Written by Rick Ackerman, Rick’s Picks

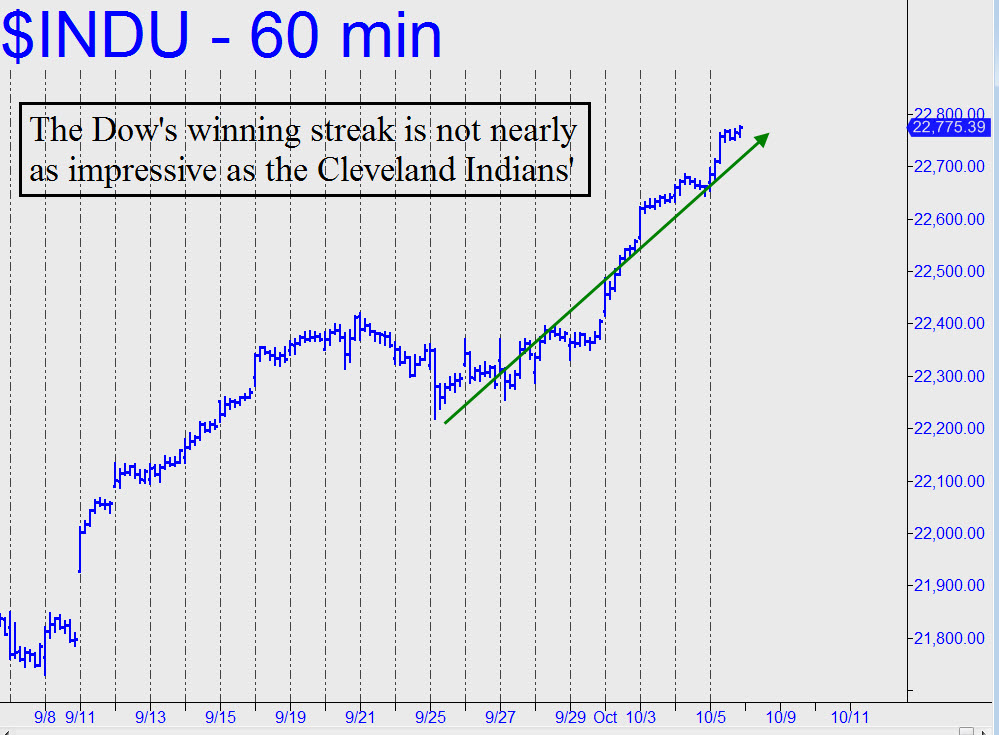

Market’s Hot Streak Still Lags Cleveland’s

The Dow Industrials rose on Thursday for an eighth straight day – a rare feat, although not nearly so rare as the Cleveland Indians’ 22 straight victories this past season. In fact, the Dow has had nearly a dozen streaks lasting eight days.

Please share this article – Go to very top of page, right hand side, for social media buttons.

What is the significance of this latest one? Mainly, that nearly everyone with money in the stock market made a little more of it the easy way. Much as they’ve been doing for eight-and-a-half years. In a bull market, it would seem, we are all rentiers with a steady stream of passive income derived from our respective chunks of the rock.

There are quite a few more of us with skin in the game than you may have imagined. We’ve all heard that “the public” has yet to go all in. In fact, collectively we are in stocks up to our eyeballs, according to Peter Eliades, editor and publisher of Stockmarket Cycles. In the latest edition of his newsletter, Peter includes a chart that shows stocks as a percentage of household financial assets. Other than during the years of the dot-com boom, readings are as high as they have been at any time during the last 65 years.

‘Most Overvalued Market in History’

In the same newsletter, he serves up an interesting quote from stock a colleague, John Hussman:

“What investors presently take as a comfortable environment of pleasant market returns and mild volatility is actually, quietly, the single most overvalued point in the history of the U.S. stock market.”

Peter notes:

“Don’t make the mistake of thinking that Hussman’s parameters for market valuations are based on simple P/E ratios or other orthodox valuation parameters,” “He has made a strong case that his valuation methodology is capable of assessing the markets potential over a following 10 to 12 year period. He uses a ratio of nonfinancial market capitalization to corporate gross value-added which includes estimated foreign revenues and which he describes as essentially measuring corporate revenues without double counting intermediate inputs. Sounds a little complicated, does it? Indeed, it may be, but that model is now calling for a 10 to 12 year annualized return on the S&P around the zero level. Compare that to a historic return of close to 10%, including dividends, and you should be able to glean what a miserable decade or more his valuation model foresees.”

If you are not a subscriber, click here for a free two-week trialthat will allow you to see the tout, and also to enter the Rick’s Picks chat room, where great traders from around the world swap timely ideas 24/7.