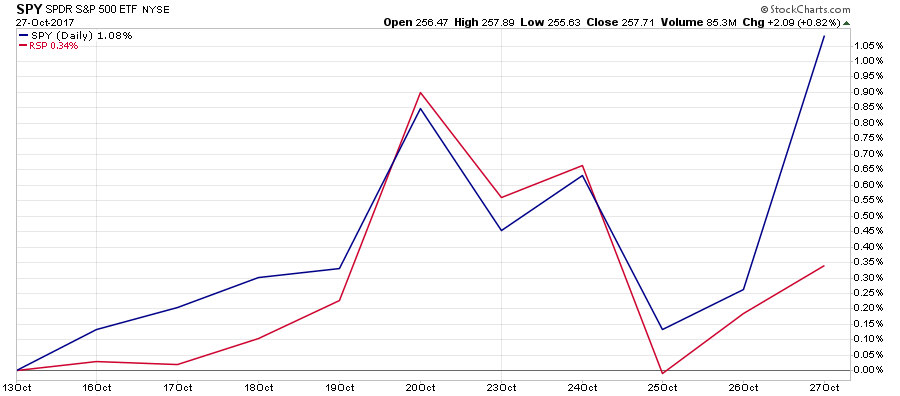

Currently, even as the market has made a seemingly unstoppable advance this year, the breadth of the advance has once again narrowed markedly.

This was clearly noticeable on Friday as the 5-largest technology stocks. by market cap. were the primary contributors to the advance.

You can see this more clearly here by looking at the difference between the Technology Sector XLK (market-cap weighted) and RYT (equal-weight).

Not surprisingly, since Technology makes up near 1/4th of the S&P 500 index, the surge in the 5-major Technology stocks magnified the performance of the S&P 500 Index ETF SPY (market-cap weighted) versus RSP (equal-weighting).

With earnings growth very weak for the overall S&P 500 index so far this quarter, the markets well ahead of fundamentals, as I discussed on Tuesday, it just makes sense to remain a bit more cautious currently particularly as the Fed begins to try an “reverse course” on monetary policy.

That doesn’t mean “sell everything” and hide in cash.

It does mean taking some time to review and understand the type and amount of risk you have undertaken in your portfolio and make some adjustments by rebalancing.

We have had one of the longest stretches in history without a 3% correction. That statistic alone suggests we are closer to one than not as “all things must end.” However, given the length of time we have gone without a correction also suggests the next correction will be both larger, and more painful, than currently anticipated.

Taking some actions today will ensure that you don’t make poor, emotionally driven, investment decisions in the middle of that correction that exacerbates the effects of a correction.