Written by Lance Roberts, Clarity Financial

On Wednesday, the Federal Reserve announced the latest decision by the Federal Open Market Committee with respect to monetary policy.

Please share this article – Go to very top of page, right hand side, for social media buttons.

That decision contained two primary components:

- No rate hike currently, although, as expected, announcements of further rate hikes in the future, and;

- The beginning of the process to cease reinvestment of the Fed’s balance sheet.

The announcement was notable for two reasons:

- The Fed did NOT hike rates because the underlying economic data, and, in particular, the inflation data, suggests the economy is too weak to absorb a further increase currently, and;

- The unwinding of the balance sheet is generally believed to be bullish for stocks.

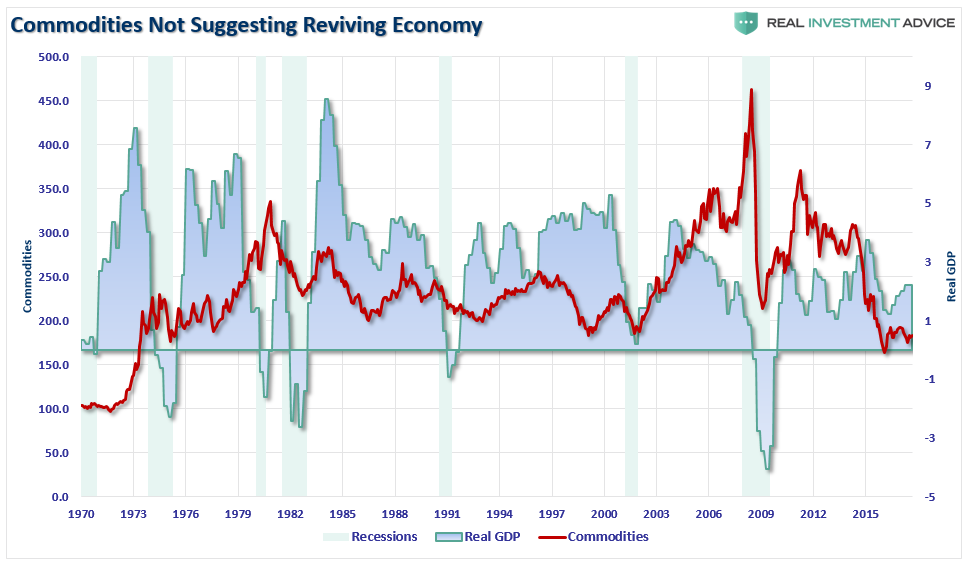

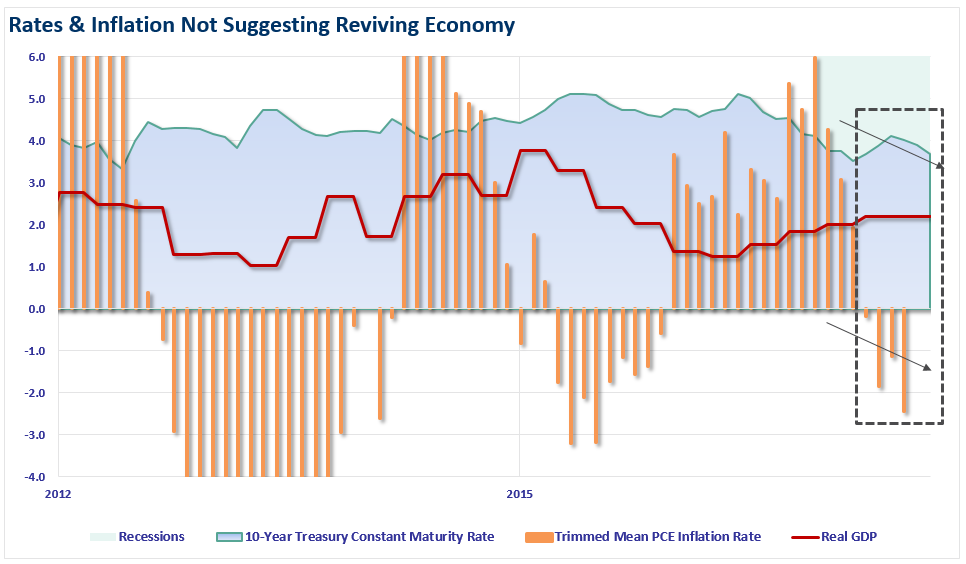

It is specifically the second point I want to address today, although, as shown below, commodities, PCE inflation, and interest rates currently suggests there is downside risk to current economic projections.

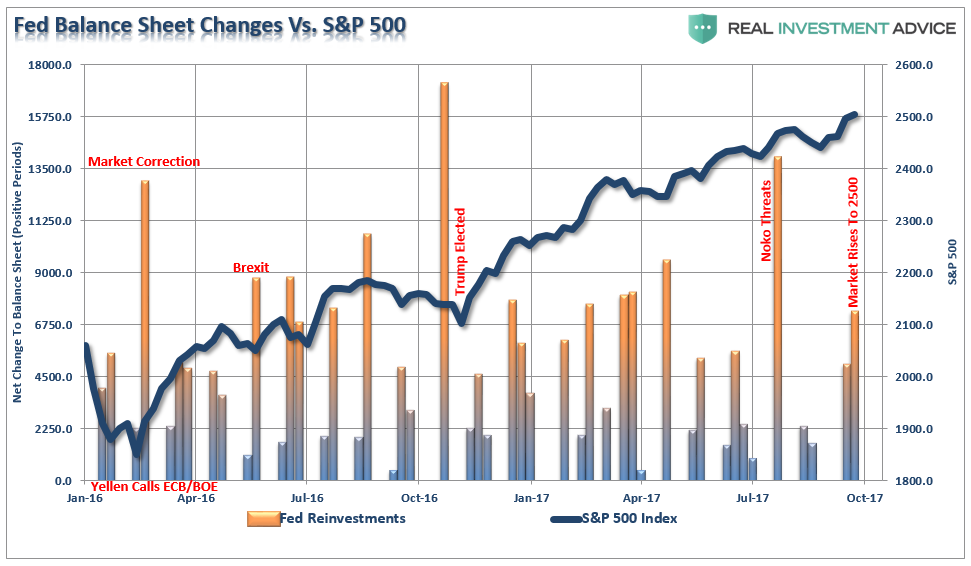

As I discussed on Friday, while the Fed talks a good game about a strengthening economy, improving jobs and rising asset prices, it is interesting to see the “coincident timing” of the Fed’s reinvestment of their balance sheet.

With that in mind here is the observation to consider.

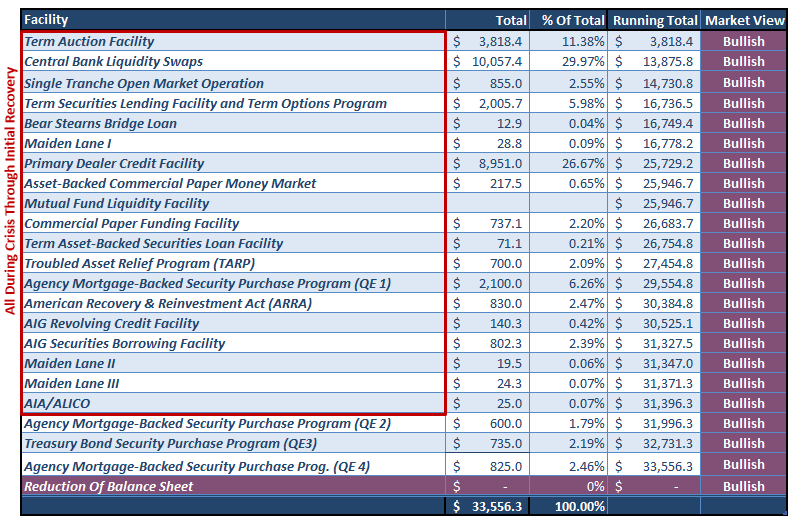

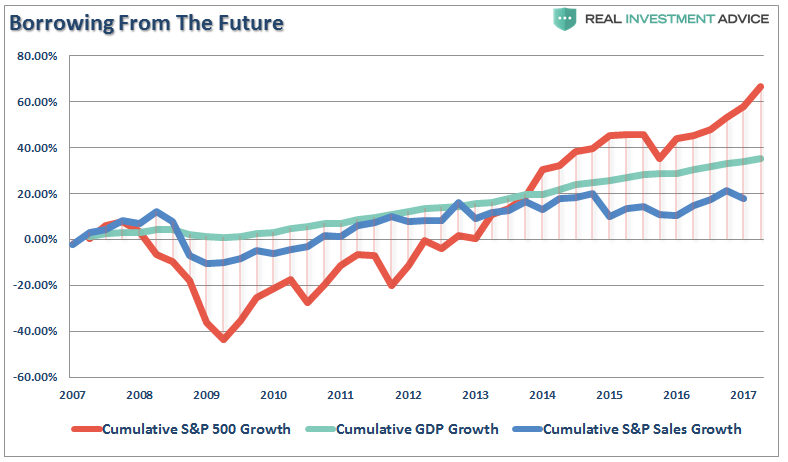

As shown in the table below, since 2009, there has been clear evidence that unbridled Central Bank interventions directly supported the market’s advance. All them considered “bullish” for asset prices.

Of course, after $33 Trillion in liquidity injections, bailouts, and supports, it should not be surprising that asset prices have been elevated well beyond the underlying growth of the economy or corporate revenue.

Furthermore, the ROI on those investments have been poor at best with each $1 of injections yielding just a $0.063 return economically speaking.

Now, ironically, despite the clear evidence of the support for the markets provided by near zero-interest rate policy and trillions in monetary injection, it is believed that “unwinding” those supports will have “no effect” on the market.

Apparently, it doesn’t matter what the Fed does, it’s “bullish.”

But let’s be very clear about one thing.

The Fed does NOT honestly believe in the strength of the recovery, that inflationary pressures are present OR that employment is as strong as stated.

It’s actually quite the opposite.

IF they believed in the strength of the economic data, as they suggest following their regular meetings, they would have been increasing rates and reducing the balance sheet in 2010 as growth exploded from the recessionary lows. But they didn’t.

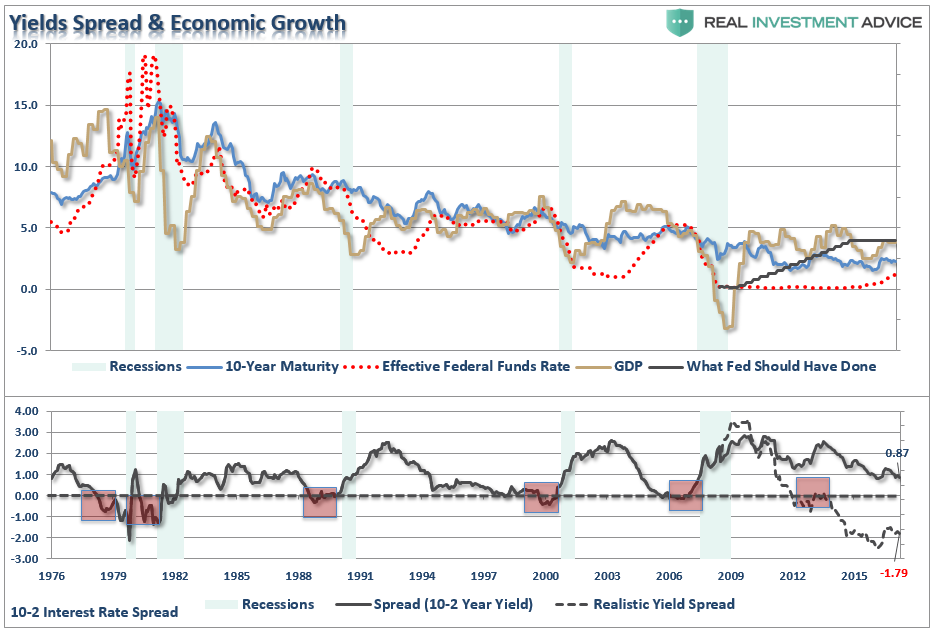

(The chart below shows 10-2 year rate spread and Fed Funds. Note, historically, when the Fed has started hiking rates, it was NOT the beginning of an economic expansion, but rather the end.)

Nor did they hike rates in conjunction with repeated liquidity injections from their ongoing balance sheet expansions. Such action s should have been the case as the liquidity flows would have offset the drag from higher borrowing costs.

But they didn’t.

The reason they are contracting the balance sheet now, and hiking rates, is due to the realization we are likely closer to the next recessionary period than not. The 10-2 year spread at just 0.87 as of the end of August (using monthly data) suggests the same.

“Unfortunately, what the Federal Reserve is quickly realizing is they have become trapped by their own ‘data-dependent’ analysis. Despite ongoing commentary of improving labor markets and economic growth, their own indicators have continued to suggest something very different.

Now they are simply considering abandoning those tools.

Is this a sign they have lost control of monetary policy?

Probably.

Will this ultimately lead to a policy misstep the disrupts the financial, and most importantly, the credit markets?

Definitely.

Why do I say that? Because there have been absolutely ZERO times in history that the Federal Reserve has begun an interest-rate hiking campaign that has not eventually led to a negative outcome.

While the Federal Reserve clearly should not raise rates further in the current environment, it is clear they will remain on their current path. This is because, I believe, the Fed understands that economic cycles do not last forever, and we are closer to the next recession than not. While raising rates will accelerate a potential recession and a significant market correction, from the Fed’s perspective it might be the ‘lesser of two evils.’ Being caught near the ‘zero bound’ at the onset of a recession leaves few options for the Federal Reserve to stabilize an economic decline.”