Written by Lance Roberts, Clarity Financial

Data Analysis Of The Market and Sectors For Traders

Please share this article – Go to very top of page, right hand side, for social media buttons.

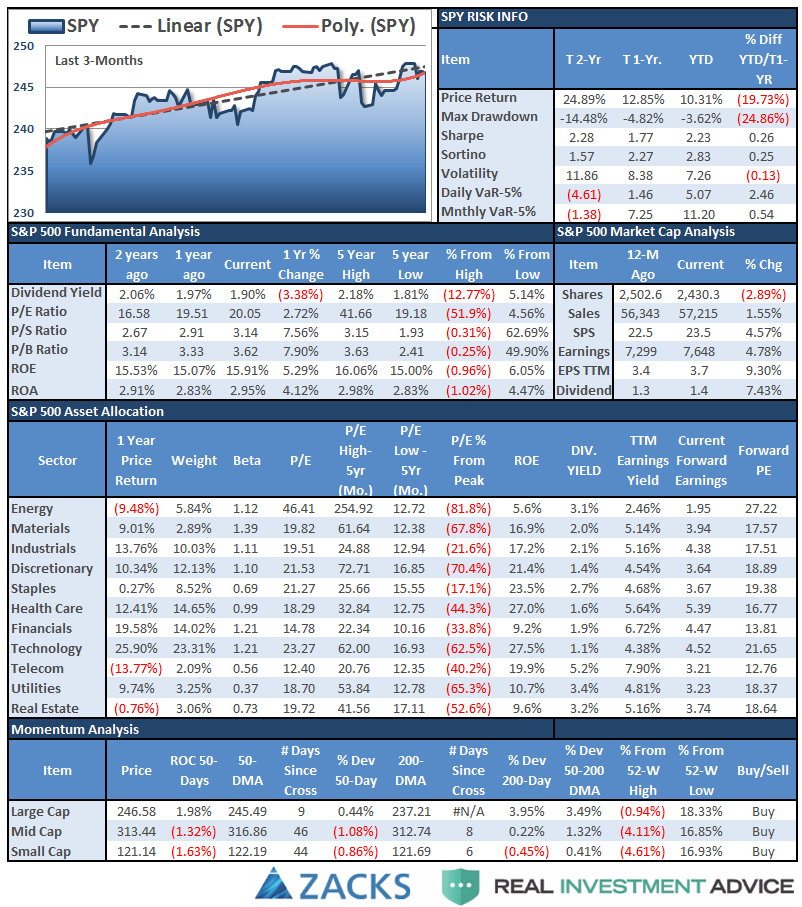

S&P 500 Tear Sheet

Performance Analysis

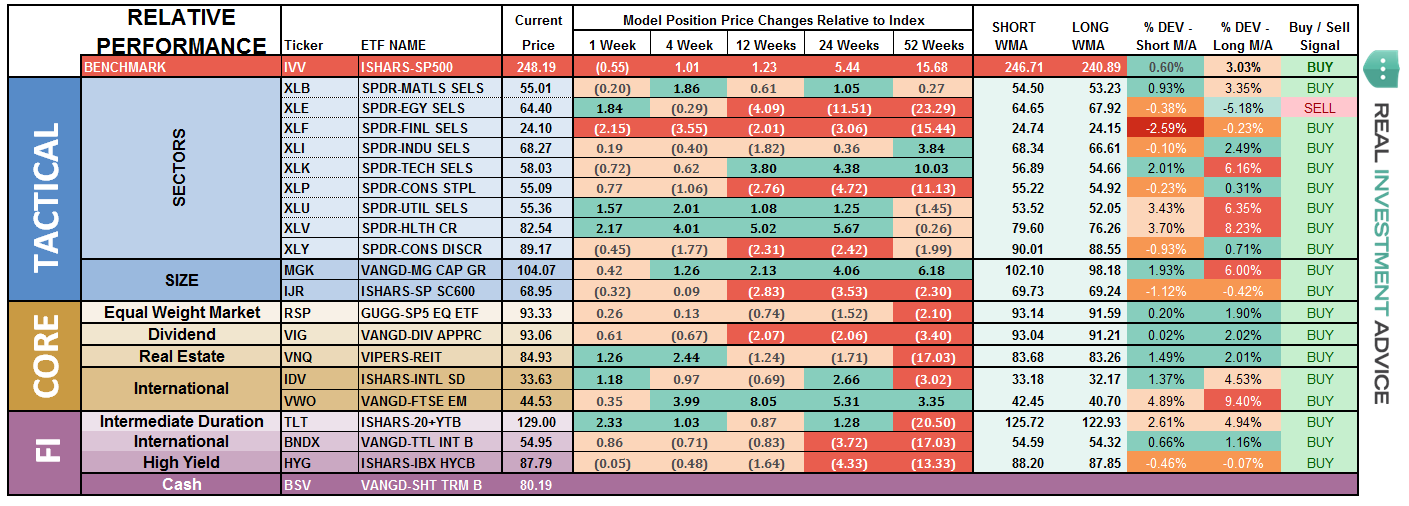

ETF Model Relative Performance Analysis

Sector & Market Analysis:

Let’s take a look at the sector breakdown.

Technology, Staples, Industrials, Materials, Utilities, and Healthcare performed the best this past week relative to the index. Healthcare and Utilities are extremely overbought so profit taking and rebalancing in these sectors is well advised.

Financials and Cyclicals were weaker on a relative basis and the deterioration in the bullish trends continue. Financials have broken the 50-dma and are now threatening the 200-dma but have gotten oversold short-term. While a bounce is likely, the decline in rates has the financial sector on alert while economic weakness is beginning to reveal itself in the discretionary sector as well.

Energy, as noted last week, mustered a decent bounce but the trends and backdrop remain sorely negative. Oil prices remain weak and there is little that suggests the damage is over yet. It is advised to continue using bounces in energy as a means to reduce exposure to the sector. We continue to remain out of the sector entirely.

Small and Mid-Cap stocks which bounced last week, faded this week, as small-cap stocks failed resistance at the 200-dma. Mid-cap stocks are retesting the 200-dma and a break of that support will signal rising risk for the broader markets. Note: the narrowing of breadth in the markets is of a major concern and is often seen prior to more major corrections.

Emerging Markets and International Stocks continue to hold support and money has been chasing performance in these sectors as of late. Continue to hold positions for now but profit taking and rebalancing is advisable.

Gold – As noted last week, Gold was FINALLY was able to break out of its trading range and its longer-term downtrend. With Gold once again very overbought, we will begin looking for an entry point on any weakness which does not reverse the recent breakout.

S&P Dividend Stocks, after adding some additional exposure recently we are holding our positions for now with stops moved up to recent lows. The index climbed back above its 50-dma and is reversing its oversold condition and on a buy signal. The deterioration in “risk” is moving to the perceived safety of yield as interest rates fell to the lowest levels since prior to the election.

Bonds and REIT’s continued to perform well last week as money rotated from “risk” into “safety” along with the decline in interest rates. REIT’s are looking to breakout of a long consolidation cycle and bonds remain favorable. Continue holding current positions for now but we are looking to take some profits and rebalance holdings.

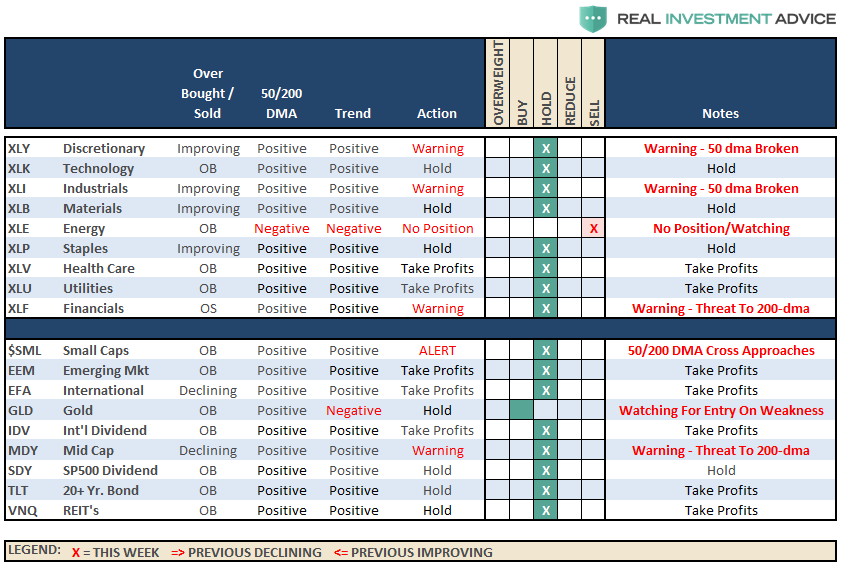

Sector Recommendations:

The table below shows thoughts on specific actions related to the current market environment.

(These are not recommendations or solicitations to take any action. This is for informational purposes only related to market extremes and contrarian positioning within portfolios. Use at your own risk and peril.)

Portfolio Update:

As noted above, the overall bullish trend remains positive which keeps our portfolios allocated toward equity risk. However, we continue to watch the deterioration of the primary supports of the market which remain concerning. But the trend remains the trend for now, and the recovery of the market above the 50-dma allowed us to allocate some capital in newer accounts to equity related risk.

We remain extremely vigilant of the risk that we are undertaking by chasing markets at such extended levels, but our job is to make money as opportunities present themselves. Importantly, stops have been raised to trailing support levels and we continue to look for ways to “de-risk” portfolios at this late stage of a bull market advance.

Again, we remain invested but are becoming highly concerned about the underlying risk.